Billionz Multi-Asset Weekly Newsletter

Navigating Consolidation: Strong Domestic Flows, Elevated Yields & Opportunities Across Commodities.

Global Developments:

RBI intervened with a lot of intent this week in offshore and onshore, hammering down spot, pulling USDINR down from all time highs around 97. RBI intervention has flooded banking system with Dollars, creating a glut pushing up near term forwards so much so that the implied annualized forward yield curve is inverted and 1m onshore points are greater than offshore.

There were also reports that India is considering measures including a rate hike to control the Rupee. RBI’s aggressive intervention suggests that the RBI may not be too keen to hike rates and dampen growth outlook and sentiment. It may instead use tight Liquidity conditions as a lever to prevent pressure on Rupee from building up again in the near term.

RBI board announced a dividend of Rs 2.87 lakh crs to the government, slightly below street expectations of over Rs 3 lakh crs.

Hopes of US-Iran reaching an agreement resulted in crude prices coming off. We have seen optimistic statements come in whenever US yields have spiked. The optimism has brought about some respite after bond yields of major economies hit multi year highs earlier in the week.

Domestic Equities:

- Valuations across broader markets continue to remain elevated, with Midcap100 and Smallcap250 trading at significantly higher PE multiples compared to Nifty50 on both trailing and forward earnings basis.

- For 44 Nifty50 companies that have reported Q4 earnings so far, representing 88% of market cap, Revenue surprise has been -0.5% and earnings surprise has been 0.8%

- FPIs have sold net USD 3.2bn of domestic equities in May so far

- India VIX ended at 17.91 compared to the previous week close of 18.79.

- FII activity turned negative this week with net outflows, while strong DII inflows of nearly ₹16,948 crore continued to support domestic equity markets.

- Gland Pharma, Honeywell Automation, and Tata Communications emerged as the top gainers this week, while Engineers India and Central Bank of India were among the key laggards.

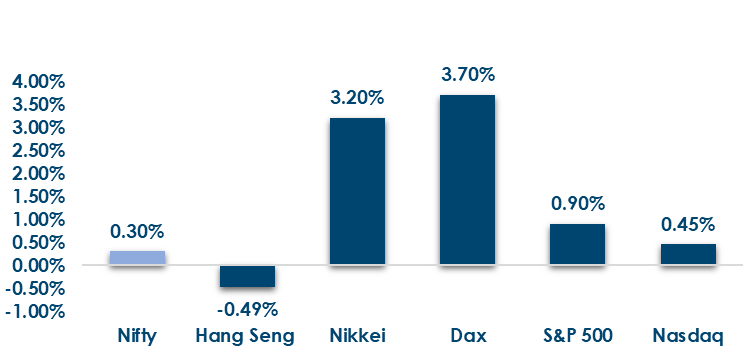

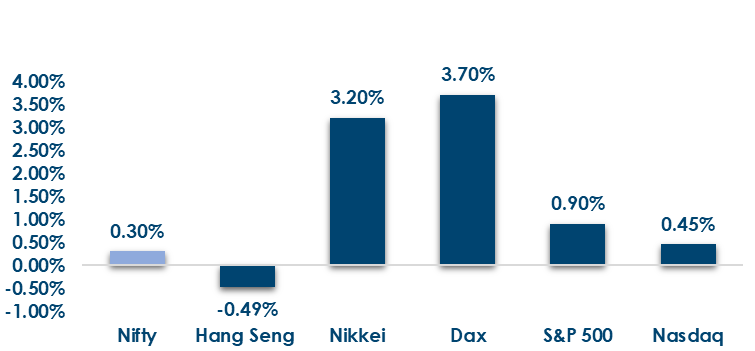

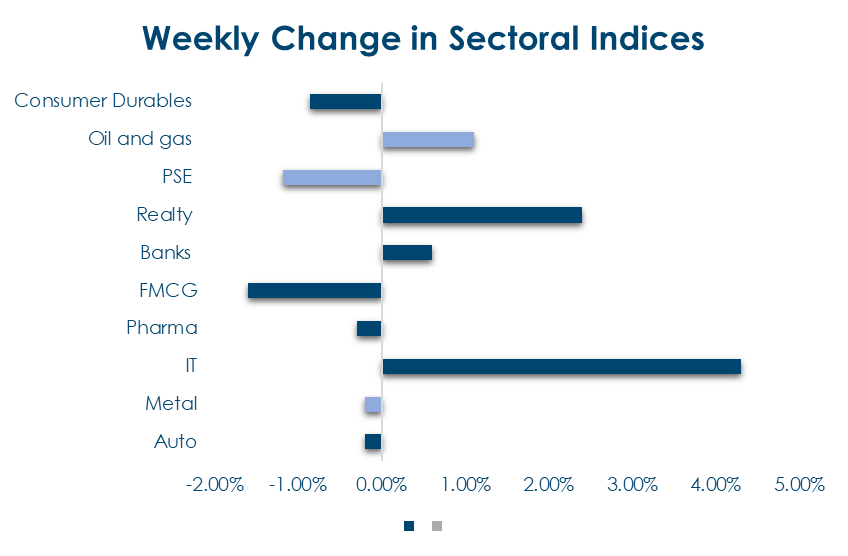

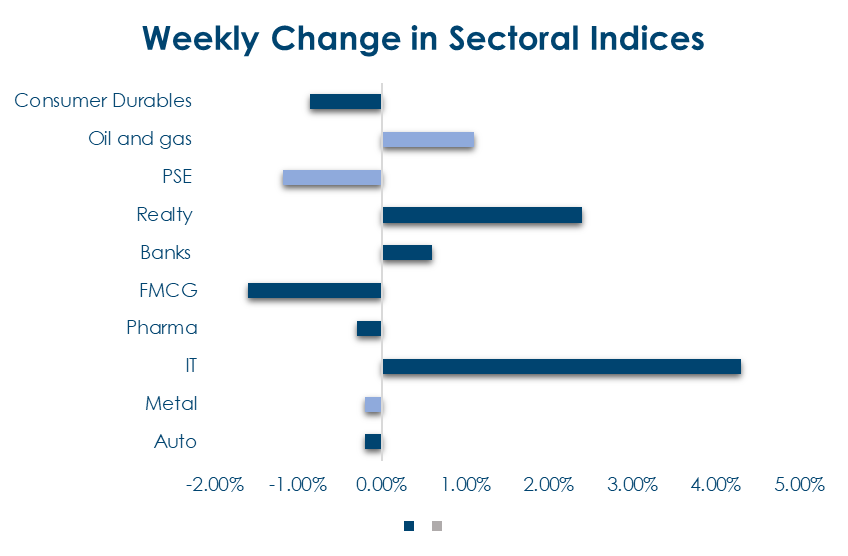

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

Global Rates:

Global bond yields broadly softened this week, led by sharp declines in the UK (-20bps), Australia (-19bps), and major European economies, while Japan was the only major market to witness an increase in 10-year yields.

India Rates & Flows:

Indian rates stayed firm with the 10-year benchmark yield closing at 7.09%, while OIS rates moved higher amid tighter liquidity conditions.

Real Estate

- Real estate developers are increasingly tapping private credit and bond markets for funding, with Kalpataru Properties and Shangrila Infracon planning bond issuances worth over ₹2,500 crore.

- Private credit funds continue to raise exposure to Indian real estate, supported by attractive yields and improving sector fundamentals

IPOs

India’s SME IPO market remains active, with healthcare, jewellery, retail, and food processing companies continuing to access capital markets despite cautious broader market sentiment.

Investor participation in SME IPOs remains selective, with stronger preference towards growth-focused businesses and fresh capital raise-led offerings.

Private Equity & Venture Capital

PE/VC activity remained selective this week, with capital continuing to flow towards scalable consumer, retail, and technology-led businesses, while K Hospitality launched a ₹200 crore venture platform focused on consumer sectors.

On the M&A front, Indian companies continued expanding globally, with MAN Industries acquiring Saudi Arabia-based NPC for nearly $102 million to strengthen its Middle East presence.

Commodities

Commodity markets were mixed this week, with crude oil seeing a sharp correction as WTI fell 8.4% and Brent declined 5.3%, while industrial metals remained firm and precious metals edged lower.

What’s New in the World of Wealth Management

Indian capital markets remained resilient this week despite persistent foreign selling and global geopolitical uncertainty. Domestic institutional investors continued to absorb FPI outflows, reinforcing the structural shift in market ownership toward local flows driven by SIPs, insurance, and retirement capital. The Nifty remained range-bound amid currency pressure and elevated volatility, while broader market participation stayed healthy. Policymakers and regulators also remained focused on improving market depth and participation through measures aimed at strengthening capital market efficiency and long-term institutional inflows.

Our Views: What we Like?

Equities: Nifty50 is likely to consolidate in 23150-24150, both of which are gap support support and gap resistance respectively .While Q4 earnings have been slightly positive, considerable uncertainty around growth outlook still remains which may keep FPIs on the sidelines for some more time.

Fixed Income: OIS rates are still extremely elevated and are pricing in hikes. We believe these are good levels to receive 5y OIS i.e. around 6.90%. 10y benchmark at 7.15% annualized is also attractive to invest in.

Commodities: We continue to remain bullish on precious metals and base metals. Gold is an attractive buy in USD 4300-4500 range and Silver in USD 65-70 range.

FX: Dollar index has been range bound in the 96-100.50 range for the last one year. RBI’s aggressive intervention may keep upside in USDINR capped for a few sessions if crude remains below USD 110 per barrel.