Billionz Global Newsletter

Global Developments & Global Equities

DISAPPOINTING US NFP PRINT TRIGGERS RISK OFF; DOMESTIC ASSETS

SPOOKED BY HIGHER THAN EXPECTED TARIFF RATE

The Fed kept rates unchanged this week, along expected lines. However there were 2 Fed members who dissented (first time since 1993 that 2 members dissented) and voted in favor of a 25bps cut.

US NFP print disappointed. It came in at 73k against expected 104k. This turned the risk sentiment around. US treasury yields came off sharply, Dollar weakened, Equities plunged and Brent retraced.

After Friday’s move, Market is now pricing in 2.5 cuts by the Fed until end of 2025. Sep rate cut is now almost fully priced in

Key event to look forward to in the coming week will be the RBI monetary policy on Wednesday and BoE rate decision on Thursday

NIFTY V/S GLOBAL MARKETS

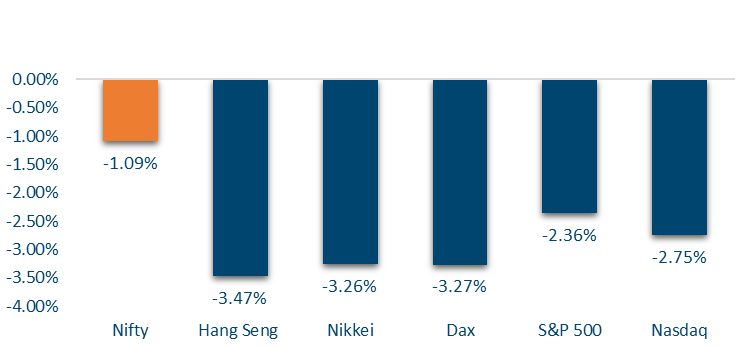

Global equity markets witnessed a broad-based decline this week, led by steep losses in European indices. France’s CAC dropped 3.7% and Germany’s DAX fell 3.3%, reflecting investor caution. Asian markets were also in the red, with Hong Kong’s Hang Seng down 3.5% and Japan’s Nikkei slipping 1.6%. The U.S. S&P 500 declined by 2.4%, while Jakarta was relatively resilient with a marginal 0.1% dip.

Domestic Equities

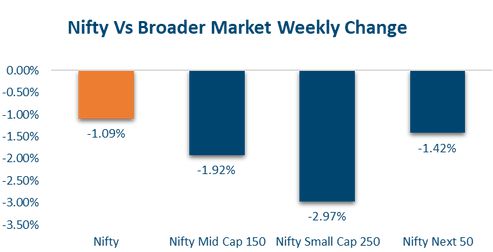

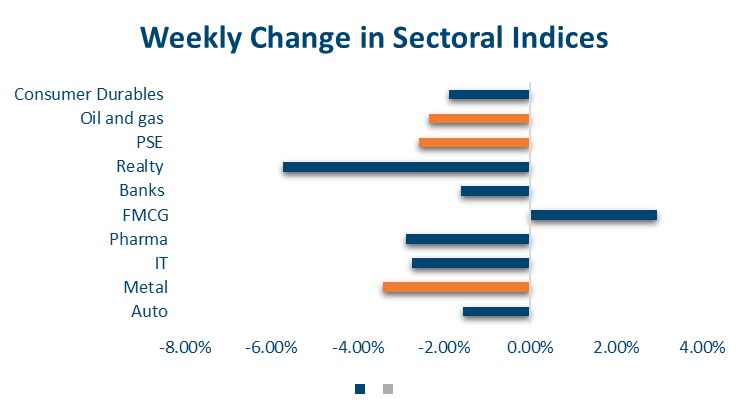

Equity markets ended the week on a negative note, with the Nifty down 1.1%, Midcap100 falling 2.4%, and Smallcap250 sliding 3%. Sectoral losses were led by Realty (-5.7%), Metals (-3.4%), Pharma (-2.9%), and IT (-2.7%), while FMCG stood out with a 3% gain. Bank Nifty, Auto, and Oil & Gas also posted declines of around 1.6%–2.8%. In terms of valuations, the Nifty50 is trading at a trailing PE of 21.9 and forward PE of 20.5, while mid and small caps remain relatively expensive with PEs of 32.4/28.3 and 30.0/27.0 respectively.

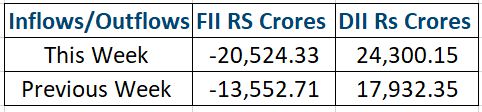

FPIs pulled out USD 2bn from domestic Equities in July

In terms of factors, low volatility and quality outperformed while value and liquidity underperformed

More than half of the NSE500 companies have reported Q1FY26 Earnings. The average Revenue surprise has been 5.5% and Earnings surprise 1%

Fixed Income, IPO and Institutional Deals

INITIAL PUBLIC OFFERING (IPO):

Over the past week, the IPO pipeline witnessed notable developments. NSDL kicked off its ₹4,012 crore offer (pure OFS) from July 30 to August 1 and was fully subscribed on Day 1. By the close, the issue was booked over 41 times. Grey market premiums hovered around 16–17%, indicating strong listing momentum ahead of its August 6 debut.

Looking ahead, Aditya Infotech is set to launch a ₹1,300crore IPO between ₹640–675 per share, with a robust 30% grey market premium suggesting solid investor interest.

Additionally, JSW Cement plans to launch its ₹4,000crore IPO from August 7–11, while Highway Infrastructure and several SME issues will come to market next week—part of a busy IPO calendar featuring over 15 listings across mainboard and SME segments.

PRIVATE EQUITY & VENTURE CAPITAL:

Private equity and venture capital deal activity continued to weaken for the second straight week, with just 19 transactions totaling $152 million— marking the lowest in three months. This drop from $215 million across 24 deals last week was largely due to the absence of any large-ticket transactions above $100 million.

The top deals included SUN Mobility’s $60 million raise from Helios Investment Partners and Infraco Asia, and Jashvik Capital’s $46 million investment in Marg ERP—together accounting for over 74% of the total. Most other deals were early-stage, sub-$10 million rounds, featuring companies like Metaforms, STAN, and SixSense.

On the M&A front, activity surged past $4.4 billion, driven almost entirely by Tata Motors’ $4.3 billion acquisition of Italian commercial vehicle maker Iveco. Iveco also agreed to sell its defense division to Leonardo, marking a strong week for strategic global deals.

REAL ESTATE:

Blackstone-backed Knowledge Realty Trust REIT, in partnership with Bengaluru-based Sattva Group, has trimmed its IPO size to ₹4,800 crore ($548 million) after raising ₹1,400 crore in a pre-IPO round. The REIT, which originally planned to raise ₹6,200 crore, will open its offering on August 5. Of the revised amount, ₹1,200 crore will come from 13 strategic investors, including major names like LIC (₹300 crore), SBI Life (₹200 crore), UTI AMC (₹175 crore), and 360 One (₹150 crore), among others.

Separately, real estate developer Omaxe Ltd has raised ₹500 crore ($57.5 million) via non-convertible debentures from Oaktree Capital Management. The company will use the funds to speed up project execution across its residential, commercial, and PPP developments in North India. According to MD Mohit Goel, the funding will support construction, reduce market-linked risks, and expand the company’s footprint in high-growth cities.

FIXED INCOME:

US 10y yield dropped 16bps to 4.22% while 2y yield dropped 28bps to 3.68% this week

10y yields across Eurozone were down 1-4bps and that in Japan was almost flat

Yield on the benchnark India 10y rose 2bps to 6.37%

1y OIS ended 3bps lower at 5.50% and 5y ended 2bps lower at 5.715%

10y AAA PSU and NBFC spreads over Gsces are 51bps and 86bps respectively

1y T-bill is at 5.53%, 1y CD at 6.21% and 1y NBFC CP at 6.55%

FPIs invested USD 1.3bn in domestic debt in July.

COMMODITIES:

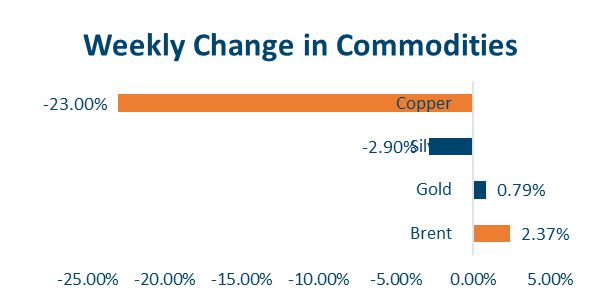

Comex Copper prices plunged 23% — the biggest single-day drop — after Trump clarified that the 50% import tariff applies only to semi-finished copper, not refined metals. Brent crude fell 3% on Friday amid post-NFP risk aversion. For the week, Brent gained 1.8% to $69.7, while US natural gas dipped 0.9%. LME aluminum and copper slipped 2.6% and 1.4% respectively. Gold edged up 0.8%, while silver dropped 2.9%.

Our Views: What we Like?

Equities

We continue to stick to large-cap space and select midcaps from a long-term portfolio construction point of view. Technically, Nifty50 forming a higher bottom this time at 24404 (previous 24337) is an encouraging sign. A break above 25200 could bring 25700 first, and subsequently, all-time highs back into play.

Bonds & Rates:

We expect the Yield On the 10y to remain steady in 6.30-6.45% We believe around 6.45-6.50% would be good levels to add duration to portfolio again. 5y OIS levels are currently attractive to pay

Commodities:

We remain constructive on precious metals and believe they present a good buy on dips opportunity. We are more bullish on Silver than Gold. We are neutral on Brent and Base Metals.

FX:

We expect the Dollar to weaken against Majors. Dollar strength this week has likely cleansed out weak short Dollar positions.