Billionz Global Newsletter

Global Developments & Global Equities

BIG BEAUTIFUL BILL BECOMES LAW; CONCERNS MOUNT OVER US FISCAL PATH

Trump’s Big Beautiful Bill cleared the House after being cleared by Senate. It was signed into law by President Trump. This has raised concerns about US fiscal deficit growing and debt to GDP ballooning. The concern was reflected in Bonds and Rates. The US June Jobs report also beat expectations. This resulted expectations getting trimmed.

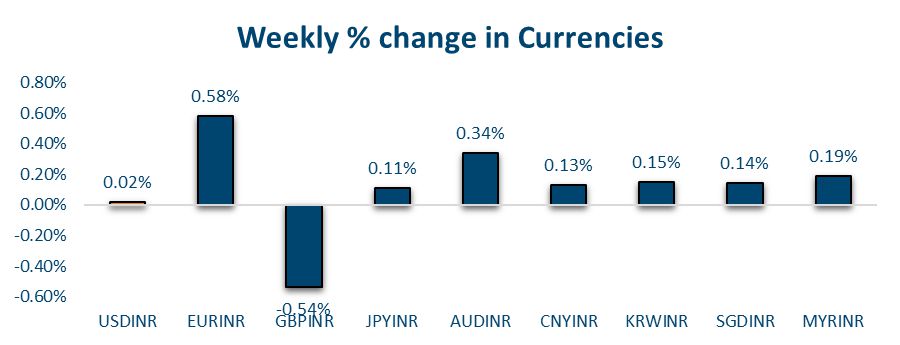

Trump has said that he will be sticking to the 9th July deadline for reciprocal tariffs. If a deal is not reached by then, goods from those countries will face a tariff rate that would be determined by the Trump administration.

The focus will be on Developments around this in the coming week. Letters are likely to be sent to 12 countries on Monday. India has not yet signed a deal/MoU with the US. Access to dairy and agriculture markets remains a sticking point. The US has so far only signed trade agreements with Vietnam and the UK.

UK Chancellor did not get support from her own party’s MPs to strengthen government finances. This led to apprehensions about the Chancellor stepping down. This, in turn, resulted in a sell-off in UK gilts and the Pound. However as the PM expressed confidence and said that the Chancellor would continue, we saw some retracement in UK Gilts and Pound.

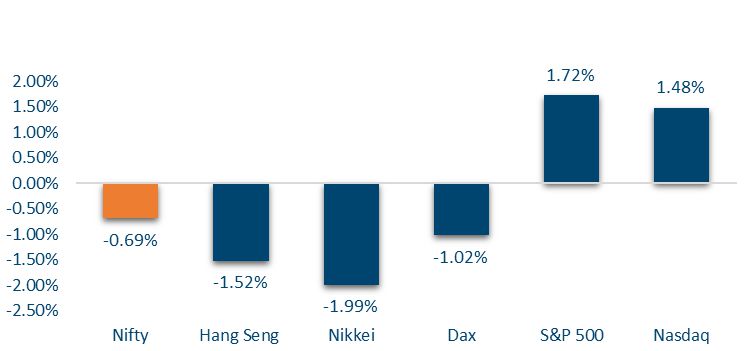

NIFTY V/S GLOBAL MARKETS

Global equities saw mixed performance this week. The S&P 500 led gains with a 2.2% rise, while Straits also posted a solid 1.2% uptick. In contrast, European and Asian indices like DAX, Nikkei, and Hang Seng declined, reflecting regional divergences.

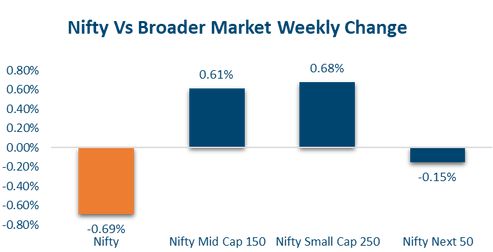

Domestic Equities

Benchmark indices had a mixed week, with Nifty50 declining by 0.7%, while midcaps and small-caps rose 0.5% and 0.7% respectively. Among sectors, Pharma (+2.1%), Oil & Gas (+1.6%), and IT (+0.9%) outperformed, whereas Realty (-2.2%) and FMCG (-0.7%) lagged. Valuations remain elevated, with Nifty50 trading at 23.3x trailing and 21.6x forward PE, while midcaps and small-caps are even higher. The number of advancing stocks in Nifty50 ranged between 20 and 31throughouth the week, indicating broad-based but selective participation.

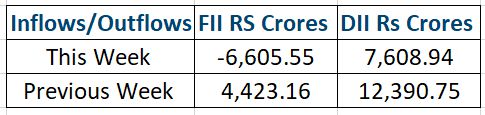

In terms of factors, liquidity and value outperformed while Growth and market cap underperformed. FPIs have sold a net of USD 166mn in the first few sessions of July so far.

FIXED INCOME

US 10y yield had gone down to 4.23% but ended the week 11bps higher at 4.35%. 2y yield ended 16bps higher at 3.88%

UK 10y Gilt yield rose 7bps this week to 4.55%

Yield on the India benchmark 10y ended 2bps lower at 6.295%

1y and 5y OIS both ended 3bps lower at 5.68% and 5.50% respectively

10y AAA PSU spreads are around 55bps and 10y AAA NBFC spreads are around 95bps

RBI sucked out Rs 1 lakh crs through a 7 day VRRR. Event post that the system liquidity is in excess of Rs 2 lakh crs. Overnight Call rates have again been fixing closer to SDF rate, around 5.30%

FPIs have bought USD 1.2bn of domestic debt in the first few sessions of July

PRIVATE EQUITY & VENTURE CAPITAL

Private equity and venture capital funding for Indian companies fell sharply this week, with startups raising a total of $294 million across 26 deals—down from $428 million across 30 deals in the previous week. The decline was largely due to a lack of big-ticket transactions, with most activity focused on early-stage investments across sectors. Only one deal crossed the $100 million mark.

The largest funding deal of the week was Jumbotail’s $120 million Series D round led by SC Ventures, with participation from existing backers like Artal Asia. This funding pushed Jumbotail’s valuation to $1 billion, earning it unicorn status.

In contrast, M&A space saw a notable surge. The number of M&A deals more than doubled to nine from just four last week, driven by strategic plays by listed companies. Torrent Pharma’s planned acquisition of a 46.39% stake in JB Chemicals from KKR for ₹11,917 crore marked one of the largest pharma deals in India.

INITIAL PUBLIC OFFERING (IPO)

Indian IPO markets continue to show strong momentum in 2025, with nearly 70% of the 26 mainboard listings trading above their issue price. Several offerings have delivered double-digit returns, with standout performers like Quality Power and Quadrant Future Tek gaining 75% and 63%, respectively, from their debut levels. This reflects sustained investor enthusiasm, particularly for companies with strong fundamentals and growth narratives.

Looking ahead, the IPO pipeline remains active. Smartworks, a major flexible workspace provider, will launch its ₹445 crore issue between July 10 and 14. The company, which has seen its revenue surge to ₹1,374 crore in FY25, is aiming to capitalize on growing demand for managed office spaces. Travel Food Services, another mainboard player, will also open its issue next week with a price band of ₹1,045–1,100.

In addition to mainboard offerings, the SME segment is buzzing with activity. Firms such as Chemkart India, Smarten Power Systems, GLEN Industries, and Asston Pharmaceuticals are set to launch IPOs, while nine new listings are lined up for debut. This broad-based momentum highlights investor confidence across market segments and sectors.

REAL ESTATE

India’s real estate sector witnessed key regulatory and acquisition developments this week. SEBI imposed penalties on Essel Finance’s second real estate private equity-style fund—India Asset Growth Fund-II —for breaching AIF regulations. The fund had invested nearly 43% of its corpus in a single company, Samruddhi Realty Ltd, significantly exceeding the 25% investment cap set by SEBI. In response, SEBI levied a fine of ₹12 lakh on the fund and an additional ₹12 lakh on its manager, Essel Finance Advisors and Managers, along with key executives.

Meanwhile, Adani Properties secured approval from the National Company Law Tribunal (NCLT) to acquire major assets of Housing Development and Infrastructure Ltd (HDIL) under the insolvency process. This acquisition marks a significant step in Adani’s growing presence in real estate, allowing the conglomerate to gain control of HDIL’s key land parcels and development rights. The move is expected to accelerate Adani’s plans in the urban development and housing sector.

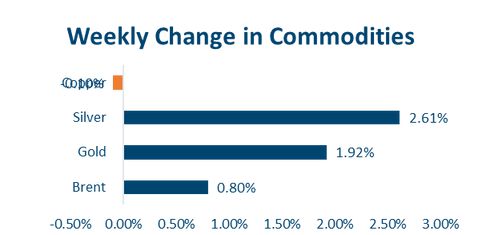

COMMODITIES

Commodities had a mixed week. Brent Crude edged up by 0.8%, while U.S. natural gas prices saw a sharp decline of 8.9%. Industrial metals like aluminum and copper remained largely flat. Precious metals outperformed, with gold gaining 1.9% and silver rising 2.7%.

FOR EXPORTERS

Option strategy, Spot ref 85.40, Atmf level 86.17

Exporter seagull, Tenor 6m, Buy put atmf, Sell put of 83.70, Sell call of 87.00

Net zero cost

FOR IMPORTERS

Option strategy, Spot ref 85.40, Atmf level 85.75

Importer risk reversal, Tenor 3m, Buy call 86.15, Sell put atms

Net zero cost

Our Views: What we Like?

Equities

Nifty50 might see strong support around 25120 in the near term. Till the time that support holds, fresh all-time highs are in play.

We believe valuations in the large-cap space are relatively much more comfortable than mid and small-caps from a long-term investment perspective.

Bonds & Rates

In a contrarian call, we prefer buying USTs and receiving rates at current levels

We see the yield on the 10y trade in a 6.20-6.40% band over the medium term.

We believe these are attractive levels to pay 5y OIS.

Commodities

China is aggressively ramping up its production of base Metals.

Commodities may continue to remain supported on a weaker Dollar.

Brent should be steady in a USD 65-75 per barrel range over the next 3 months or so.

FX

We expect the Dollar to continue to weaken against DM currencies. It may not weaken to the same extent as EM currencies