Billionz Multi-Asset Weekly Newsletter

War-Driven Market Outlook

Global Developments:

- Today it’s been 15 days since the war began.

- While the US is claiming that it has significantly debilitated Iran’s capacity to prolong the war, Iran continues to exercise its leverage over the Strait of Hormuz by blocking it

- March 13th saw the heaviest US strikes against Iran, and Trump has warned that strikes will intensify further. The new Iranian Supreme Leader reportedly is wounded.

- India is procuring Russian oil & gas stranded at sea and is also procuring from the US Gulf coast to minimize dependence on the Middle East.

- In India, gas supply is being rationed to industry and being diverted to households and the transport sector. Restaurants and Hotels are making contingency plans as well.

Global Equity Markets:

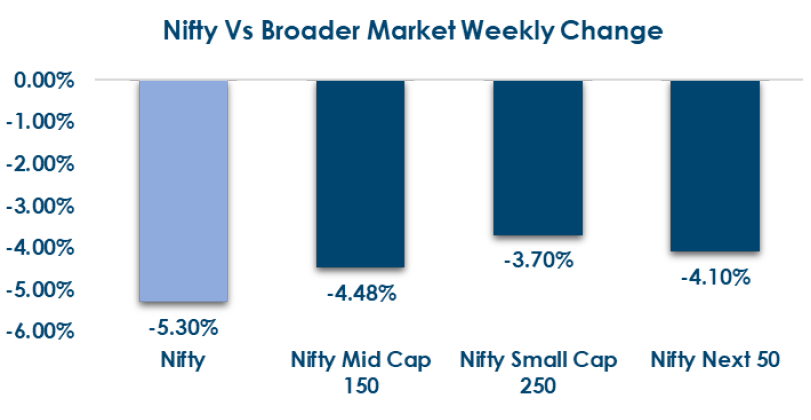

Domestic Equities:

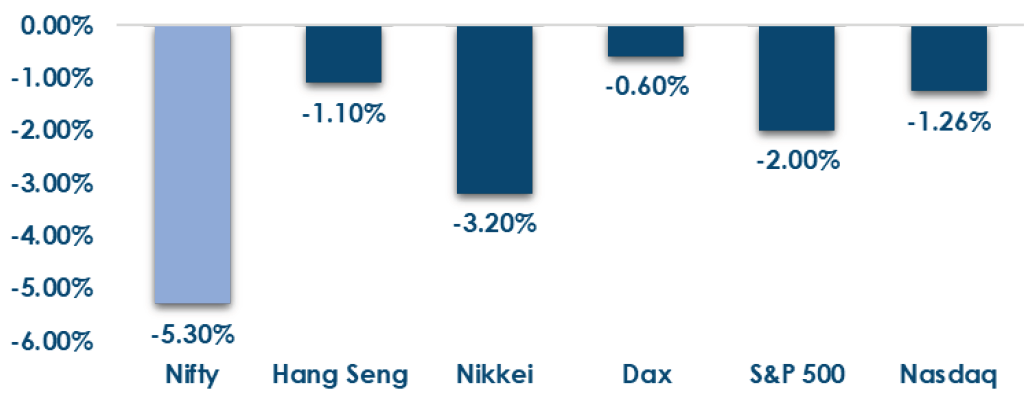

- Most major indices ended lower this week, led by sharp declines in Asia, while the S&P 500 and key European indices posted relatively modest losses

- Nifty 50 trades at 19.1x (TTM) / 18.3x (Forward), while richer valuations persist in Nifty Midcap 100 at 31.3x / 25.7x and Nifty Smallcap 250 at 27.3x / 24.5x, indicating mid and small caps continue to command a significant premium to large caps.

- In terms of factors (those who have the highest exposure to that factor), momentum outperformed while growth underperformed this week.

- FPIs have sold net USD 5.7bn of domestic equities in March so far.

- FII bought ₹35,052 Cr this week vs ₹21,831 Cr last week, while DII invested ₹37,739.8 Cr compared to ₹32,787 Cr in the previous week.

- Fertilisers and Chemicals Travancore Limited (+25.1%), Adani Total Gas Limited (+17.3%), and Happiest Minds Technologies Limited led gains, while Amber Enterprises India Limited (-18.1%), PG Electroplast Limited (-17.6%), and Sapphire Foods India Limited were among the top losers.

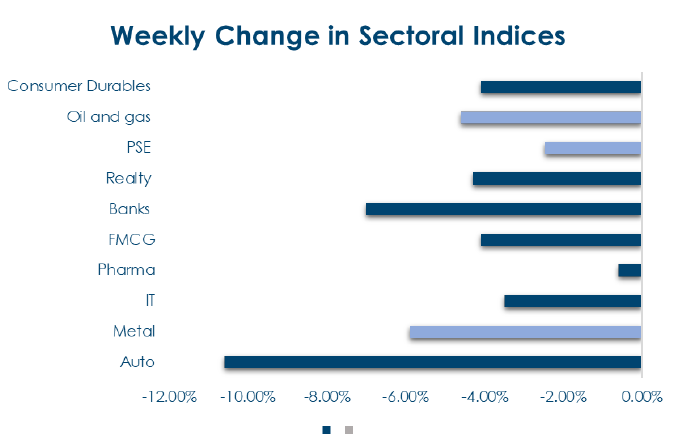

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: Global 10Y yields moved higher across major economies: US +18bps, UK +18bps, France +16bps, Germany +12bps, Japan +7bps, while Australia and China were broadly flat at +1bp each.

- India Rates & Flows: India 10Y G-sec traded 6.64–6.70%, closing 6.68% (vs 6.72%); 1Y OIS +23bps, 5Y OIS +17bps, while FPIs sold ~$800mn debt in March.

Liquidity surplus ~₹2.2L cr; MIBOR ~5.12%, TREPS ~4.8–5.04%, 1Y T-bill 5.61%, 1Y CD ~7%, with 10Y spreads 59bps (AAA PSU) / 70bps (NBFC).

Real Estate:

- Brookfield India REIT brought in 360 ONE as a domestic investor in Arliga Ecoworld Business Parks in a $120mn+ deal, reflecting continued institutional appetite for premium office assets in India.

- Srijan Realty is exploring a buyer for DLF TechPark II and ~26 acres of land acquired from DLF Ltd, in a ₹670cr (~$72.5mn) transaction, expected to close within four months.

IPOs:

- Primary market activity picks up: Novus Loyalty Ltd will launch a ₹60.15 cr SME IPO (₹139–146/share) from Mar 17–20, while GSP Crop Science Ltd plans a ₹400 cr IPO (₹304–320/share) open Mar 16–18, listing on BSE/NSE.

- Exchange IPO progress: National Stock Exchange of India has appointed 20 merchant bankers for its longawaited IPO, which could raise ~₹23,000 cr via OFS, potentially making it one of India’s largest listings.

Private Equity & Venture Capital:

- PE–VC activity rebounded, with 23 deals raising $277.7mn (+56%), supported by a $100mn+ transaction; notable deals included Mozark ($40mn Series B) and investments in Mosaic Wellness, Kaar Technologies, StrideOne, and Eat App.

- M&A activity stayed muted with 5 deals (vs 9 last week); key transactions included Kansai T&D investing $17.3mn for a 10% stake in OMC Power and Cars24 acquiring Vasundhara Infotech LLP.

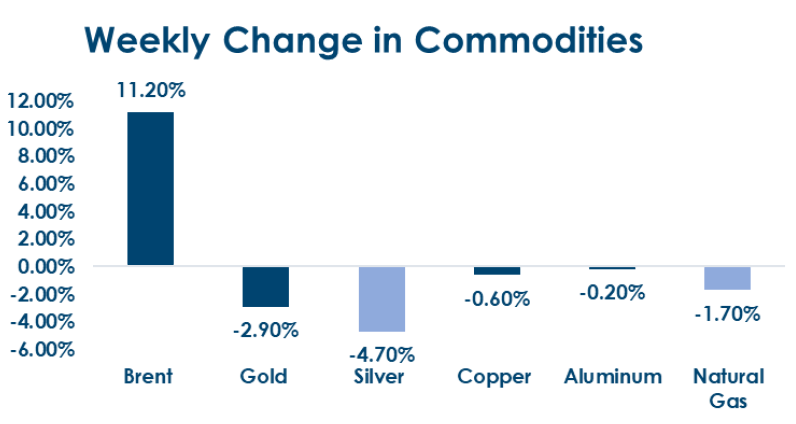

Commodities:

- Energy surged: Brent Crude jumped 11.2% to $98.7, while U.S. Natural Gas slipped 1.7% to $3.13 and European Natural Gas declined 6.1% to €50.1.

- Base metals steady: LME Aluminum eased 0.2% to $3,439, while Copper fell 0.6% to $12,780.

- Precious metals corrected: Gold dropped 2.9% to $5,019, and Silver declined 4.7% to $80.6.

What’s New in the World of Wealth Management?

In a key regulatory development, the Securities and Exchange Board of India has revised the reporting framework

for Alternative Investment Funds (AIFs), shifting from a purely quarterly system to a two-tier reporting structure

comprising an Annual Activity Report and a limited quarterly report. Under the revised framework, AIFs will now

submit a comprehensive annual report through the SEBI Intermediary Portal within 30 days from the end of each

financial year, providing a consolidated overview of fund operations. Quarterly reporting will continue in a simplified

format, aimed at reducing compliance burden while maintaining regulatory oversight.

Separately, SEBI has also introduced a voluntary debit freeze facility for mutual fund folios to enhance investor

protection and digital security. The feature allows investors to lock their mutual fund holdings—across both demat

and non-demat folios—preventing any redemption or transfer of units until the folio is unlocked. The facility will

initially be available through the MF Central platform and is expected to come into effect from April 30, 2026,

providing investors with an additional safeguard against unauthorised transactions.

Our Views: What we Like?

Equities: Equities are now feeling the pinch as the war is seen extending into the third week. There is definitely likely to be

an impact on growth as Gas supply is diverted away from industry. IT is outperforming amid current geopolitical

turmoil while Auto is getting hammered (as the manufacturing process relies heavily on gas). 22500-22700 is now

a crucial support zone for Nifty50 where one can consider investing for the long term.

Fixed Income: Domestic benchmark 10y has been incredibly resilient. Besides OMOs, RBI has likely been buying in secondary

market as well. On the other hand rates have sold off. 1y OIS at 5.84% suggests the RBI may have to hike this year.

For how long the RBI can protect both Bonds and Rupee is the question. Protecting the Rupee means selling

Dollars and withdrawing liquidity from banking system which is negative for Bonds. Doing OMOs or secondary

market purchases means injecting liquidity which is negative for Rupee, which means RBI has to sell more

Dollars!

Commodities: The most surprising has been the behaviour of precious metals during current risk-off times. We believe,

however, that this is an opportunity to add positions, as while the current geopolitical dynamics are temporary,

De-Dollarization is a long-term structural theme that will resurface once geopolitics subsides. Brent and Natural

Gas prices are likely to be headline-driven. Risks remain skewed to the upside in the short term.

FX: Dollar index is at the top of the 95.50-100.50 range and the Dollar may continue to strengthen till the war

continues.