Billionz Global Newsletter

Global Developments & Global Equities

RECIPROCAL TARIFFS ANNOUNCED; INDIA ESCAPES LIST

Trump announced reciprocal tariffs on countries with whom trade negotiations were stalling. This included 50% tariff on Brazil and 35% on Canada.

India does not feature in that list. However there is a bill introduced by 2 Senators which proposes 500% tariffs on imports from countries that purchase Crude from Russia. Trump is however not happy with the bill in its current form.

Trade talks with India are ongoing and we can expect a mini trade deal to be signed by 31st July wherein the tariff rate could be lower than 20%, a rate that would be more favorable compared to other countries in the region. However threat of participation in BRICS could result in an additional 10% tariff.

Developments around tariffs will continue to be monitored closely. Market is pricing in 2 cuts by the Fed till end of 2025.

US June CPI print will be the key data to look forward to in the coming week

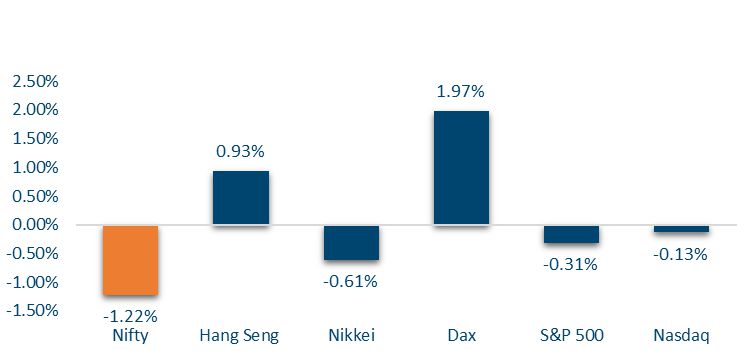

NIFTY V/S GLOBAL MARKETS

Global equities saw mixed movements this week. While European and Asian indices like DAX (+2%), CAC (+1.7%), and Jakarta (+2.7%) posted strong gains, US and Japanese markets showed mild declines with the S&P 500 down 0.3% and Nikkei slipping 0.6%. Notably, South Korea’s Kospi surged 4%, leading regional performance.

Domestic Equities

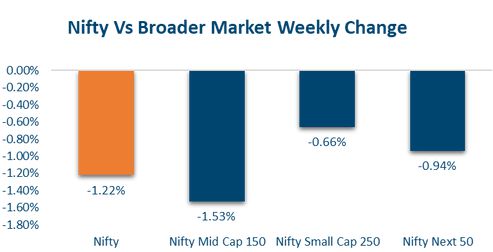

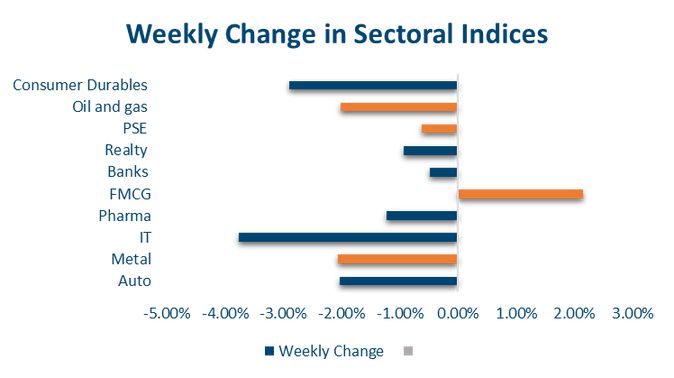

Weekly Market Wrap-Up & Valuation Snapshot: Domestic equities ended the week in the red, with the Nifty50 down 1.2%, led by broader market underperformance—Midcap100 fell 1.7% and Smallcap250 slipped 0.7%. Most sectoral indices declined, with IT (-3.8%), Consumer Durables (-2.7%), and Metals (-2.1%) taking the biggest hit. FMCG stood out with a 2.2% gain, signaling defensive buying. In terms of valuations, mid and small caps remain richly priced, with trailing PEs at 33.5x and 31.5x, respectively, significantly above the Nifty50’s 23x, suggesting relatively higher risk premiums in the broader markets.

IT stocks were down this week as the Earnings season kicked off with TCS Q1 Revenue missing estimates.

AUM of MFs reached a record high of Rs 74 lakh crs in June as per AMFI data. Investments through SIPs reached an all time high of Rs 27300crs. Investments into Equity MFs rose 24% MoM to Rs 23500crs

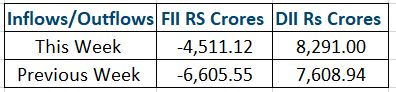

FPIs have invested net USD 447mn in domestic Equities in July so far

INVIX at 11.82 has dropped to the lowest level in one year

In terms of factors, value underperformed while Growth outperformed this week.

FIXED INCOME

Yield on the US 10y treasury was up 3bps at 4.41%. US 2y yield ended 1bps lower at 3.89%

10y yields across Eurozone were up 6-9bps

Yield on the benchmark India 10y ended flat at 6.30%

Banking system liquidity continues to be in surplus. RBI sucked out Rs 150000crs for 7 days through VRRR. Overnight call fixings moved higher steadily through the week from 5.30% to 5.50%. Weighted average TREPS rate also moved higher from around 5% to 5.25%

1y OIS ended 4bps higher at 5.54% and 5y OIS ended 2bps higher at 5.70%

10y AAA PSU and NBFC spreads are 55bps and 85bps respectively

FPIs have invested close to USD 1bn in domestic debt in July so far

PRIVATE EQUITY & VENTURE CAPITAL

Private equity and venture capital activity in India slowed in terms of deal volume last week, with 18 transactions compared to 26 in the previous week. However, overall investment rose slightly to $312 million from $294 million, primarily driven by a large-ticket deal.

The standout PE transaction was Swiss firm Partners Group acquiring a majority stake in Infinity Fincorp for $230 million. This deal also saw participation from Jungle Ventures, while True North made a complete exit, marking the biggest deal of the week.

In mergers and acquisitions, deal count fell to five from nine, though the disclosed deal value rose to $3.3 billion from $2.8 billion. The highlight was Capgemini’s $3.3 billion takeover of WNS, an Indian IT outsourcing company listed in New York.

INITIAL PUBLIC OFFERING (IPO)

India’s IPO market remained active with key listings and fresh issues. Travel Food Services closed its 2,000 crore offer and is set to list on July 14 after strong institutional interest. Smartworks Coworking Spaces, which saw moderate demand, will debut on July 17 with a small premium expected in grey markets.

The upcoming week will see the launch of Anthem Biosciences’ ₹ 3,395 crore IPO, a major offer-for-sale backed by True North, opening July 14. Several SME IPOs, including Spunweb Nonwoven and Glen Industries, are also scheduled, highlighting investor appetite in niche sectors.

Multiple SME listings like Chemkart, Smarten Power, and Glen Industries are expected this week, keeping momentum strong in the primary market. While mainboard action is selective, overall activity reflects robust interest across sectors like biotech, coworking, and manufacturing.

REAL ESTATE

Neo Asset Management, the investment arm of Neo Group backed by Peak XV Partners and MUFG Bank, has successfully closed its first infrastructure fund, raising around ₹ 2,300 crore—about 15% above its initial target. The fund, NIIOF, had aimed for ₹ 800 crore with a ₹ 1,200 crore greenshoe option and has already completed its first infrastructure acquisition after receiving NHAI approval.

Meanwhile, TVS Emerald, the real estate wing of TVS Holdings Ltd, is set to receive up to ₹ 428 crore from the International Finance Corporation (IFC) to support middle-income housing projects in Chennai and Bengaluru. IFC’s investment, through rupee denominated NCDs, will be routed via three TVS Emerald subsidiaries to partially fund the planned developments.

COMMODITIES

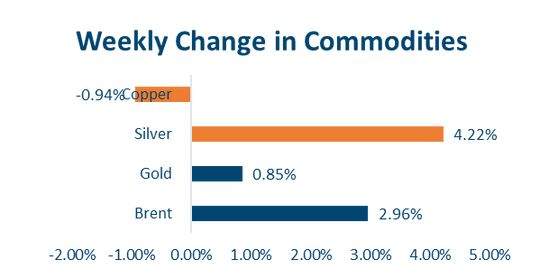

This week saw mixed trends across major commodities. Brent crude rose 3% on continued supply concerns, while US natural gas fell nearly 3% amid easing demand. Industrial metals showed divergence — Aluminium remained flat, LME Copper dipped 2.1%, but COMEX Copper surged 9% after Trump’s announcement of 50% tariffs on copper imports, triggering supply fears. Precious metals gained, with Silver up 4% and Gold steady, indicating a mild risk-off sentiment in markets.

Option Strategies

EXPORTER OPTION STRATEGY (KIKO)

Spot ref 85.8, Atmf level 86.65, Tenor 6m, Buy put atmf with eko at 83.10, Sell call Atmf with eki at 90.00, Net zero cost

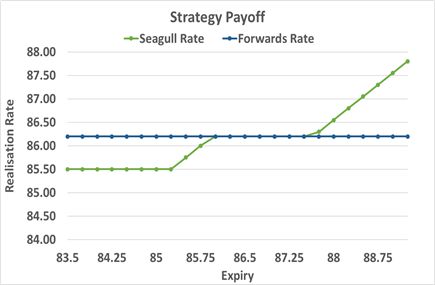

IMPORTER OPTION STRATEGY (SEAGULL)

Spot ref 85.86, Atmf level 86.20, Tenor 3m, Buy call atmf Sell put 85.50, Sell call 87.90, Net zero cost

Our Views: What we Like?

Equities

Nifty50 ended the week at a crucial support level of 25100.

We maintain our medium-term bullish outlook and will wait for a weekly close below 25100 to change that view.

We are advising clients to avoid the Midcap and Smallcap space from a long-term perspective, as current valuations are expensive.

Bonds & Rates

We expect the benchmark 10y yield to continue trading in a 6.20%-6.40% range.

We expect the RBI to withdraw Banking system liquidity on a medium term basis than just overnight. This could cause overnight rates to harden and remain close to Repo instead of SDF.

Those with floating-rate liabilities can look to convert to fixed by paying 5y OIS.

FX

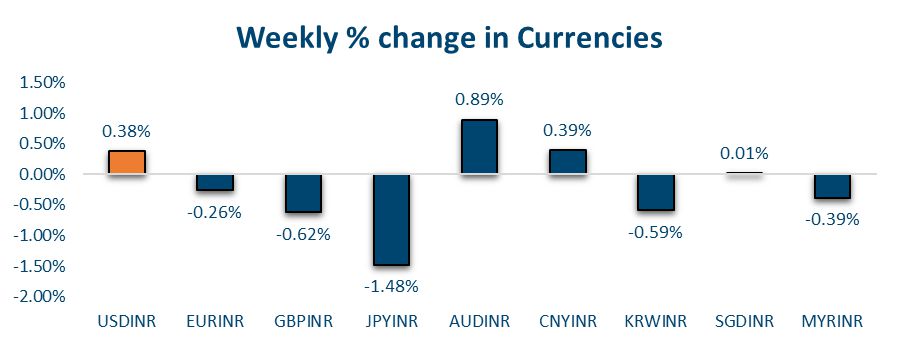

The dollar saw some recovery this week. However, we believe the overall downtrend is still intact.