Billionz Global Weekly Newsletter

Global Developments & Global Equities

2ND APRIL IN FOCUS AS RECIPROCAL TARIFFS TO COME INTO EFFECT

President Trump announced 25% tariff on auto imports this week. It also applies to cars of US auto companies assembled overseas and imported into US.

Trump announced a 25% on countries importing Venezuelan crude.

Trump softened his stance on reciprocal tariffs a bit. He said certain countries could be given concessions.

Developments and announcements over the weekend will be tracked closely, as we approach 2nd April, the date when reciprocal tariffs are to come into effect.

US Fed’s preferred inflation gauge rose more than expected and consumer spending rose less than expected in Feb. Market is pricing in almost 3 Fed cuts by end of 2025.

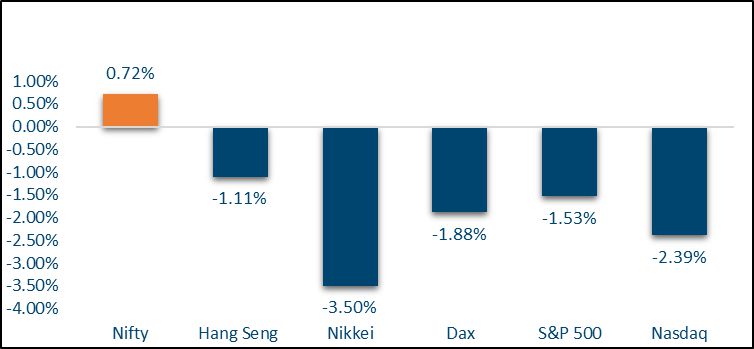

NIFTY V/S GLOBAL MARKETS

Below is how major global indices performed this week:

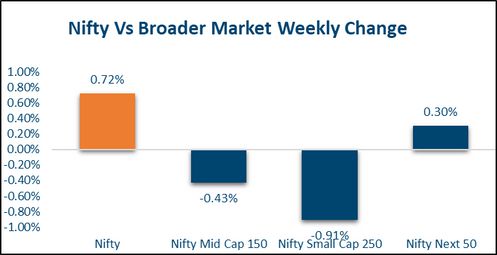

Domestic Equities

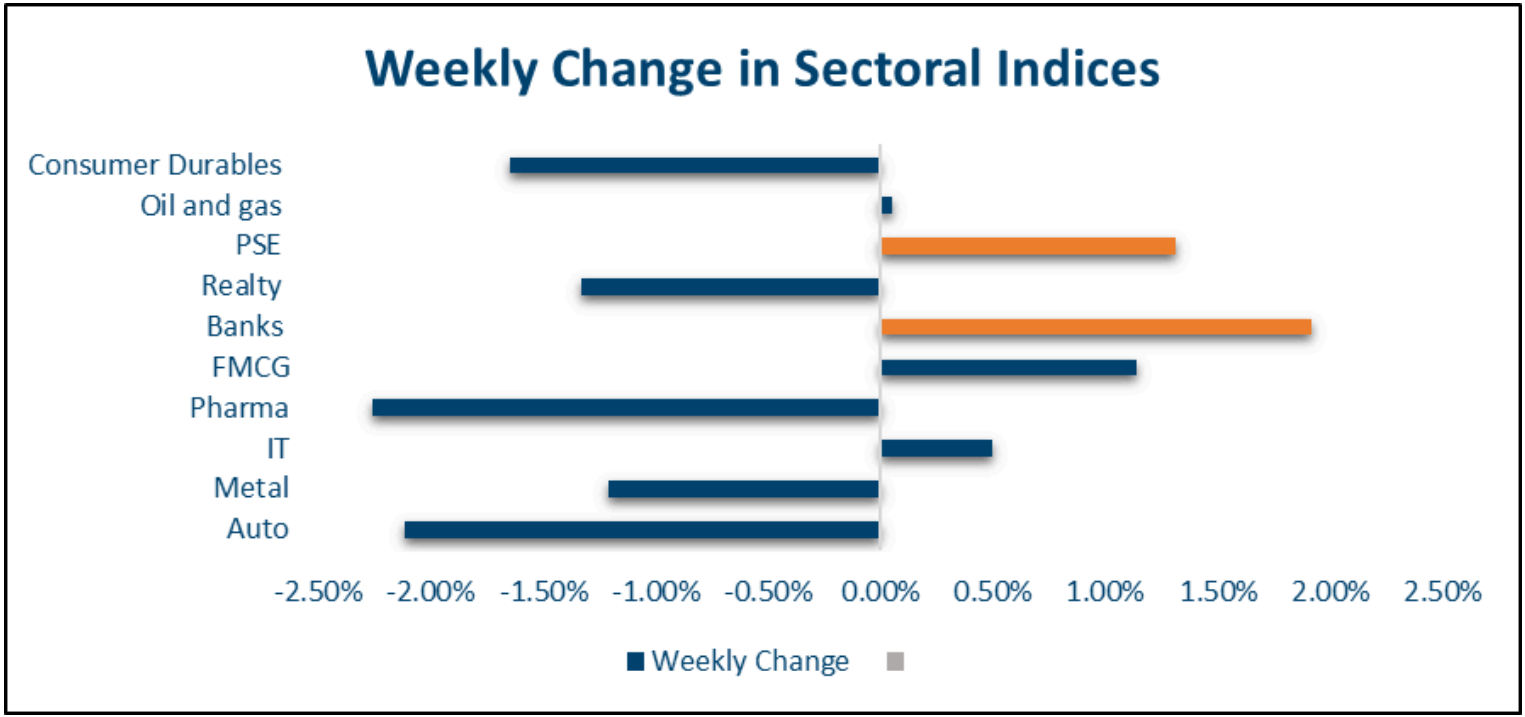

Broader markets underperformed the benchmark this week. Midcap100 and Smallcap250 indices were down 0.3% and 0.9% for the week

Below is the valuation in PE terms at which the large cap, Midcap and Smallcap indices are trading on a trailing and forward 12 month basis:

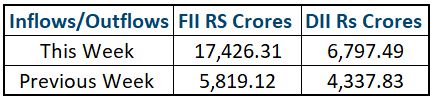

Nifty50: 21.8, 19.6 Midcap100: 34.5, 28.8 Smallcap250: 25, 23.2 FPI sold net USD 400mn of domestic equities in March. FPI flows returned in the second half of the month.

In style terms, Dividend, Liquidity and value outperformed growth and low volatility. SEBI has come out with a discussion paper saying exchanges will have to choose Tuesday or Thursday for weekly and monthly expires. This may require NSE to reverse it’s recent decision to move expiry to Monday and BSE to move single stock expiry from Mid month Thursday to last week Tuesday.

Fixed Income, IPO, and Institutional Deals

REAL ESTATE:

Abound, a cross-border financial solutions provider incubated by Times Internet, has raised $14 million (Rs 119.6 crore) in a seed funding round led by NEAR Foundation, with participation from Circle Ventures, Times Internet, and others. This marks Abound’s first external investment since its incubation at Times Internet. With this funding, Abound plans to expand it’s product offerings, enhance it’s technology infrastructure and grow it’s team in product, engineering and growth. Hakimo, an Al-powered physical security monitoring startup, has raised $10.5 million in a Series A funding round led by Vertex Ventures and Zigg Capital, with participation from RXR Arden Digital Ventures and existing investors Defy.vc and Gokul Rajaram.

PRIVATE EQUITY AND VENTURE CAPITAL:

Big-ticket deals in the infrastructure and renewable energy sectors dominated the list of private equity and venture capital transactions this week, followed by healthcare, fintech and financial services. PE and VC investors committed a total of $817.5 million in the week through Friday, higher than last week’s $763 million. The total volume of deals increased to 28 from last week’s 24, according to data collated by VCCircle.

In the largest deal of the week, Canada Pension Plan Investment Board (CPPIB) and Ontario Teachers’ Pension Plan (OTPP) together invested Rs 4,160 crore in an infrastructure investment trust (InvIT) sponsored by the National Highways Authority of India. The Employee Pension Fund Organization invested Rs 2,035 crore, marking its first InviT investment.

The second-largest deal of the week saw Kotak Alternate Asset Managers Ltd investing in Tirupati Medicare Ltd, helping emerging markets-focused PE firm Affirma Capital make an exit.

INITIAL PUBLIC OFFERING (IPO):

Infonative solutions Ltd (28 mar to 3rd April)

Aten papers and Foam Ltd (28th Mar to 2nd April)

Rettagio Industries Ltd (27th Mar to 1st April)

FIXED INCOME:

Yield on the US 10y ended 9bps lower at 4.25%. 2y yield was down 12bps at 3.91%. 10y Yields across Eurozone and UK were down 2-5bps this week. Yield on the India benchmark 10y ended 4bps lower at 6.58%, lowest level since Jan’22. Government announced the H1 FY26 borrowing calendar in which it pegged the gross borrowing at Rs 8 lakh crs (54% of what it intends to borrow for the entire fiscal i.e. Rs 14.8 lakh crs). This amount was lower than what the market was expecting. In FY25, government borrowed Rs 14 lakh crs through dated securities, Rs 7.4 lakh crs in H1 and Rs 6.6 lakh crs in H2. Drop in US treasury yields combined with RBI OMOs and lack of supply in March have resulted in a rally in bond markets. Also there is expectation that recent Rupee strength could give RBI more leeway to run a more accommodative monetary policy. 1y OIS ended 5bps lower at 6.04% and 5y OIS rose 3bps to 5.90% this week. FPIs bought USD 4.3bn of domestic debt in March. Purchases under FAR route were the highest ever at USD 3.3bn

COMMODITIES:

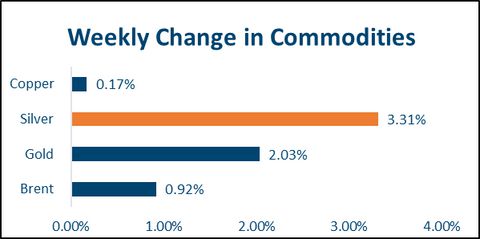

Brent was up 2% for the week at USD 73.6 per barrel as Trump administration announced tariff of 25% on countries buying Venezuelan crude

LME Aluminum was down 2.9% and Copper 0.6% for the week

Gold surged to yet another all time high and ended the week 2.1% higher at USD 3085 . Silver rose 3.3% this week to USD 34.1

Ideas and Opportunities

Our Views : What we like?

Equities:

We expect the Equities to see some time correction over the medium term. We are in times when active investing could outperform. Sector allocation and stock selection would be crucial. Dividend, value and quality are likely to outperform growth and momentum.

Fixed Income:

There is further downside possible in 10y India yield as terminal rate in this rate cut cycle could be

50bps lower than earlier thought. Recent Rupee strength could give RBI more leeway to cut rates

further. One can consider holding on to duration in bond portfolios and look to pay 5y OIS on dips

to 5.75-5.80% to convert floating rate liabilities to fixed.

Commodities:

This week’s price action in gold and silver suggests, the rally in precious metals could have further

legs in Dollar terms. Levels of Rs 90000 on Gold in INR terms is possible. However we would

prefer to use this rally to gradually exit long Gold positions. We are bullish on crude in medium

term and believe that base metals too are a buy on dips.

FX:

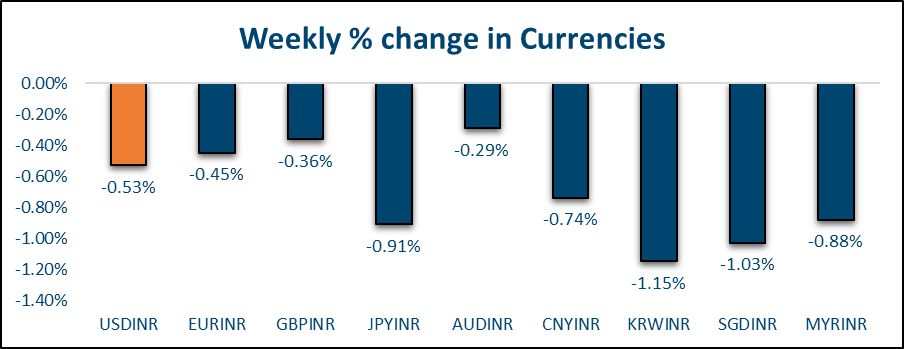

We expect the Dollar to trade with a slight weakening bias. Rupee has outperformed it’s Asian counterparts over the last one and half months.