Billionz Global Newsletter

Global Developments & Global Equities

ISRAEL STRIKING IRAN DAMPENS RISK SENTIMENT

Most US data until Thursday ( ADP, jobless claims, ISM manufacturing and service PMIs) had come in weaker than expected, but the tables turned on Friday with Israel launched air strikes on Iran to prevent Iran from developing Nuclear capabilities. Iran has retaliated with missile attacks.

US CPI and PPI prints for May were softer than expected. The market is expecting two Fed cuts by the end of 2025.

The key event in the coming week would be the Fed’s monetary policy on Wednesday. The market is expecting a status quo in terms of rates. However, the tone of the policy will matter. BoJ policy is due on Tuesday, and BoE policy on Thursday. Both these central banks are also expected to maintain the status quo.

President Trump said letters would be sent to trading partners with unilateral tariff rates. He said that would be the deal offered, and countries could take it or leave it. The release of the jobs report. Headline NFP print came in at 139k against the expected 126k. Unemployment rate was steady at 4.2% and Average Hourly Earnings grew 3.9% yoy against the expected 3.7% yoy. The market is expecting 1.8 cuts by the Fed till the end of 2025. The US May CPI print will be the key data to look forward to in the coming week.

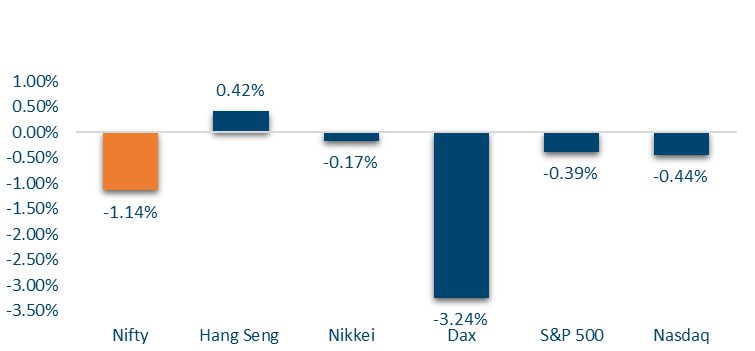

NIFTY V/S GLOBAL MARKETS

Global markets were mixed this week, with European indices like DAX (-3.2%) and CAC (-1.5%) under pressure. Asian markets outperformed, led by Kospi (+2.8%) and modest gains in Nikkei and Hang Seng.

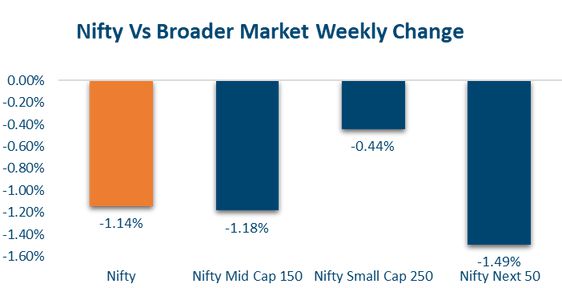

Domestic Equities

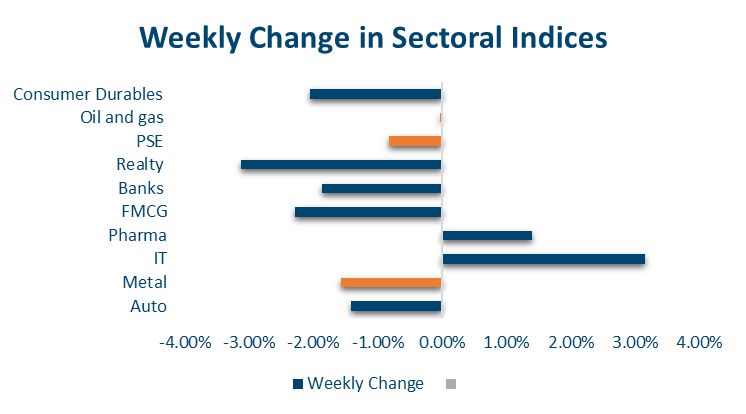

Markets closed lower this week with the Nifty50 down 1.1%, Midcap100 1.3%, and Smallcap250 0.4%. Most sectors declined, led by realty, FMCG, and banks, while IT and pharma outperformed. Valuations remain elevated, especially in the mid and small-cap space, warranting a selective and cautious approach.

In terms of style, Dividend, value, and market cap outperformed while growth and momentum lagged.

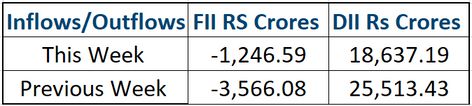

FPIs have sold net USD 600mn of

domestic Equities in June so far.

Inflows into equity MFs hit a 13-month low in May. Investments through SIPs, however, touched an all-time high. Small caps saw bigger inflows than midcaps and large caps. MF AUM rose to Rs 72 lakh crores.

FIXED INCOME

Yield on the US 2y rose 4bps to 3.95%. Yield on the US 10y ended 4bps higher at 4.40% this week.

UK 2y yield fell 7bps and 10y yield fell 8bps as weak labor data increased prospects of the BoE turning more dovish.

Yield on the India 10y ended 1bp higher on the week. It had spiked to 6.40% on a surge in crude prices on Friday but retraced to end the week at 6.36%. May CPI surprised on the downside at 2.82% yoy on lower food inflation on Thursday, pushing the yield to 6.32%. The rally was, however short lived as on Friday we woke up to news of Israel striking Iran, sending crude prices soaring.

10y AAA PSU spreads widened 15bps this week

Overnight call rates have been fixed around 5.35%, lower than the repo rate of 5.50%, as there is an abundant liquidity surplus in the banking system. 1y OIS rose 6bps this week to 5.54% and 5y OIS rose 9bps to 5.76%

FPIs have sold USD 3.1bn of domestic Bonds in June so far.

PRIVATE EQUITY & VENTURE CAPITAL

Private equity and venture capital activity picked up this week, with 24 deals totaling $465 million, a 60% jump from the previous week’s $290 million across 19 deals. The increase in value was largely driven by Advent International’s $175 million investment in Felix Pharmaceuticals, accounting for 37% of the total.

Advent also exited a part of its holding in Aditya Birla Capital, raising approximately $133 million. Other notable mid-sized deals ranged from $20 100 million, contributing to the week’s strong activity levels.

M&A transactions also saw a modest uptick with five deals versus three last week. Highlights include DCM Shriram’s ₹375 crore acquisition of Hindusthan Specialty Chemicals and ICRA’s $26 million deal to acquire data analytics firm Fintellix, signaling growing interest in advanced materials and data-driven solutions.

INITIAL PUBLIC OFFERING (IPO)

Last week’s IPO space remained buoyant, particularly in the SME segment, where issues like Sacheerome attracted over 60× subscription, backed by strong retail and HNI demand. Listings of companies such as Ganga Bath Fittings and Neptune Petrochemicals saw healthy investor interest, with modest listing gains reflecting continued appetite in the broader primary market.

Looking ahead, the upcoming week is packed with activity, featuring six new IPOs, including mainboard player Arisinfra Solutions and five SME issues like Patil Automation, Samay Project Services, and Eppeltone Engineers. These offerings span sectors such as infrastructure, automation, and engineering services, attracting diverse investor segments.

Additionally, five listings are lined up, including Oswal Pumps and other SME firms, which will test investor sentiment in a relatively strong secondary market. With solid subscription trends and multiple fresh listings, the IPO pipeline remains robust, offering both momentum and select opportunities for primary market participants.

REAL ESTATE

Birla Estates, a subsidiary of the Aditya Birla Group, has secured $50 million (₹420 crore) in funding from IFC for two residential projects in Pune (Manjri) and Thane (Kalwa). The projects, expected to deliver 6,000–9,000 housing units, will be developed through SPVs where IFC will hold a 44% economic interest via rupee-denominated non-convertible debentures, while Birla Estates will retain 56%. The total project cost is estimated at $1.1 billion.

Separately, Pantomath Group launched its first real estate fund, Bharat Bhoomi Fund, under its asset management arm, targeting ₹1,000 crore ($110 million) with a greenshoe option of the same size. The fund will invest in data centers, warehousing, and residential properties as part of the fifth Bharat Value Fund series, led by Rakesh Kumar and Bhavya Bagrecha.

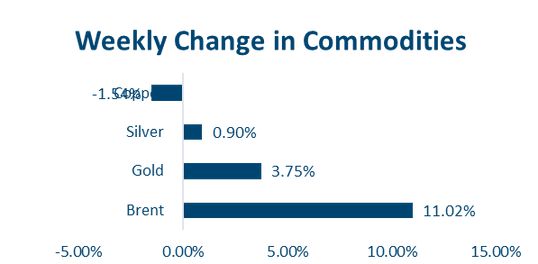

COMMODITIES

Crude prices soared this week as Middle East geopolitics came back into the spotlight with Israel attacking Iran. Brent surged 11.7% this week to USD 74.2 per barrel.

Precious metals rose on safe-haven demand. Gold surged 3.7% to USD 3432, and Silver gained 0.9% to USD 36.3 per troy ounce.e

Base metals were mixed. Aluminum rose 2.1% to USD 2503 while Copper came off 0.5% to USD 9645 per ounce.

Option Strategies

FOR EXPORTERS

Spot ref 86.10, Tenor 12m, Forward extra, Atmf level 87.80

Buy put of 87.65, Sell call of 87.65 with eki at 89.25

FOR IMPORTERS

Spot ref 86.10, Tenor 3m, Importer kiko

Buy call Atms with eko at 88.75, Sell put Atms with eki at 84.50

Our Views: What we Like?

Equities

We continue to remain bullish on the Nifty50 as long as 24500 holds on a closing basis.

Given the current valuation, we prefer adding quality large caps from a long-term investment horizon standpoint. We prefer to stay away from Mid and Small caps at the current juncture.

We prefer value and quality over growth and momentum.

Bonds & Rates

We have been mentioning in our previous weekly reports that we see the 10y yield bottoming out. RBI changing stance to neutral acted as a trigger. We continue to be of the view that 5.50% is the terminal rate in this rate cut cycle.

Conditions for a follow-through on the sell-off in bonds are in place with crude prices surging.

Around 6.50-6.60% could be a level where one can consider buying duration again.

Commodities

It will be interesting to see if Brent sees a follow-through next week. Our base case is that it could settle in the USD 70-80 per barrel range

We remain neutral on Base metals.

Precious metals could see haven demand given that trade uncertainty is back with unilateral tariffs anticipated and a flare-up in Middle East geopolitical tensions.

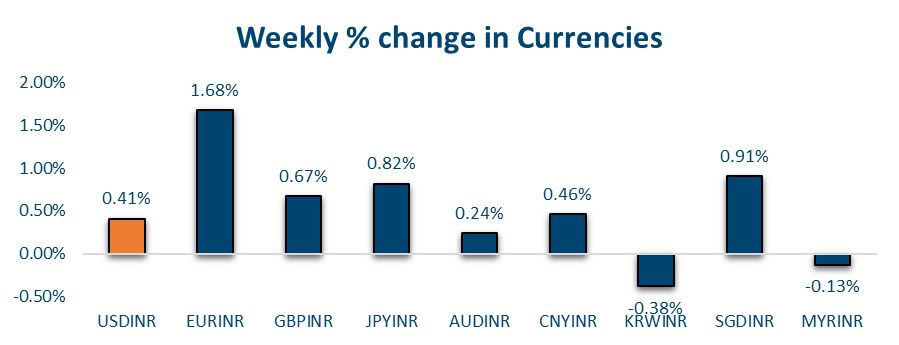

FX

The dollar could continue to weaken against the Majors. It may not weaken to the same extent against EM currencies.