Billionz Multi-Asset Weekly Newsletter

Equity Momentum Softens, Metals Stay in Focus as Nifty Nears Key Support

Global Developments:

- The highlight of the week was the announcement of Kevin Warsh as the next Fed Chair. He is seen as an inflation fighter, and having been a former Fed governor, it eased concerns aroundthe Fed’s independence being compromised

- We saw a massive plunge in precious metals, with Gold seeing the sharpest intraday decline since the early 1980s and Silver seeing the biggest intraday decline ever

- Fed kept rates unchanged this week as expected. However, 2 members voted for a reduction.

- The big event on the domestic front is the union budget on Sunday. Equity and commodity markets are open while FX and Fixed Income are closed. In the case of equities, however, there will be no T+0 settlement

- The budget will be followed by the monetary policy on Friday. It will be interesting to see how the RBI addresses the stress in the money markets. The funding cost for banks has soared

Global Equity Markets:

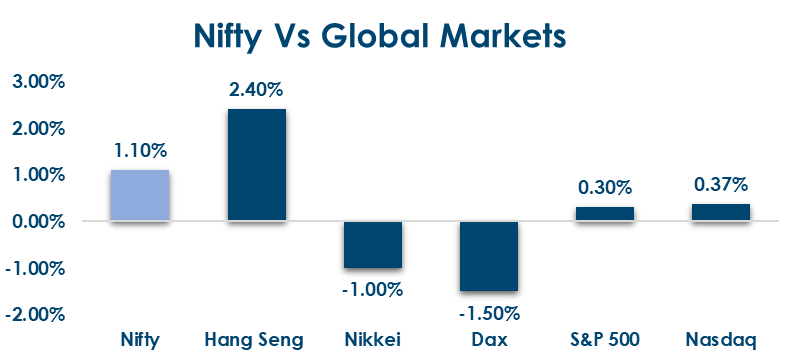

Global equity markets were mixed this week. US markets edged higher, with the S&P 500 up 0.3%, while European indices weakened, led by the DAX (-1.5%) and the Nikkei (-1%).

Asian equities outperformed overall, supported by gains in Kospi (+4.7%) and Hang Seng (+2.4%), although Jakarta fell sharply (-7%), highlighting regional divergence in market sentiment.

Domestic Equities:

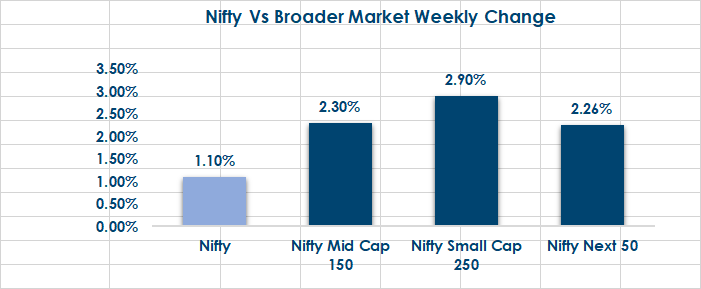

- Domestic equity markets closed the week on a positive note, with Nifty50 up 1.1%, Midcap100 gaining 2.3%, and Smallcap250 rising 2.9%.

- Valuations remain elevated, with Nifty50 trading at a trailing PE of 21x and forward PE of 20.8x, while Midcap100 and Smallcap250 are richer at 35x/28.5x and 29x/26x, respectively, on a forward basis.

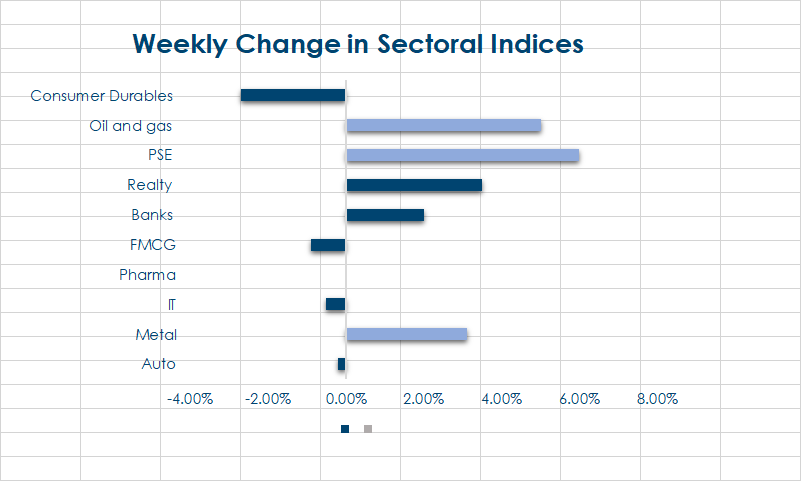

- Sectoral performance was mixed, led by Energy (+6.2%), Oil & Gas (+5%, and Metals (+3.1%), while Realty (+3.5%) and Infra (+2.5%) also posted solid gains.

- On the downside, Consumer Durables (-2.7%), Auto (-0.2%), IT (-0.5%), and FMCG (-0.9%) declined, while Pharma remained flat for the week.

- In terms of factors, value and dividend outperformed, while growth and market cap underperformed

- Based on 30 Nifty50 companies that have reported Earnings for Q3, sales surprise is 5%, and earnrings surprise is -10%

- FPIs sold net USD 4bn of domestic equities in January

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: Global rates were mixed, with US frontend yields easing as the 2y fell 4bps to 3.52% while the 10y was largely unchanged at 4.23%; Eurozone 10y yields declined 1–8bps, while UK Gilts and JGBs edged higher.

- India Rates & Flows: Indian rates were stable to slightly firmer, with the 10y benchmark ending higher at 6.70%, the curve flattening as 1y OIS eased to 5.60% while 5y OIS rose to 6.16%, supported by strong FPI debt inflows, surplus system liquidity of ~₹80,000 crore, and short-term rates with 3m T-Bill at 5.48% and 3m CD at 7.33%, even as overnight MIBOR fixed marginally above the repo rate.

Real Estate:

- CapitaLand Investment has advanced the divestment of its 2.6 mn sq ft International Tech Park asset in Chennai, with strong institutional interest and 360 One emerging as the highest bidder.

- ASK Property Fund invested ₹260 crore to support KREEVA’s acquisition of a South Delhi land parcel for a luxury residential project, underscoring rising institutional participation in NCR real estate.

IPOs:

- The IPO calendar for early February remains muted on the mainboard, with activity concentrated in the SME segment where three new issues and six listings are scheduled, reflecting steady participation in smaller offerings.

- While near-term mainboard IPO activity is subdued, a healthy medium-term pipeline supported by regulatory approvals points to a gradual pickup in larger IPO launches ahead

Private Equity & Venture Capital:

- PE & VC activity moderated in the final week of January, with deal count dropping to 23 and the total value falling to $207 million due to the absence of large-ticket transactions.

- The key highlight was HDFC Capital Advisors’ ₹1,000 crore partnership with Curated Living Solutions, while M&A activity also softened despite Waaree Renewable Technologies’ ₹1,225 crore acquisition.

Commodities:

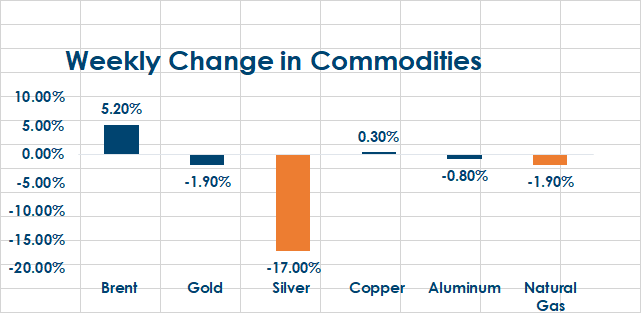

Commodity markets were sharply divergent this week, with Brent crude up 5.2% while precious metals and natural gas saw heavy losses; silver plunged 17%, and gold fell 1.9%, marking one of the steepest weekly declines in decades.

The selloff in gold and silver was intensified by forced deleveraging after CME raised margin requirements, with silver collapsing from USD 118.5 to USD 73.6 intraday before ending at USD 85.2, and gold sliding from USD 5,595 to USD 4,894.

What’s New in the World of Wealth Management?

The Economic Survey 2025-26 highlighted the need to deepen and strengthen India’s capital markets to support longterm growth. It pointed out that corporate bond markets are still shallow and underdeveloped, constraining the flow of long-term capital essential for infrastructure and climate financing, and recommended tax rationalisation on debt instruments and enhanced credit mechanisms to improve market liquidity and participation. The Survey also noted broader trends of strong retail engagement — with over 235 lakh new demat accounts opened in FY26 — and continued buoyancy in primary markets, including robust SME listings and IPO activity.

In the run-up to the Union Budget 2026, markets are preparing for potential policy signals that could influence investor sentiment. Equity and commodity exchanges will remain open on Sunday, 1 February — a rare move timed with the budget presentation — allowing real-time market reactions to fiscal announcements. This reflects the increasing importance of budget outcomes for wealth markets and investor strategies, especially amid ongoing global uncertainties and domestic capital flow dynamics

Our Views: What we Like?

Equities: Nifty50 is seeing technical support around 24900. A break below 24900 could open room for further downside. This line of thought gets invalidated on a close above 25460. We prefer to remain cautious amid lackluster earnings and continued FPI outflows. In terms of sectors, we are overweight in IT and metals.

Fixed Income: Benchmark 10y yield is heading into budget at a key level, around 6.70% Market will be keeping a close eye on the gross borrowing number. Anything above Rs 16 lakh crs may cause the market to panic. Underlying Expectations in terms of the nominal GDP growth rate considered for budgeting will also be scrutinized. One can look to go long duration on any sell-off that we get post-budget.

Commodities: Wild gyrations in Gold and Silver can be seen as short-term speculative positions getting cleansed. We prefer to remain with the underlying structural theme and believe previous metals are a buy on dips. On Gold, we see USD 4400-4500 as being a crucial support, and in silver around USD 72-75 zone is likely to act as a good support.