Billionz Multi-Asset Weekly Newsletter

Global Development

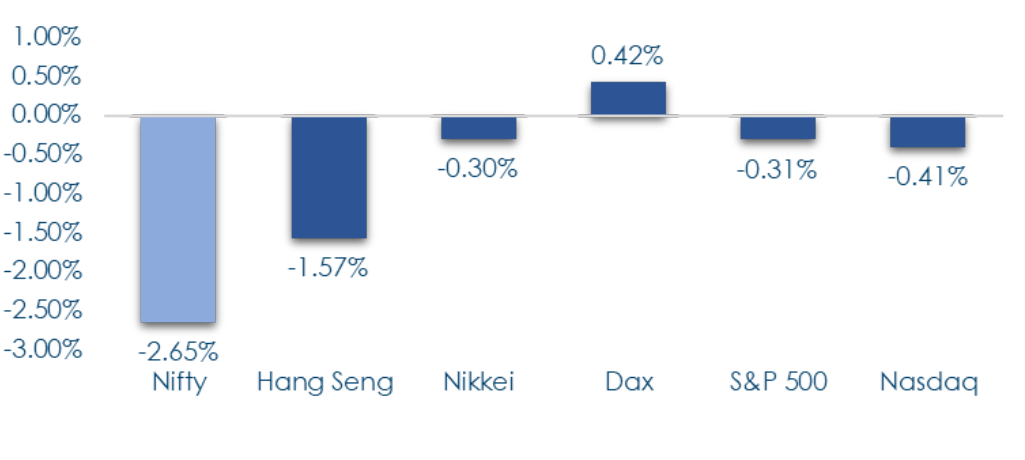

The IT Sector, reeling under outsourcing and immigration concerns, drags Nifty lower.

- US Q2 GDP revised higher: 3.8% QoQ annualized vs expected 3.3%.

- Market trims Fed rate cut bets: 90% (Oct), 73% (Dec) vs 92% & 87% last week.

- US PCE/Core PCE (Aug): 2.7% / 2.9% YoY, in line with expectations.

- Focus next week: US September Jobs report (Friday).

- Domestic: RBI policy (Wednesday), expected to keep rates unchanged.

Global Equities

This is how Global Equities performed this week.

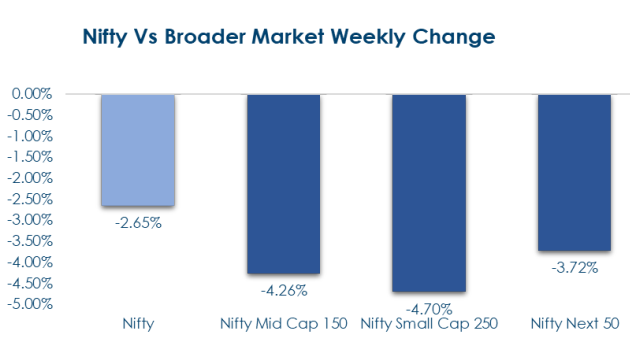

Domestic Equities

- Indian equities remain relatively expensive; midcaps & smallcaps have higher P/E than largecaps.

- Forward earnings indicate possible valuation moderation if growth meets expectations.

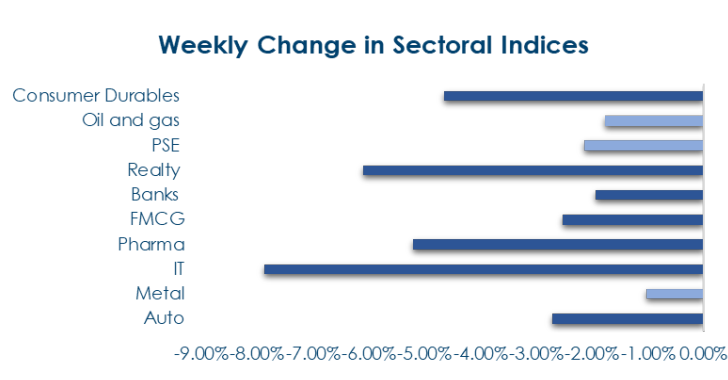

- The IT sector underperformed due to H1B visa costs and potential outsourcing tax.

- Value stocks outperformed, Growth stocks underperformed.

- FPIs: USD 2bn outflows in September so far; ₹19,570 Cr outflow this week.

- DIIs: Buying increased to ₹17,411 Cr, nearly double last week.

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices performed this week:

Fixed Income

Yield on the US 2y rose 4bps to 3.64% and that on the 10y rose 3bps to 4.18% this week

Change in 10y Yields across the Eurozone and the UK was anywhere between -1bps and +4bps this week

Yield on the domestic benchmark 10y traded a 6.46-6.53% range and ended the week at 6.52% compared to the previous week’s close of 6.49%

Overnight call fixings were in the 5.58-5.68% range this week. Banking system liquidity is almost neutral.

1y OIS was up 1bps this week to 5.46% while 5y OIS ended 3bps higher at 5.74%. 5y Mod MIFOR is at 6.40%

10y AAA PSU spread above gsec is 52bps and that of AAA NBFC is about 88bps

FPIs have invested net USD 1.4bn in domestic debt in September so far

Private Equity & Venture Capital

Private equity and venture capital dealmaking in India surged to a record high in the five days ending September 26, with investments topping $1.2 billion (₹8,800 crore), nearly four times the prior week. Deal volumes jumped to 38 from 21, well above the usual 25–30 range, while the top three transactions alone contributed nearly 70% of the value. M&A activity, however, slowed to 6deals from 10. Key transactions included Prime Offices Fund’s purchase of 2.4 million sq. ft. Chennai office campus from Singapore’s Keppel, accounting for about a quarter of the total, and a near-$300 million deal where Prosus and WestBridge Capital acquired Swiggy’s 12% stake in Rapido. Other large flows featured Kedaara Capital’s $240 million investment in Axtria, one of the biggest employee-focused liquidity events in the sector, and Tide Holdings’ $100 million-plus raise from TPG to fund its India expansion.

IPOs

The IPO market is set for a busy week ahead, with four mainboards and 16 SME issues lined up to open. Among them, Infinity Infoway and Advance Agrolife are expected to draw attention, while several other small and mid-sized companies are also entering the market with fresh offerings. The breadth of activity signals continued strong appetite for primary issuances.

Given the crowded pipeline, listing performance is likely to be selective. Well-positioned companies with strong fundamentals and sectoral tailwinds are expected to see healthy subscriptions, while weaker names could struggle to attract demand. SME issues, in particular, may witness sharp volatility at listing due to their relatively thin liquidity.

Overall, investor interest remains robust, but differentiation will be key. Investors are likely to focus on quality names, while being cautious of aggressive pricing in smaller offerings.

Real Estate

Arnya Real Estates Fund Advisors and developer Supreme Universal have partnered to create a ₹1,000 crore ($113 million) private-equity style platform targeting real estate projects in Mumbai and Pune. Under this structure, Arnya will provide fund-management expertise while Supreme Universal will drive project execution, focusing on developments across the two key markets.

Meanwhile, Certus Capital, led by former KKR executive Ashish Khandelia, is preparing to launch its second real estate-focused alternative investment fund, Certus India Opportunities Fund 2. The Category-II AIF, with a target size of ₹300–500 crore ($34–56 million), will take debt exposure in residential and commercial projects across Mumbai, Bengaluru, and Hyderabad, aiming to deliver gross returns of around 20%. Typical deal sizes will range between ₹100–150 crore, adjusted to market opportunities.

Commodities

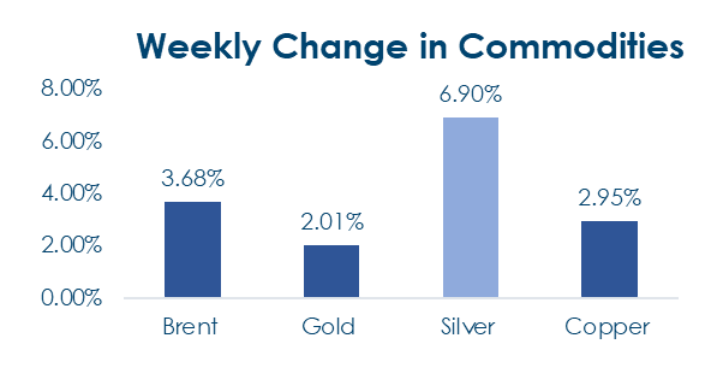

Brent crude: Largest one-week gain since

June 13.

1. Driver: Russia extends petrol export ban until

year-end to secure the domestic supply after the Ukrainian strike.

Gold: Gains for 6th consecutive week amid

risk-off sentiment

What’s New in the World of Wealth Management?

SEBI and the RBI are working to streamline the entry process for foreign investors, aiming to cut registration timelines

from around six months to 30–60 days and simplify documentation for already-regulated global investors. These

measures are intended to boost foreign capital inflows amid subdued corporate earnings and global economic

uncertainties.

On the digital front, The Wealth Company Mutual Fund, led by Madhu Lunawat, has become India’s first AMC to launch a

New Fund Offer (NFO) on the Open Network for Digital Commerce (ONDC), expanding mutual fund accessibility,

especially in Tier 2 and Tier 3 cities

Our Views: What we Like?

Equities

This week’s price action in Nifty50 was quite disconcerting after three solid weeks prior. 24350 is an extremely important

support, and for now, we expect that whichever side we see a break, 24350 or 25350, the next 5% move could happen on

that side. Among sectors, we prefer being overweight on Auto. We prefer value and quality over growth and momentum.

Fixed Income

We may see a move towards 6.60% on the 10y again if the RBI comes across as being less dovish, which we feel it

will. One can consider adding duration to the portfolio around the 6.60% mark on 10y. Any dip in 5y OIS to 5.68-5.70% is

attractive to pay.

Commodities

We continue to remain bullish on precious metals. It’s a view that has worked quite well. We believe it still has further

legs. We are more bullish on Gold than Silver. We expect Silver to attempt the psychological USD 50 mark soon. We are

slightly bullish on Brent after this week’s price action. We could see a move towards USD 75 per barrel. Copper may

continue its gradual grind higher, while Aluminum may see sideways price action.

FX

We continue to remain bearish on the Dollar. Over the last several weeks, we have seen some range-bound price action

in 96.20-98.80.