Billionz Multi-Asset Weekly Newsletter

Global and Indian Equities Under Pressure Amid Rising Risk-Off Sentiment and FPI Outflows.

Global Developments:

Trump said that he is strongly considering resuming military action against Iran and that spooked sentiment. Equities and bonds sold off, Dollar strengthened as energy prices rose again.

Trump-Xi meeting in China was the eagerly awaited event of the week. Both agreed on importance of SoH remaining open and Iran not having nuclear weapons.

Government increased import duty on Gold and tightened compliance measures for imports. Government hiked petrol and diesel priced by Rs 3 per litre.

Domestic Equities

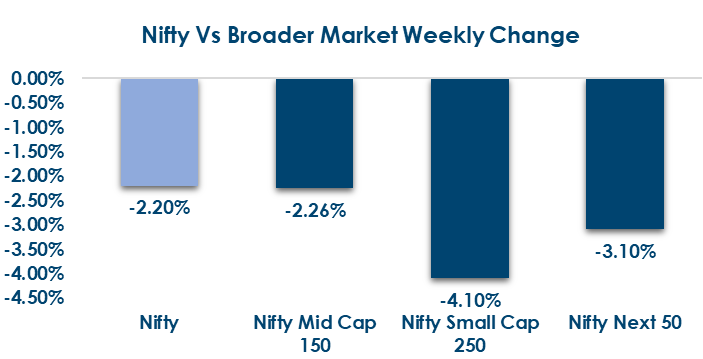

- Valuations across broader markets remain elevated relative to large caps, with Midcap100 and Smallcap250 indices trading at significantly higher PE multiples compared to Nifty50.

- With 66% of market weight of Nifty50 having reported earnings for Q4 FY26, earnings surprise has been around 1-1.5% (in line to marginal beat). Sales surprise has been -0.5% to 0% (Flat to marginal miss).

- FPIs have withdrawn net USD 2.8bn from domestic equities in May so far

- India VIX ended at 18.79 compared to the previous week close of 16.84

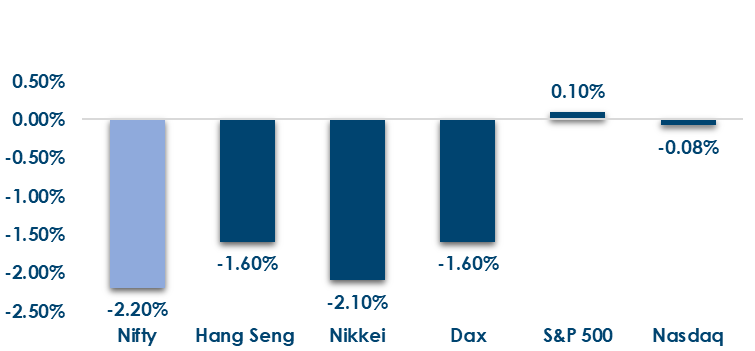

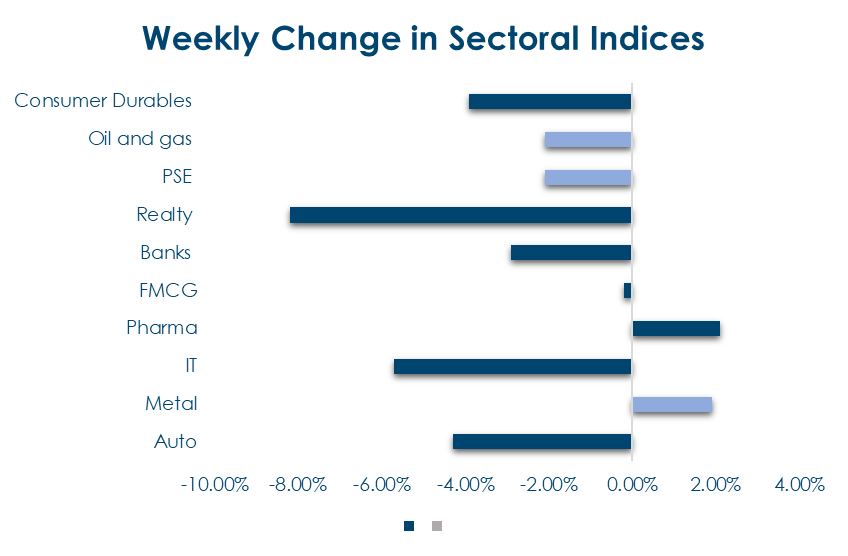

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income

Global Rates:

Global bond yields moved sharply higher this week, led by Japan, South Korea and the US, amid persistent inflation concerns and risk-off sentiment.

India Rates & Flows:

India’s 10-year benchmark bond yield rose 8bps to 7.06%, while OIS rates moved higher across the curve despite surplus banking system liquidity.

Real Estate

- Bagmane Prime Office REIT made a strong market debut, listing at a 3.5% premium to its IPO price, amid robust investor demand for high-quality commercial real estate assets in India.

- The REIT attracted strong institutional participation and marquee backing, with its Bengaluru-focused Grade A+ office portfolio and high occupancy levels reinforcing confidence in India’s premium office real estate segment.

IPOs

- Blackstone also raised USD 1.75bn through the IPO of Blackstone Digital Infrastructure Trust, underscoring rising global investor interest in AI-linked data center and digital infrastructure assets.

- Global IPO markets showed signs of revival this week, with strong investor interest continuing in technology, AI-linked infrastructure and digital asset platforms.

Private Equity & Venture Capital

- PE-VC activity remained steady with selective capital deployment, led by Fairfax India’s $211 million investment in IIFL Capital Services and continued interest in quality financial and consumer platforms.

- Parle Global acquired its US partner’s stake in their joint venture, reflecting the growing push by Indian manufacturing firms to strengthen global operations, technology ownership and export capabilities.

Commodities

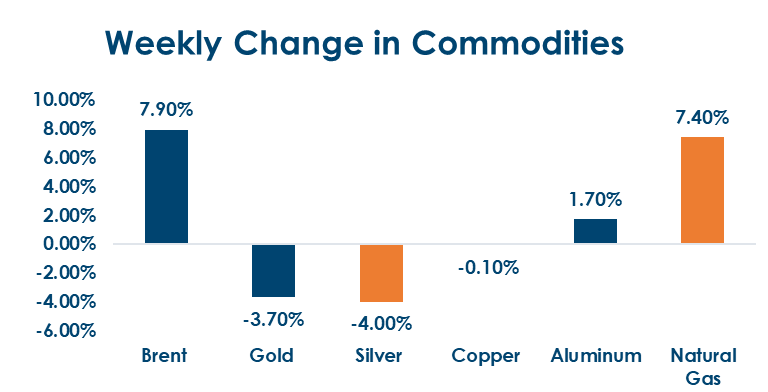

- Energy markets rallied sharply this week, with WTI crude rising 10.5% and European natural gas gaining 13.7%, as geopolitical tensions surrounding the fragile US-Iran ceasefire supported risk premium in oil and gas prices.

- Gold and silver declined sharply, while base metals traded largely stable.

Our Views: What we Like?

Equities: 23800 support on Nifty50 gave way this week. 23100 is the next level to to watch out for where there is a gap support. Q1 earnings have been in line. However earnings expectations will be revised significantly nased on how the war situation pans out over the next couple of weeks. Latest AMFI data suggests retail investors continue pouring money into equity MFs. Small and Midcaps funds are seeing netter traction than large caps.We remain overweight Fin Nifty and IT in our model portfolio.

Fixed Income: WPI surged to a 42 month high of 8.3% yoy this week on higher fuel and power prices. Government passing on some burden to Citizens by hiking pump prices will push CPI higher. We expect the 10y sovereign yield to remain supported at 6.90% till Brent remains above the USD 95 per barrel mark. OIS suggests that the RBI should be hiking rates

Commodities: We remain bullish on commodities overall. Brent is trading in a USD 95-125 per barrel mark and that is something the market has learned to live with. However as realization sinks in that it can remain in this range for long, sentiment will keep getting dented periodically. The stress is even more acute in products and distillates. We remain bullish on precious metals as well

FX: Crosses continue to remain extremely range bound. Euro and Pound have retreated from familiar resistance zones. Rupee continues to remain under pressure and is expected to remain so till Brent remains above the USD 95 per barrel mark. We expect a 93.40-96.90 range for Rupee over the next 3 months