Billionz Multi-Asset Weekly Newsletter

Steady Equities, Shining Metals: The Two-Speed Market Setup

Global Developments:

As we come to the end of 2025, it is a great time to unwind, rewind, and brace for 2026.

We touch upon the key drivers, themes, and narratives of 2025 and share perspectives and outlook for 2026 across all asset classes.

Global Equities:

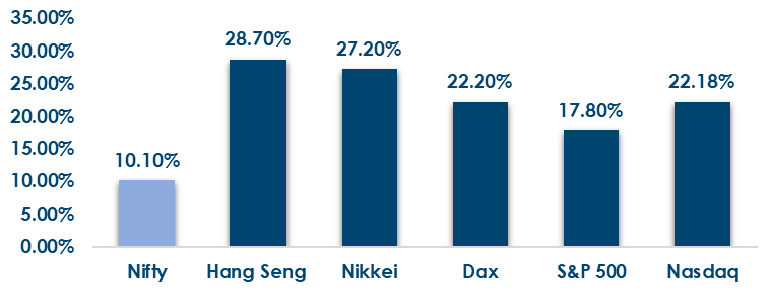

This is how Global Equities performed this year.

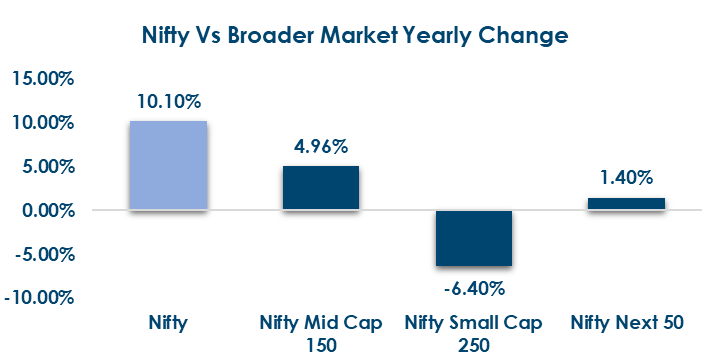

Domestic Equities:

- Equities globally did well despite trade tensions. AI was the major theme this year. Stocks of miners of base and precious metals did well too, amid supply tightness.

- Major global indices posted strong gains this year, led by Kospi (+72.1%), Hang Seng (+28.7%) and Nikkei (+27.2%), followed by DAX (+22.2%), Straits (+22.4%), Jakarta (+20.6%), S&P 500 (+17.8%), FTSE (+17.4%), CAC (+9.8%), and Nifty 50 (+10.1%).

- Indian equities had a quiet year in comparison to global peers. Tariff concerns and rupee underperformance weighed on sentiment. The primary market, on the other hand, was booming.

- Breadth was poor this year, and broader markets underperformed the Nifty50 on concerns of overvaluation and earnings growth

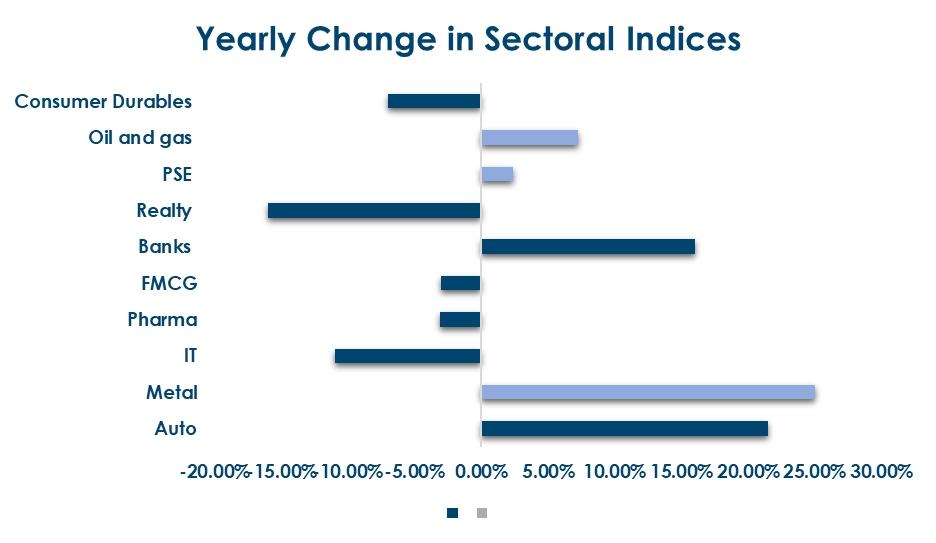

- Among sectoral indices, Bank Nifty outperformed amid RBI easing. Metals did well as commodity prices rallied. IT underperformed on concerns over lagging in the AI race and immigration concerns.

- In terms of factors, value, dividends, and low volatility outperformed growth and momentum. Market cap and the quality were somewhere in the middle.

- FPIs sold net USD 4.6bn of domestic equities in 2025.

- This year saw continued FII outflows of ₹2.96 lakh crore, while DII inflows strengthened to ₹7.73 lakh crore, highlighting strong domestic support compared to last year.

- Force Motors, Ather Energy, and L&T Finance emerged as top gainers with over 120% returns, while Aditya Birla Fashion, Tejas Networks, and Ola Electric were among the biggest laggards, declining over 60%.

Below are the graphical representations for how key benchmark indices performed this year & how sectoral indices performed this year:

Fixed Income:

- Global Rates: US 10Y yields are down ~50 bps YTD, while Eurozone yields are higher by 20–50 bps, with Italy largely flat YoY. Japan stands out, with 10Y JGB yields surging ~94 bps, crossing 2% for the first time since 1998.

- India Rates & Flows: India’s 10Y benchmark yield declined ~20 bps to 6.56% YTD, alongside a cumulative 125 bps repo rate cut to 5.25%. With limited fiscal headroom post tax cuts, growth support has shifted to monetary policy; higher SDL supply and concerns on state finances have widened SDL spreads over G-Secs.

Real Estate:

- India’s real estate sector is expected to maintain its growth momentum, supported by strong economic fundamentals, resilient office leasing, steady residential demand, and increasing diversification into asset classes such as data centres and mixed-use developments. Developer sentiment remains optimistic, with expectations of firm housing demand and prices.

- While residential sales dipped ~16% YoY in Q4 2025 due to higher prices and cautious buyers, institutional investments hit a record $10.4 billion in 2025, reflecting strong investor confidence and deeper institutional participation.

IPOs:

- India witnessed a record IPO year in 2025, raising ~₹1.95 trillion across 365+ mainboard and SME listings. Strong institutional and retail participation made it one of the most active primary markets globally.

- The pipeline remains strong with 190+ companies targeting ₹2.5 lakh crore+, including marquee names like Reliance Jio, NSE, PhonePe, Flipkart, and Zepto— signalling sustained investor confidence and deeper capital markets.

Private Equity & Venture Capital:

- Deal momentum slowed in the final full week of 2025 amid the Christmas holiday, with only 13 deals worth $205.6 million (₹1,846 crore), sharply lower than the prior week’s 26 deals totalling over $600 million. The largest raises were Sensa Core Medical ($72 million) and CoreEL Technologies ($30 million).

- Despite the slowdown in private funding, M&A activity remained steady with nine announced deals, led by Stonepeak’s agreement to acquire 65% of BP’s Castrol business for about $6 billion, valuing the brand at around $10.1 billion.

Commodities:

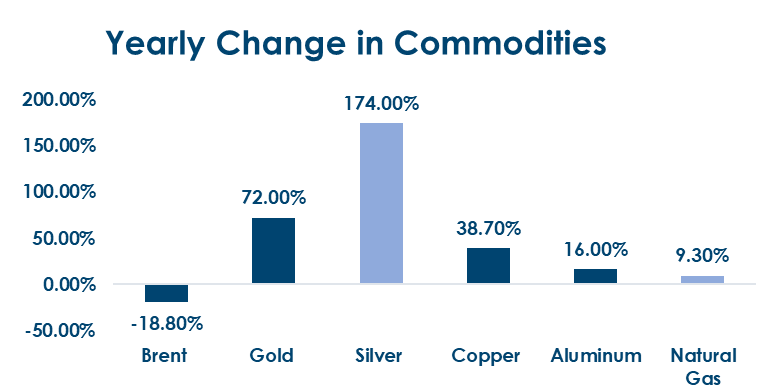

- Major commodities delivered sharply divergent returns this year, with Brent down 18.8% while industrial metals and precious metals rallied strongly—LME Aluminium up 16%, Copper 38.7%, Gold 72%, Silver 174%, Platinum 171%, and Palladium 113%.

- Precious metals were driven by Dollar weakness and the de-dollarisation narrative. Silver skyrocketed on its dual appeal as a safer haven and a good conductor for industrial usage.

- Base metals too rose on Dollar weakness, supply concerns, and optimism around China’s demand revival.

- Brent fell this year as OPEC+ increased production (rolled back production cuts).

What’s New in the World of Wealth Management?

India’s Real Estate Investment Trust (REIT) market has reached a major milestone, emerging as a global powerhouse with a gross asset value of around ₹2.3 lakh crore, surpassing Hong Kong’s REIT market in size. This rapid expansion over just a few years reflects deepening institutional participation, strong occupancy rates across core commercial assets, and growing investor interest in stable yield-driven instruments. With SEBI’s regulatory support and evolving market structures, REITs are poised for further growth and broader inclusion in mainstream portfolios.

At the same time, India’s equity markets have seen unusually low volatility, earning a reputation as one of the calmest stock markets globally. This subdued price movement has challenged traditional derivatives and options strategies, pushing traders to reassess risk-management approaches amid narrow trading ranges and reduced short-term volatility. The shift in market dynamics signals changing behaviour among equity and derivatives participants, even as broader investor engagement and structural developments continue to shape capital market evolution.

Our Views: What we Like?

Equities: We may see an extended period of time for correction. Budget will be an important event, but we do not expect fireworks given that the Government has already expended considerable fiscal space through tax cuts. Valuations in large caps seem reasonable from a long-term investment perspective. We prefer large caps, quality, and value. Trade deal, if done, will impart a big boost to sentiment, which could cause a 4-5% up move for Nifty50. For now, we see consolidation in 25700-26300, and the next 4-5% swing, depending on which side the break happens.

Fixed Income: We believe it is a great time to hold duration in U.S. Treasuries. We believe the Fed will cut rates faster than what the market is currently pricing in and see its balance sheet expanding. On the domestic front, we expect the repo rate to be at 5.25% for several months and banking system liquidity to be in ample surplus. We see RBI OMOs keeping the longer end of the curve capped. We therefore believe it is a good time for a carry roll-down strategy. 6.70% may be capped on the benchmark 10y over the next few months.

Commodities: While the precious metal rally may look overstretched, there is a huge FOMO factor. We will likely see buying coming in at dips. The Weak Dollar should continue to support as well. We remain positive on precious metals, especially Gold. It may continue its march towards USD 5000 in 2026. Base metals have also broken out, and we believe we will see a follow-through in 2026. We expect Brent to be in the USD 55-70 per barrel range in 2026.

FX: We expect the Dollar to continue to trade with a weak bias overall, especially against majors. Rupee may continue to underperform as the RBI’s ability to hold off on Rupee may keep getting tested until the flow picture improves.