Billionz Multi-Asset Weekly Newsletter

Global Developments & Global Equities

WALMARTS’ NEGATIVE OUTLOOK SPOOKS SENTIMENT ON WALL STREET, NIFTY ENDS WEEK BELOW CRUCIAL 22800 SUPPORT.

It was a steady week regarding price action without major data/events/comments. US S&P Global Feb Services PMI missed expectations and slipped into contraction territory for the first time since Jan’23. University of Michigan’s Long-term inflation expectations rose to 3.5% from 3.3%. FOMC minutes were hawkish. Fed members prefer seeing further progress on the inflation front before cutting rates. The outcome of the German elections will be in focus next week. US Jan PCE print is also due next week. The market is pricing in 1.8 cuts by the Fed till the end of 2025, 3.1 cuts by the ECB, 2 cuts by BoE, and 1.4 hikes by BoJ.

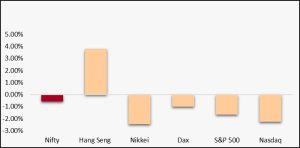

NIFTY V/S GLOBAL MARKETS

US equities corrected this week. S&P500 ended 1.7% lower while Nasdaq ended 2.1% lower. Poor outlook by Walmart dampened sentiment on Wallstreet. CAC, DAX and FTSE were down 0.3%, 1% and 0.8% respectively. Asian equities overall did well. Benchmark indices in Korea, Indonesia, Taiwan were up 2.5%. Hang Seng continued to outperform, gaining 3.8

Domestic Equities

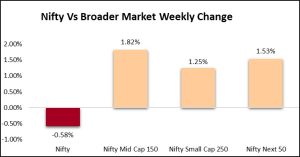

Benchmark Nifty50 ended the week 0.6% lower. Broader markets outperformed with Midcap100 and Smallcap250 indices rising 1.7% and 1.3% respectively. On a trailing 12m basis, Nifty50 is trading at a PE of 21.2 and on a forward 12m basis at 19.2. On a trailing 12m basis, Midcap100 index is trading at a PE of 33.8 and on a forward 12m basis at 29.2. High Beta stocks did well while defensives underperformed.

Fixed Income, IPO, and Institutional Deals

REAL ESTATE: Brigade Group will invest ₹1,500 crore in Kerala, expanding its real estate presence with a new World Trade Center, a Kochi residential project, and a luxury resort in Vaikom. The projects, set for completion by 2030, are expected to create 12,000 jobs, with government support for regulatory facilitation. The Income Tax Bill 2025 introduces clarifications on handling house property losses. Taxpayers can offset losses from one house property against income from another. Any remaining loss, up to ₹2 lakh annually, can be adjusted against other income sources; excess losses beyond this limit cannot be offset in the same year. Unabsorbed losses can be carried forward for eight years, but only to offset future house property income.

INITIAL PUBLIC OFFERING (IPO): Next week, two SME IPOs will open for subscription. Nukleus Office Solutions (Feb 24) is offering 13.54 lakh fresh equity shares at ₹234 each, focusing on co-working spaces in Delhi NCR. Shreenath Paper Products (Feb 25) has a ₹23-crore IPO priced at ₹44 per share, with 53.1 lakh fresh equity shares. Additionally, five companies, including Quality Power Electrical, are set to list in the market.

PRIVATE EQUITY AND VENTURE CAPITAL: Private equity and venture capital activity slowed down, with total investments dropping 20% to $217 million from the previous week’s $269 million, despite the number of deals remaining steady at 23. The largest funding deal of the week came from B2B e-commerce platform Udaan, which raised $75 million in its Series G round, led by M&G Plc with participation from Lightspeed Venture Partners, valuing the company at $1.5–1.8 billion. Additionally, Skegen Management Advisors, the family office of Bharat Biotech’s founders, invested ₹360 crore in Sagar Defence Engineering and Zeus Numerix. Volumes in the M&A space doubled this week to 10 with Head Digital Works acquiring Adda52 from Deltatech Gaming in a ₹491 crore ($56.6M) cashand-stock deal. Meanwhile, InCred Group bought Dubai-based Arrow Capital, boosting InCred Global Wealth’s AUM to $2B across Dubai, Singapore, and London.

FIXED INCOME: Yield on US 10y dropped 5bps to 4.43% and that on 2y dropped 6bps to 4.20%.10y Yields across the Eurozone were down 1-5bps this week. Yield on the India benchmark 10y had dipped to 6.68% intraweek but ended the week flat at 6.706% 1y and 5y OIS ended 1bps lower at 6.2950% and 6.08% respectively The RBI came out with directions for bond forwards which would be effective from 2nd May onwards. The USD 10bn Buy-Sell swap announced by the RBI would inject Rs 86000crs of durable liquidity into the banking system. This should reduce the banking system liquidity deficit significantly and bring it close to neutral.

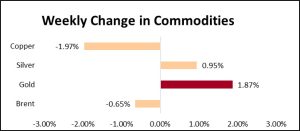

Commodities

Among base metals iron ore was the big mover this week, gaining 6.4% as China vowed more support for its economy. LME Copper and Aluminum were up 0.9% and 1.9% respectively.

Brent dropped USD 2 per barrel despite Israel vowing revenge against Hamas and despite OPEC+ seen deferring production hike to April inspite of Trump’s call. Brent ended 0.4% lower for the week.

Precious metals extended the rally with Gold and Silver up 1.9% and 1.1% for the week.