Billionz Global Weekly Newsletter

Global Developments & Global Equities

RISK ASSETS RALLY AS TRUMP ADMINISTRATION STANCE SEEN MORE CONSTRUCTIVE THAN CONFRONTATIONAL ON TRADE

We have seen the risk sentiment turn on its head post the first week of April i.e. after the week when reciprocal tariffs were announced by the Trump administration.

The US Q1 GDP data was disappointing, indicating a contraction. However the labor market still continues to remain resilient, as indicated by the the latest April jobs report.

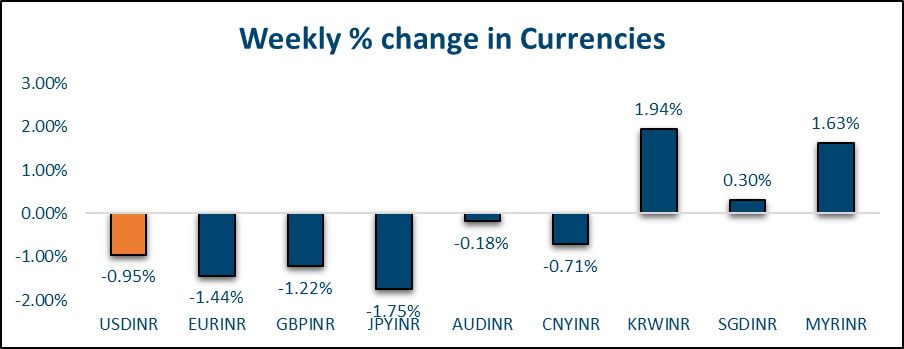

We saw risky assets such as equities and EM currencies do well and safe havens such as US treasuries, JPY and gold take a breather.

It seems the market now feels that big bang reciprocal tariffs were just a way to get trade partners to the negotiation table. While earlier it seemed like the Trump administration’s approach would be confontrational, it now seems that the approach would be constructive in dealing with trade partners. Extension of timeline for when tariffs would come into effect has given room for negotiations to take place. The Trump administration it seems is also asking trade partners for devaluation of Dollar. However this is not confirmed. It just seems so given the concerted way in which EM and Asian currencies have appreciated this week.

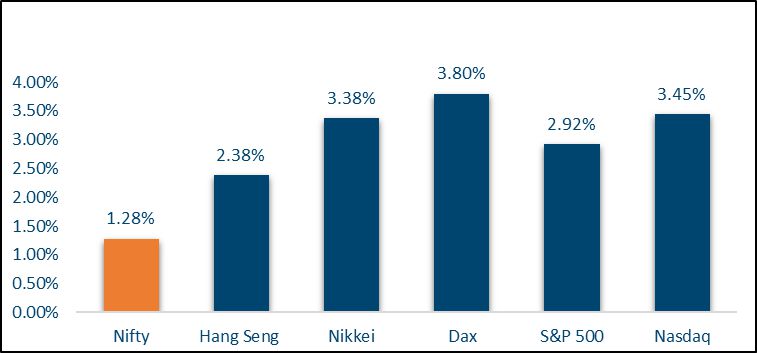

NIFTY V/S GLOBAL MARKETS

Equities globally did well this week. S&P500 and Nasdaq rallied 2.8% and 3.4% respectively this week. Among Asian indices, Hang Seng was up 2% and Nikkei 4%

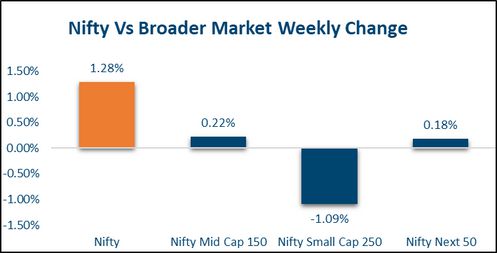

Domestic Equities

For the Nifty50 companies that have reported Earnings so far for Q4FY25, the Earnings surprise has been about 3.5% and Revenue surprise has been 1.9%

Nifty50 22.5, 20.9, Midcap100 37.4, 29.1, Smallcap250 26.3, 25.3

Growth and marketcap outperformed while Dividend yield and value underperformed

Fixed Income, IPO, and Institutional Deals

REAL ESTATE:

MHADA has initiated the redevelopment of 114 layouts in Mumbai, marking a major push toward boosting affordable housing and urban renewal under the ‘MMR as an Economic Growth Hub 2030’ vision. This step is expected to encourage cluster redevelopment and support infrastructure development across the city.

In a significant regulatory relief for developers, the Bombay High Court has struck down a GST demand on the transfer of development rights (TDR). The ruling brings clarity on the tax treatment of TDR, potentially reducing cost burdens and uncertainties in real estate transactions.

PRIVATE EQUITY AND VENTURE CAPITAL:

Private equity and venture capital funding saw a sharp rebound in the week ending May 2, rising to $396 million from just $84 million the previous week. This surge was largely driven by two major investments in the renewable energy and manufacturing sectors, which together accounted for nearly 70% of the total deal value. The week’s biggest funding came from Kotak Alternate Asset Managers, investing ₹1,200 crore in Ace Designers Ltd to support its manufacturing expansion and global growth. Meanwhile, Evren, Brookfield’s renewable energy platform, secured $100 million from UAE-backed Altérra—its first direct investment in India—to boost clean energy initiatives alongside Brookfield and other coinvestors. Meanwhile, mergers and acquisitions activity slowed considerably, with only three deals closed during the week—well below the recent weekly average of around 10. The drop in M&A volume stands in contrast to the uptick in funding momentum, highlighting a divergence in investor activity across segments.

INITIAL PUBLIC OFFERING (IPO):

Arunaya Organics’ IPO saw full subscription by Day 2, reflecting healthy investor appetite, while Kenrik Industries’ issue remained undersubscribed, highlighting the selective nature of current investor sentiment in the primary market. Only two SME IPOs—Manoj Jewellers and Wagons Learning—are set to open for subscription in the coming week, suggesting a relatively muted near-term pipeline. However, the broader IPO market in India is gaining traction with increased activity and anticipation. Looking ahead, over 30 tech startups including Flipkart, PhonePe, and Oyo are preparing for IPOs by 2027, aiming for a combined valuation of $100 billion. Flipkart is shifting its base back to India to meet local listing norms, while PhonePe, already redomiciled, is awaiting regulatory clarity before launching its public offer.

FIXED INCOME:

US 2y yield rose 13bps to 3.82% while 10y yield rose 10bps to 4.31%

10y Yields in Eurozone and UK were mostly steady

Yield on the old benchmark 10y ended 1bps lower at 6.35%. Cut off on the new 10y benchmark auctioned yesterday came in at 6.33%

1y and 5y OIS fell 9bps each to 5.63% and 5.59% respectively

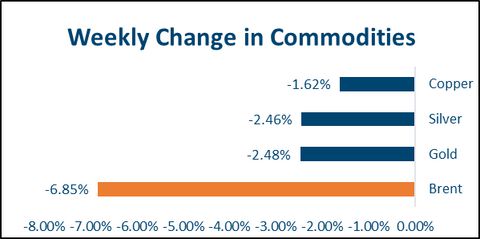

COMMODITIES:

There was a massive sell off in Brent this week. It plunged 8.3% to USD 61.3 per barrel. It seems Saudi Arabia is continuing to pump crude at the same pace, despite such low levels to get non compliant OPEC members in line and increase market share. Precious metals lost a bit of shine this week given the risk on sentiment. Base metals were flat this week with LME Copper And Aluminum ending at 9365 and 2431 respectively

Our Views: What we Like?

Equities:

We believe the current rally could still have legs. We believe the Nifty50 is a buy on dips till 23500 holds. FPI interest in domestic equities has got revived. It initially seemed like we would have the 4th successive month of outflows from equities. However, April eventually turned out to be a positive month. Market has overlooked the uncertainty around domestic terror attack and also weak Q4FY25 Earnings. Amelioration on the trade front and likelihood of a trade deal with the US has instead dominated and driven sentiment.

Fixed Income:

We expect domestic Bonds to trade sideways with a slight Bullish bias. Lower crude, strong government finances and rate cut expectations should keep the yields suppressed. We could see the yield on the old 10y benchmark dip to 6.25% levels.

Commodities:

Focus will be on the OPEC meeting on the 5th of May. We believe a final leg lower in crude prices is possible. That could be a capitulation move. We believe gold and silver could continue to correct further. It now seems to be a crowded trade. However Gold in INR terms could remain supported.

FX:

We believe the USDINR pair has likely seen a bottom around 83.65. We had seen the Rupee weaken in NDF itself to 84.58 levels.