Billionz Global Weekly Newsletter

Global Developments & Global Equities

SOFTENING OF STANCE BY TRUMP ADMINISTRATION LIFTS SENTIMENT

After the initial liberation day shock in the form of massive reciprocal tariff rates, there has been some mellowing down of stance by the Trump administration. It seems to be more willing to give concessions while it negotiates trade deals.

Especially in case of China, there seems to a realization that the Trump administration went too far. Treasury secretary Bessent acknowledged that 145% tariff rate is unsustainable and is akin to a trade embargo

Softening of stance would minimize the extent of trade and supply chain disruption that was expected earlier. Risk sentiment has seen a definite improvement on the back of softening down of stance.

Key data in the coming week would be the US April jobs report due on Friday.

Market is pricing in 3.5 cuts by the Fed until end of 2025.

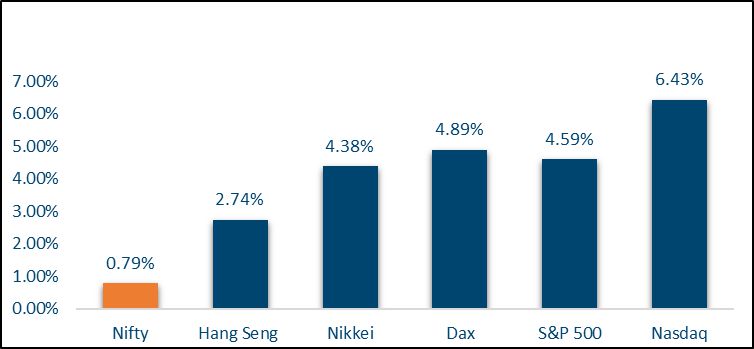

NIFTY V/S GLOBAL MARKETS

Equities globally did well this week.

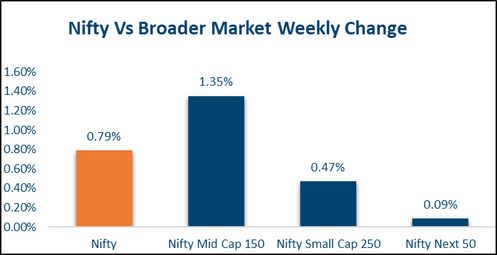

Domestic Equities

The Nifty50 was up 0.8% this week, underperforming major global indices. Midcap100 index was up 1.7% while Smallcap250 index was up 0.5%

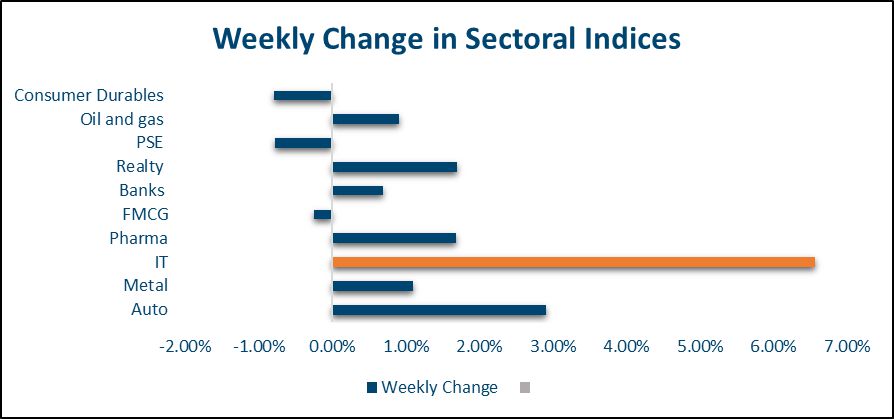

IT index was the outperformer this week. Gift Nifty futures is indicating +0.4% for the Nifty on Monday open

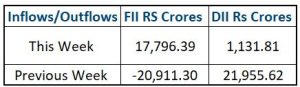

FPIs have sold net USD 650mn of domestic Equities in April so far.

Among styles, Liquidity, Momentum and Growth did well while Low Volatility, Size and Value underperformed. However on a YTD basis, it is exactly the opposite i.e. Momentum and Growth have underperformed while Size and Low Volatility have outperformed.

Out of the 17 Nifty50 companies that have reported Earnings so far for Q4FY25, 9 have delivered positive surprises and 5 have delivered negative surprises. The average Earnings surprise has been 3.3%.

Below is the valuation of large, mid and small caps on a trailing 12m and forward 12m Earnings basis: Nifty50: 22.3, 20.5, Midcap100: 37.3, 29.8, Smallcap250: 26.3, 25.7

Fixed Income, IPO, and Institutional Deals

REAL ESTATE:

Max Estates Ltd has acquired a stalled Noida property project after securing approvals from the NCLT and NCLAT. The takeover of Boulevard Projects Pvt Ltd (BPPL) involves a capital commitment of Rs 1,400 crore, covering all outstanding liabilities, as per an exchange filing. BPPL is now a wholly-owned subsidiary.

With this, Max Estates will revive the long-delayed Delhi One project near south-east Delhi, which has been inactive for seven years. The company plans to develop 2.5 million sq. ft. featuring ultraluxury residences and premium office spaces.

PRIVATE EQUITY AND VENTURE CAPITAL:

Private equity and venture capital investments plunged to their lowest point of the year this week, following a sharp drop from nearly $1 billion recorded last week. The decline comes as earlystage deals continue to dominate the investment landscape. Start-ups collectively raised approximately $84 million this week, while the number of deals remained relatively steady—24 compared to 25 in the previous week.

It’s worth noting that last week’s funding figures were significantly inflated by a single large transaction: a $900-million infusion into IDFC First Bank by ADIA and Warburg Pincus. Without this outlier, the previous week’s total would have stood at roughly $135 million—indicating a week-onweek decline of nearly 40%.

M&A activity gained pace with 11 deals announced, up from the previous week. Notably, 360 One WAM Ltd, backed by Bain Capital, will acquire UBS’s Indian wealth management unit for $36 million, including its stockbroking, distribution, and portfolio management services.

INITIAL PUBLIC OFFERING (IPO):

IThe primary market is set to stay active next week as IPO activity gains momentum after a brief hiatus of around 2 months. In the mainline segment, Ather Energy’s ₹2,980-crore IPO will open for public subscription on Monday, April 28, marking the end of a nearly two-month lull.

The EV maker plans to use the funds for expansion, debt repayment, and R&D. Investor interest is also expected in the SME segment, with three new public issues lined up and one listing scheduled on D-Street. Meanwhile, Canara Robeco Asset Management has filed draft papers for a pure OFS IPO, signalling a broader revival in the primary market.

FIXED INCOME:

US 10y treasury yield dropped 17bps this week to 4.23%. 2y yield ended almost flat at 3.75%

Yields across Eurozone and UK were steady this week

Yield on the India 10y had dipped to 6.30% (lowest level since Nov’21) but ended the week at 6.36%

1y and 5y OIS ended the week almost flat at 5.72% and 5.68% respectively

Banking system liquidity is in surplus. Overnight call rate fixings have been happening below the repo rate in 5.93-6% range.

FPIs have sold net USD 2bn of domestic debt in April so far

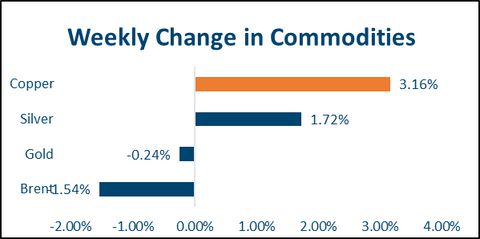

COMMODITIES:

Brent ended the week 1.6% lower at USD 66.9 per barrel.

Base metals had a good week. LME Copper and Aluminium were both up 1.9%

As the demand for safe havens tempered, Gold saw a bit of profit taking, ending the week 0.2% lower at USD 3320. Silver however did well, ending 1.7% higher for the week.

Our Views: What we Like?

Equities:

The Nifty50 has witnessed a sharp short-covering rally, surging from 21,800 to 24,100 in just two weeks. However, with rising geopolitical tensions involving Pakistan and ongoing global trade uncertainties, we expect equities to trade largely within a range, with limited room for further upside.

Fixed Income:

We could have seen a short term bottom in place around 6.30% on the India 10y. That was the level we were targeting. One can look to exit long duration positions and wait on the side-lines for fresh triggers. One can look to re-enter on uptick towards 6.50%

Commodities:

Precious metals, especially Gold, have also performed quite handsomely in the last couple of weeks with both the metals coming across some profit booking from the weekly highs. Therefore, we believe they are also to trade with a rather sideways bias in the near term. Recovery in base metals is also likely to continue.

FX:

We expect the Dollar to trade with a weakening bias against other major Reserve currencies such as EUR, CHF, JPY, GBP. USD may remain steady against Asian and EM currencies.