Billionz Multi-Asset Weekly Newsletter

Global Developments & Global Equities

Trump’s comments on reciprocal tariffs dampen sentiment into the weekend.

US Jan jobs report was solid. Though the headline NFP print missed expectations, the previous print was revised even higher, and wage growth surprised the the upside. This caused the Dollar to strengthen. Key data next week would be the US Jan CPI print due on Wednesday. President Trump’s comment that he intends to impose reciprocal tariffs on countries next week soured risk sentiment heading into the weekend. The market is expecting 1.4 cuts (35bps) by the Fed till the end of 2025.

NIFTY V/S GLOBAL MARKETS

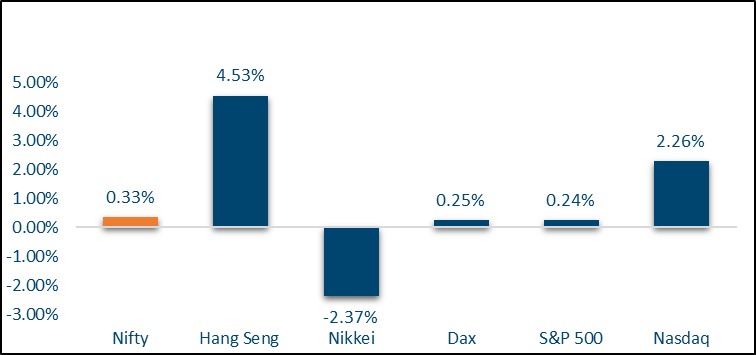

S&P500 ended the week 0.24% lower. CAC,DAX and FTSE were all up 0.3%. Chinese Equities opened after the Lunar New Year and caught up with global equities. Hang Seng ended 4.5% higher and CSI300 ended 2.3% higher. Nikkei lost 2% this week.

Domestic Equities

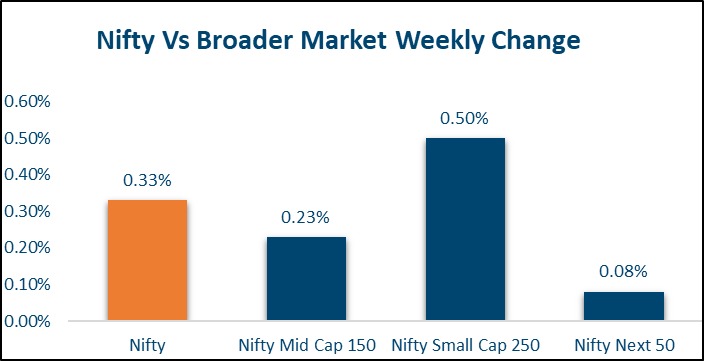

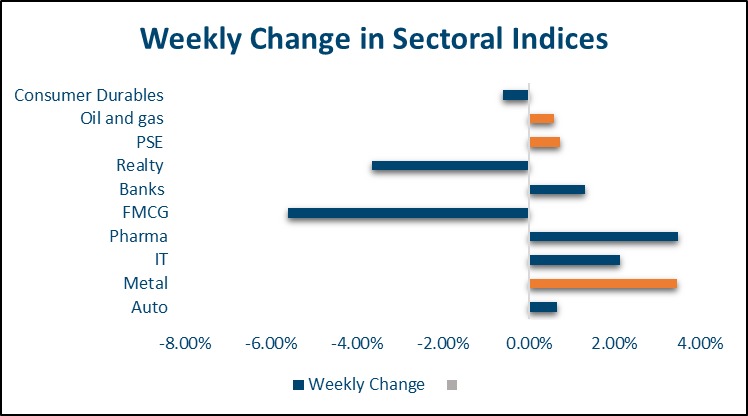

Nifty ended the week 0.3% higher. The midcap100 index was up 0.2% while the Smallcap 250 index ended 0.2% lower. Below is how various sectoral indices performed:

-

- FMCG index -2.8%

-

- Pharma +3%

-

- IT +0.6%

-

- Auto +2.6%

-

- Metals +2.2%

-

- Infra -1.2%

-

- Consumer Durables +2.1%

-

- Oil&Gas -2%

-

- Realty -0.4%

-

- Bank Nifty +1.2%

FPIs have pulled out USD 850mn from domestic Equities in Feb so far. Nifty is currently trading at a trailing 12m P/E of 22. The 2y Average P/E has been 22.6.

Fixed Income, IPO, and Institutional Deals

REAL ESTATE: The rapid growth of India’s coworking and flex office space sector in recent years has been fueled by increasing demand for flexible and cost-efficient shared workspaces. This surge has prompted several providers to enter the public markets, with WeWork India recently filing for an IPO. The India franchisee, controlled by Embassy Group, joins a growing list of companies in the sector exploring public listings. Last year, Awfis Space Solutions Ltd successfully launched its IPO, attracting strong investor interest, while SmartWorks Coworking Spaces Ltd obtained regulatory approval for its share sale. IndiQube Spaces Ltd filed for an IPO in December, and Table Space Technologies Pvt Ltd is also advancing plans to go public, highlighting the sector’s expanding presence in the market.

INITIAL PUBLIC OFFERING (IPO): The Indian primary market is buzzing with activity as investors gear up for a busy week ahead. Eight new IPOs, including six in the SME segment, are set to open for subscription, alongside six market listings. Key highlights include the IPOs of Ajax Engineering and Hexaware Technologies, with the latter’s ₹8,750 crore offering poised to become India’s largest IT services IPO.

PRIVATE EQUITY AND VENTURE CAPITAL: This week saw a rise in capital commitments from private equity and venture capital firms, even as the number of deals declined. A total of $368 million was invested across 28 deals, compared to $301 million across 33 deals in the previous week. It is worth noting that certain transaction values, such as Akasa Air’s funding round supported by PremjiInvest and Claypond Capital, were not disclosed. The week’s largest disclosed deal featured a $200 million investment by Renuka Ramnath-led Multiples PE into technology services firm QBurst. This transaction alone accounted for more than half of the total capital deployed during the period. In the M&A space, Alkem Labs emerged as the top spender this week, acquiring two companies—Bombay Ortho and Adroit.

FIXED INCOME: Yield on the US 10y treasury dropped 6bps to 4.49% and that on the 2y rose 4bps to 4.29% this week. Yields across the UK and the Eurozone were almost flat week over week. Yields on JGBs rose 5-7bps across the curve. RBI cut the repo rate by 25bps to 6.25% as expected through a unanimous 6-0 vote. This was the first policy under new RBI governor Mr Sanjay Malhotra. RBI expects the GDP to grow 6.7% and projected CPI inflation at 4.2% for FY26. Yield on the India 10y ended had dropped to 6.645% just before the RBI policy but rose thereafter to end the week almost flat at 6.70%. RBI maintaining the stance as neutral did not go down well with traders. 1y and 5y OIS ended 1bps and 3bps higher on the week at 6.08% and 6.11% respectively.

Commodities

Brent ended the week 2.8% lower at USD 74.6 per barrel. The EIA report indicated a larger-than-expected inventory build-up. US natural gas prices rose 8.7% this week. Base metals did well this week. LME Aluminum and Copper were up 1.3% and 4% respectively. Dalian Iron ore was up 2.1% Precious metals gained this week. Gold and Silver were up 2.2% and 1.6% respectively.

Ideas & Opportunities

What do we look forward to?

Equities: We expect the Equities to remain sideways in 22800-23800 in the near term. We prefer the comfort of large caps and want to avoid Midcap and Smallcap space. Among sectors, we prefer defensives over high beta and value tilt overgrowth.

Fixed Income: One can look to exit long-duration positions on dips to 6.60-6.65% on 10y and look for levels around 6.85% to reenter. 5.90% on 5y OIS can be targeted to concert floating rate exposures to fixed.

Commodities: We continue with our bullish view on precious metals, both in USD and INR terms. We continue to remain bearish on Brent and believe USD 70 per barrel levels can be revisited in the near term. We expect the base metals to trade sideways.

Disclaimer: The views and opinions expressed above are for informational purposes only and should not be construed as investment advice. IFA does not provide, and this communication is not intended to constitute financial, legal, or tax advice. IFA neither solicits any funds for management nor offers investment advice through this communication. Investors should thoroughly evaluate their financial situation and objectives before making any investment or hedging decisions. It is essential to consider these decisions in the context of an overall portfolio, taking into account personal risk tolerance, time horizon, and financial goals. Past performance is not indicative of future results, and all investments carry inherent risks, including the potential for loss of principal. Any reliance on the information presented in this communication is solely at the reader’s discretion. Always consult a qualified financial advisor before making significant financial decisions.