Billionz Global Newsletter

Global Developments & Global Equities

S&P 500 ENDS AT RECORD HIGHS AS GEOPOLITICAL TENSIONS SUBSIDE

Risk sentiment improved drastically as President Trump brokered a truce between Iran and Israel.

The Fed proposed reducing the Enhanced Supplementary Leverage Ratio, which bodes well for large US banks.

President Trump expressed displeasure with Fed Chair Powell, calling him ‘terrible’. He is most likely going to be replaced by a more dovish chairman as early as October. The market is pricing in 2.5 cuts by the Fed by the end of 2025

The US June Jobs report, due on Thursday, will be the key data point to look forward to in the coming week.

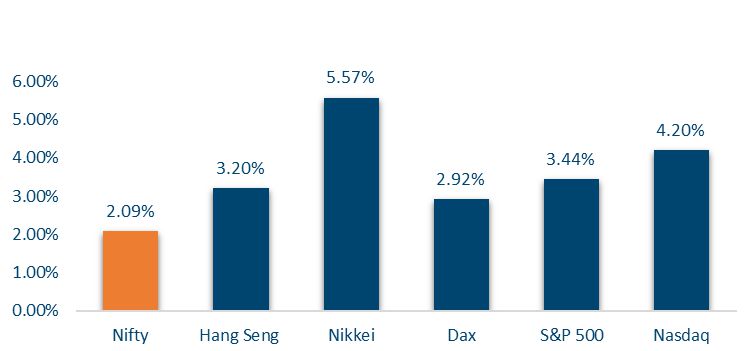

NIFTY V/S GLOBAL MARKETS

Global equity markets saw strong gains this week, led by Japan’s Nikkei (+4.5%), the S&P 500 (+3.4%), and Hang Seng (+3.2%). European indices also rose moderately, while the FTSE lagged (+0.3%). Asian markets broadly advanced on improving sentiment.

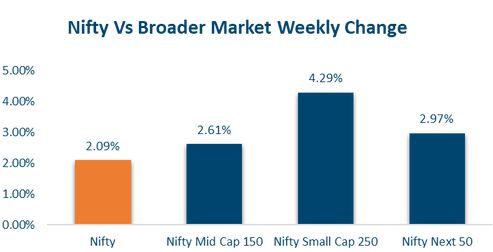

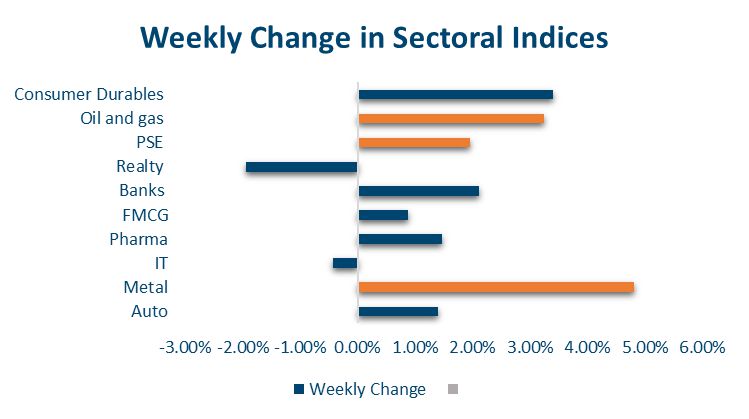

Domestic Equities

Indian equities witnessed broad-based gains this week, with Nifty50 rising 2.1%, Midcap100 up 2.4%, and Smallcap250 outperforming with a 4.3% gain. Among sectors, Metals (+4.8%), Infra (+3.4%), and Oil & Gas (+3.2%) led the rally, while Realty (-1.9%) and IT (-0.4%) saw declines. On the valuation front, Mid and Small caps continue to trade at elevated PE ratios with trailing PEs of 34 and 31.5, respectively, compared to 23.5 for the Nifty50.

In terms of factors, Growth and Momentum outperformed market cap and quality this week. NSE500 breadth has been in favor of advances ranging from 277 to 388 this week.

INVIX at 12.39 is the lowest since Oct’24 FPIs have invested a net USD 1bn in domestic Equities in June so far.

FIXED INCOME

Yield on the US 2y dropped 12bps this week to 3.75% and that on 10y dropped 7bps to 4.28%. US treasuries rallied on news that Fed Chair Powell is likely to be replaced by October and the Fed is proposing to reduce the Enhanced Supplementary Leverage Ratio.

Germany’s 10-year bond yield was up 8bps this week.

Yield on the domestic 10y ended flat at 6.31%

1y OIS ended 2bps higher at 5.54% and 5y OIS ended 4bps lower at 5.71%

Overnight call fixings which had been happening Below SDF jumped on Friday as RBI sucked out liquidity through a 7 day Variable Rate Reverse Repo (VRRR). Weighted average TREPS, which was below SDF through the early part of the week, also popped to 5.42% on Friday.

FPIs have sold net USD 2.9bn of domestic debt in June so far.

10y AAA PSU spreads are around 55bps and NBFC spreads are about 100bps over corresponding Gsec yield

PRIVATE EQUITY & VENTURE CAPITAL

Private equity and venture capital activity picked up in the week ending June 27, with 30 deals recorded — nearly double the 16 from the previous week. However, overall deal value fell 13% to $428 million, down from $495 million.

The defense sector stood out, as drone manufacturer Raphe MPhibr raised $100 million in a funding round led by U.S.-based General Catalyst — the largest funding round in India’s drone space to date.

M&A activity also remained active, with at least five deals totaling over $1.8 billion. The biggest was JSW Paints’ acquisition of Akzo Nobel’s India business for €1.4 billion ($1.6 billion), including debt.

INITIAL PUBLIC OFFERING (IPO)

India’s IPO market saw strong momentum last week, with five offerings raising ₹15,600 crore and attracting bids worth ₹1.85 lakh crore. HDB Financial Services led the way with its ₹12,500 crore IPO, subscribed nearly 17 times, making it the most subscribed billion-dollar IPO in four years. The robust demand signals renewed investor confidence backed by strong institutional interest.

Other listings also performed well. Sambhv Steel Tubes’ ₹540 crore issue was oversubscribed 28 times, while Kalpataru’s ₹1,590 crore IPO saw 2.3× subscription. The trend reflects solid interest across sectors like industrials, financials, and real estate, driven by improved fundamentals and a favorable market outlook.

The momentum is set to continue with 19 companies lined up to list next week. These include Crizac, opening on July 2 with a ₹233–₹245 price band, along with Globe Civil Projects, Rayzon Solar, and Ellenbarrie Industrial Gases—indicating a packed IPO calendar heading into July.

REAL ESTATE

Mumbai-based Arbour Investments has forayed into South India with a $12.2 million investment in two mid premium residential projects by Bengaluru’s ELV Projects. The developments — ELV Highgarden and ELV Kingsland in Whitefield — will add 596 apartments across 11.7 lakh sq. ft. Arbour, led by Chirag Mehta and Priyesh Chheda, focuses on private equity and credit in real estate.

Meanwhile, Motilal Oswal Alternates has fully exited its $56.3 million IREF II real estate credit fund with a gross IRR of 18.3%. Launched in 2015, the fund backed 14 mid-income residential projects. MO Alts credited proactive asset management and early stress identification for the outcome.

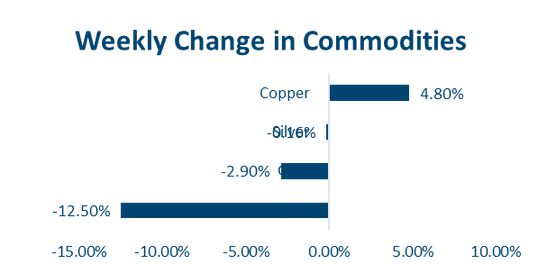

COMMODITIES

Brent fell 12% this week to USD 67.8 per barrel due to the diffusion of geopolitical tensions.

European natural gas prices came off by 18%

LME copper and Aluminum were up 1.8% and 2.5% respectively to USD 2595 and 9878 per tonne

Gold fell 2.8% to USD 3274 per ounce. Silver was flat on the week and ended at USD 36 per ton ounce.

Option Strategies

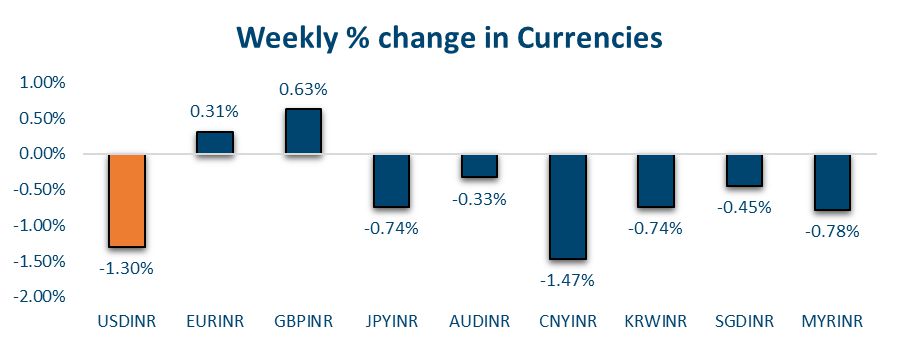

FOR EXPORTERS

Spot 85.49, Forward 85.84

Exporter seagull, BP ATMS 69p, SC 87.05 38p, SP 84.50 31p, 3m, Zero cost

FOR IMPORTERS

Importer risk reversal

BC 86.35, SP ATMS

Zero cost

64p each leg

Our Views: What we Like?

Equities

We continue to remain bullish on Equities and expect the risk sentiment to hold.

Nifty50 has broken out of consolidation in 24500-25200. Momentum and breadth indicators are strong. We could see it test new all-time highs soon.

Bonds & Rates

We believe the market is underpricing US cuts. While a July cut is unlikely, we may see accelerated cuts after the replacement of Powell as Fed Chairman.

Domestically, we believe we have reached the terminal rate in this cut cycle. We set the withdrawal of liquidity this week through VRRR as a prudent step.

Commodities

Brent came off this week on the de-escalation between Iran and Israel. However, we do not see Brent slipping below USD 60 per barrel again.

Precious metals may not see safe haven demand but may be supported on overall Dollar weakness.

FX

We continue to see further Dollar weakness.