Billionz Multi-Asset Weekly Newsletter

Nifty Rebounds from Key Support; Momentum Builds in Select Pockets

Weekly Global Developments:

- US Inflation & Fed Outlook: US November inflation came in lower than expected, with recent comments from Fed members leaning mildly dovish. Markets are now pricing in ~2.5 rate cuts by the end of 2026.

- Global Central Banks: In contrast to the Fed, other major central banks struck a relatively hawkish tone this week.

- Crude Oil Watch: Optimism around a potential Russia-Ukraine peace deal has weighed on Brent prices. However, value buying is emerging near sub-USD 60 levels.

- Market Liquidity: Expect sporadic and volatile price action across asset classes over the next two weeks as liquidity thins amid the holiday season

Global Equities:

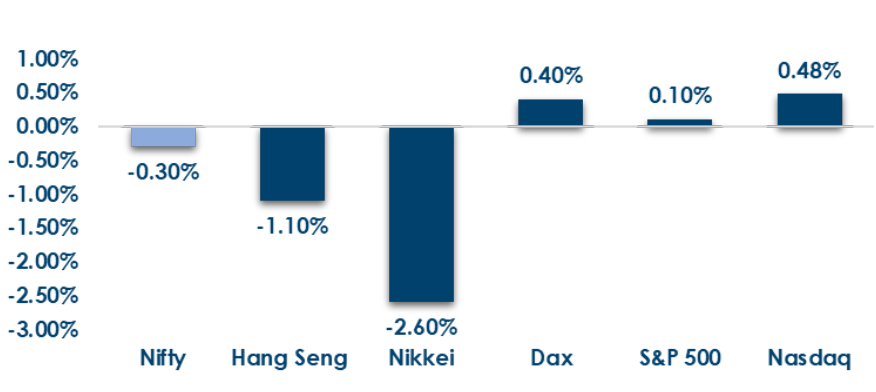

This is how Global Equities performed this week.

Domestic Equities:

- Global equity markets saw mixed performance this week, with FTSE leading gains (+2.6%), modest upticks in S&P 500, CAC, and DAX, while Asian markets underperformed, led by declines in Kospi (-3.5%), Nikkei (-2.6%), and Hang Seng (-1.1%).

- Valuations remain stretched beyond large caps, with Nifty50 at ~21x PE, while Midcap100 (34.5x TTM / 29x forward) and Smallcap250 (30.5x TTM / 26x forward) continue to trade at a significant premium despite lower forward multiples.

- In terms of factors dividend and value outperformed while low volatility and market cap underperformed

- India VIX at 9.52 is at the lowest level ever!

- FPIs have pulled out USD 1.6bn from domestic equities in December so far.

- FIIs remained marginal net sellers this week (₹252 cr outflow), though selling eased sharply from last week, while DIIs stepped up buying to ₹12,062 cr, indicating strong domestic support.

- Reliance Infrastructure (+27.6%) led the gainers alongside Praj Industries and Reliance Power, while Akzo Nobel India (-12.6%) topped the losers, followed by New India Assurance and Aditya Birla Lifestyle Brands.

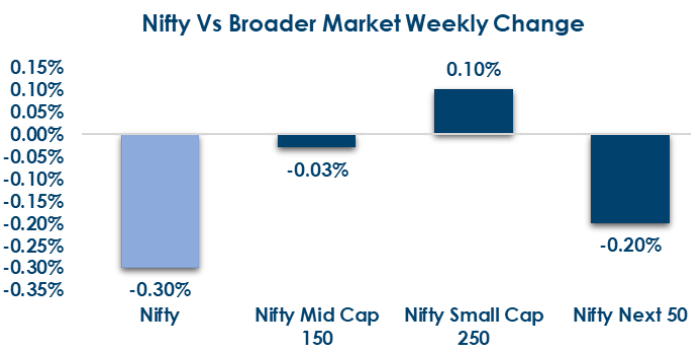

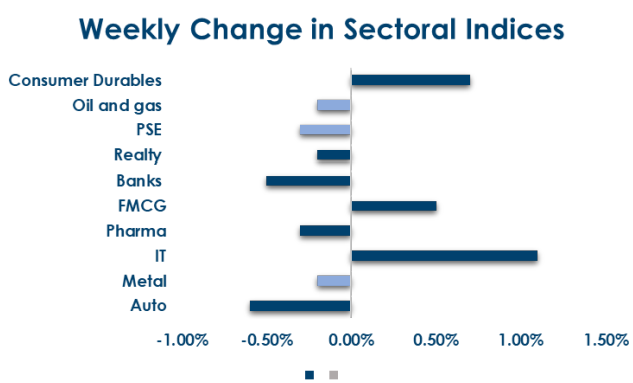

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices performed this week:

Fixed Income:

- Global Rates: US yields eased marginally with the 2Y and 10Y down 2 bps to 3.48% and 4.15%, while Eurozone 10Y yields rose 1–5 bps and Japan’s 10Y JGB climbed 6 bps, reflecting divergence across major markets.

- India Rates & Flows: India rates remained stable with the 10Y G-sec ending flat at 6.60% and 1Y/5Y OIS up 3 bps, liquidity near-neutral, and credit spreads steady, while FPIs have sold a net USD 1 bn of Indian bonds in December so far, signalling continued foreign outflows despite stable domestic conditions.

Real Estate:

- Global Interest: Japan’s Sumitomo Realty is expanding in India with a focused, long-term strategy centred on Mumbai, attracted by rising rentals, lower construction costs, and the city’s economic depth, while preferring ownership-led, ground-up development.

- Domestic Flows: Domestic appetite for real assets remains firm, with 360 ONE Asset raising ₹2,300 crore for infrastructure and commercial real estate, reflecting strong UHNI and family office interest in stable, income-generating properties.

IPOs:

- IPO activity remains strong, with around 11 upcoming issues targeting over ₹750 crore, led by the Gujarat Kidney & Super Specialty IPO, while SME offerings continue to dominate the pipeline.

- Investor sentiment is selective but stable, with GMPs indicating modest listing gains in quality names, especially in the SME segment, even as broader markets stay cautious.

- Listings remain active, with multiple companies set to debut in the coming days, reflecting sustained depth and participation in India’s primary market across segments.

Private Equity & Venture Capital:

- India’s PE/VC landscape in 2025 stayed cautious, with tech funding down ~17% to ~$10.5 bn, while investor focus shifted to quality deals, selective early-stage bets, and stronger IPO/M&A exits, especially in AI, fintech, and enterprise tech.

- Globally, venture funding showed signs of stabilization, with sector-focused investments— particularly in AI and retail tech—gaining traction, reflecting a maturing ecosystem prioritizing disciplined growth and long-term value creation.

Commodities:

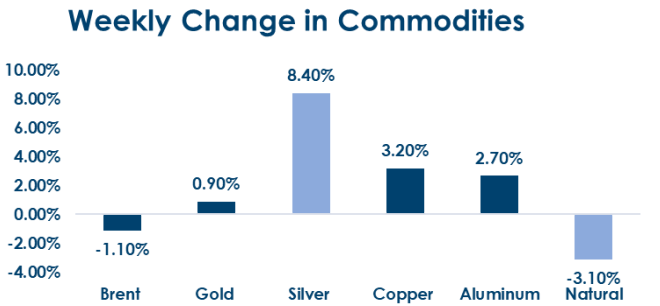

- Commodities saw mixed moves, with Brent crude slipping 1.1% to USD 60.5, and US natural gas falling 3.1% to USD 3.98, while base metals strengthened—LME Aluminum rose 2.7% to USD 2,945, and copper gained 3.2% to USD 11,881—and precious metals advanced, led by gold up 0.9% at USD 4,338 and a sharp 8.4% surge in silver to USD 67.2.

- Base metals and precious metals continue to do well.

What’s New in the World of Wealth Management?

India’s capital markets and wealth management space is seeing important regulatory and market developments that could shape investor experience and participation. A key reform is the Securities Markets Code Bill, 2025, which proposes to unify multiple securities into a single principle-based code to simplify compliance, reduce overlaps and strengthen investor protection across capital markets. This unified framework is expected to make market rules clearer for intermediaries and investors and support innovation and transparency in investment products.

Alongside this regulatory push, market-level changes are also underway that directly affect investors and wealth management dynamics. SEBI has revised mutual fund expense ratio norms by introducing a Base Expense Ratio (BER), excluding statutory levies from core fees and lowering caps across various fund categories to make investing cheaper and more transparent for retail investors. These changes are intended to reduce costs, improve clarity on what investors truly pay, and potentially enhance long-term returns. AMC and wealth management stocks have reacted positively to the framework, indicating market confidence in the adjustments.

Our Views: What we Like?

Equities: Price action of the last couple of sessions in Nifty50 is encouraging. We have managed to bounce back from 50 DMA. 25700 is a crucial support in the near term. We could see the Nifty50 trade a 25700-26300 range over the next couple of weeks. A break in any direction could result in momentum picking up in that direction. The preference is to stick to quality large caps and select midcaps from a medium-term investment perspective. In terms of sectors, we prefer being overweight in banks and IT.

Fixed Income: Whether the RBI manages liquidity through VRR or OMOs will determine how the 10y behaves. We are in a resistance zone in terms of yields in 6.60-6.65%. These are attractive levels to add duration to the portfolio. 5y OIS at 5.95% is close to resistance. One can look to exit paid positions at these levels

Commodities: Optimism around the Russia-Ukraine peace deal sent Brent below USD 60 per barrel, where it is finding value buying. However, concerns of oversupply are limiting the bounce back from those levels. Base metals and precious metals, especially Silver, continue to do so well. We see the rally in Silver extending to USD 70 levels. We continue to remain upbeat on base metals and precious metals.

FX: We expect the Dollar to trade with a weak bias against majors. There is likely to be policy divergence between the Fed and the rest of the key central banks, i.e., BoJ, ECB, and BoE. USDINR was whacked twice by the RBI this week. This should help dampen the momentum on the upside as of now, but in the absence of significant flows, USDINR will have a propensity to bounce back after every major intervention.