Billionz Multi-Asset Weekly Newsletter

Global Developments & Global Equities

DOLLAR WEAKENS, AND RISK SENTIMENT IS POSITIVE DESPITE RECIPROCAL TARIFFS, HAWKISH POWELL, AND HIGHER US CPI.

It was an action-packed week with US President Trump announcing reciprocal tariffs, PM Modi visiting the US, Fed Chair Powell testifying in Congress and US CPI and Retail sales data coming outTrump announced reciprocal tariffs. Still, vagueness around timelines of them being effective meant that markets were not spooked. The takeaway from Fed Chair Powell’s testimony was that the Fed is in no rush to cut Rates as inflation remains elevated. The market is pricing in 1.5 cuts by the Fed by the end of 2025. The Possible easing of Russia-Ukraine tensions also supported risk sentiment.

Equities overall had a good week globally. S&P500 was up 1.5%. CAC and DAX rose 2.6% and 3.3%, respectively. HangSeng gained 7% on AI fuelled enthusiasm, while Kospi rose 2.7%

Domestic Equities

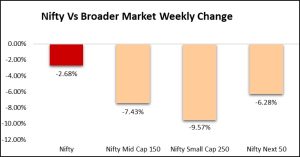

Domestic Equities underperformed global equities. Nifty ended the week 2.7% lower. There was a bloodbath in the broader markets, with Midcap100 and Smallcap250 indices dropping 7.4% and 9.6% respectively. FPIs have sold a net USD 2.4bn in Equities in Feb so far. Jan and Feb combined is 11.4bn, the most ever in the first 6 weeks of any calendar year. In terms of price, it is the worst start for the Nifty50 since 2016.

Fixed Income, IPO, and Institutional Deals

Fixed Income

US 10Y yield fell 2bps to 4.48%, while the 2Y ended at 4.26%. European 10Y yields rose 4-10bps. India’s 10Y yield ranged between 6.68-6.73%. RBI increased OMO purchases to ₹40,000cr amid a ₹2 lakh cr liquidity deficit, with ₹1.8 lakh cr offered. 1Y and 5Y OIS ended lower at 6.30% and 6.09%.

Private Equity & Venture Capital:

PE and VC investments dropped 26% to $269 million, with only two deals exceeding $50 million. ToneTag led the week with a $78 million round, while SpotDraft raised $54 million in Series B funding. Deal volume fell to 25 from 28, but M&A activity remained strong with eight deals, including ONGC NTPC Green’s $2.3 billion acquisition of Ayana Renewable Power.

Real Estate:

Nexus Select Trust, India’s only listed retail REIT, acquired Bengaluru’s Vega City Mall for Rs 913 crore. It invested Rs 870 crore, with the rest for capex. This marks its fourth Bengaluru acquisition, strengthening its presence. The deal, first announced in October 2023, was with Blue Horizon Hotels.

Initial Public Offering (IPO):

IPOs remain significant but less dominant, with investors taking a selective approach. No mainboard IPOs open next week, but the SME segment will see two issues and nine companies will list, including Royalarc Electrodes on February 21.

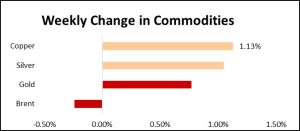

Commodities

- Brent was down 0.4% for the week to USD 74.7 per barrel.

- Base metals had a steady week, with LME Copper and Aluminum gaining 0.7% and 0.4,% respectively.

- Precious metals continues their upward trend. Gold and Silver were up 0.7% and 0.9%, respectively.