Billionz Global Newsletter

Global Developments & Global Equities

TRUMP PENALTY WEIGHS ON RUPEE, EQUITIES

President Trump announced a 25% penalty on Indian imports for India’s purchases of Russian crude. The Indian government has said that targeting India is unfair, unjustified, and unreasonable. The tariffs are likely to impact 1% India’s GDP,i.e.. USD 40bn and affect the GDP growth rate by 0.3 percentage points.

The RBI kept the repo rate unchanged this week through a unanimous vote, opting to remain in a wait-and-see mode. It maintained the GDP growth estimate for FY26 at 6.5% and lowered the inflation projection to 3.1% from 3.7%

The US July CPI print will be the key data to look forward to in the coming week

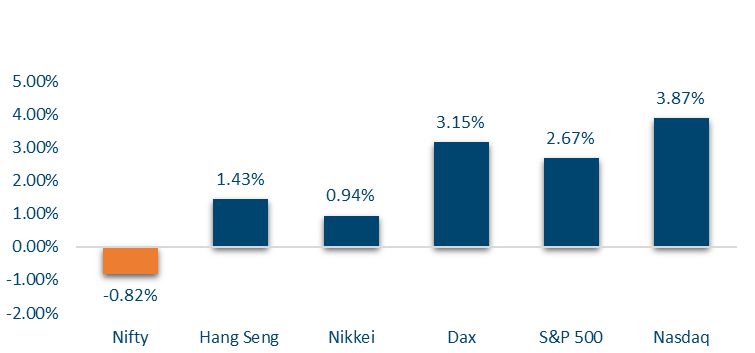

NIFTY V/S GLOBAL MARKETS

Global equities posted strong gains this week, with European indices leading—DAX up 3.2% and CAC up 2.6%. The S&P 500 rose 2.4%, while Asian markets also advanced, including Nikkei (+2.5%), Kospi (+2.9%), and Hang Seng (+1.4%). The Straits Times gained 2.1%, and FTSE saw a modest 0.3% rise. Jakarta was the only major index to slip, edging down 0.1%.

Domestic Equities

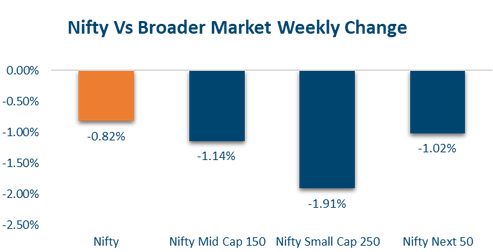

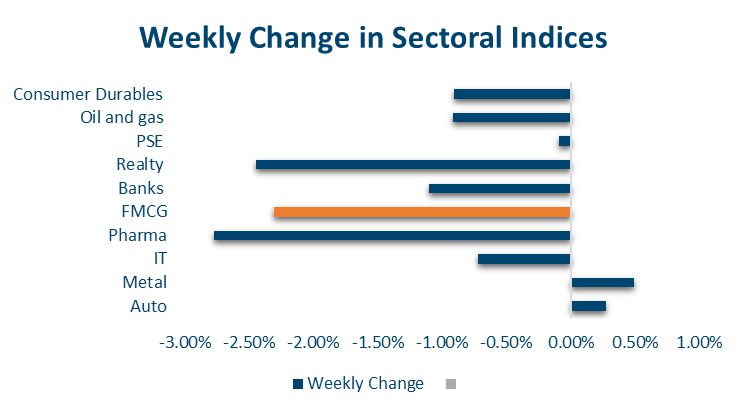

Indian equities fell this week, with the Nifty50 closing below the 24,500 mark, down 0.8%. Midcap100 and Smallcap250 declined 1.1% and 1.9% respectively. Valuations remain elevated, with Nifty50 trading at 21.6x trailing and 20.5x forward PE, Midcap100 at 31.1x/28x, and Smallcap250 at 29.3x/27.1x. Sectorally, Pharma (-2.8%), Realty (-2.5%), and FMCG (-2.3%) led the declines, while Metals (+0.5%) and Auto (+0.3%) posted modest gains.

INVIX ended the week at 12.03, still quite suppressed despite a key support having been broken

Most of the Nifty50 Q1 earnings have been reported. Average Sales surprise has been 5.2% and Eanrings surprise 2.1%

In terms of factors, liquidity, low volatility and growth underperformed while value and dividend yield outperformed

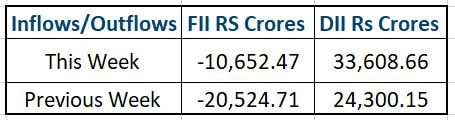

FPIs have sold net USD 2bn of domestic equities in the first few sessions of August

Fixed Income, IPO and Institutional Deals

INITIAL PUBLIC OFFERING (IPO):

The coming week will be active for India’s primary markets, with four IPOs opening for subscription and eleven companies set to list. Mainboard offerings include BlueStone Jewellery & Lifestyle, aiming to raise ₹1,540.65 crore, and Regaal Resources, targeting ₹306 crore, alongside two SME issues, reflecting strong investor interest.

BlueStone’s IPO is priced at ₹492–₹517 per share with a lot size of 29 shares, while Regaal Resources is priced at ₹96–₹102 with a lot size of 144 shares. Both combine fresh share sales with offers for sale to fund expansion, working capital, and debt reduction. Several SME IPOs will also open, catering to niche markets.

On the listing side, JSW Cement, Highway Infrastructure, All Time Plastics, and other SME players will debut. The combination of new issues and multiple listings points to a buoyant IPO market supported by robust secondary market sentiment and steady investor inflows.

PRIVATE EQUITY & VENTURE CAPITAL:

Private equity and venture capital activity rebounded in the week ending August 8 after two weeks of slowdown. Thirty-three companies raised $209 million, up from $152 million by 19 firms a week earlier—a 37.5% jump in deal value.

The top three deals accounted for over half the funding, led by The Sleep Company’s $54.7 million Series D from ChrysCapital, Renee Cosmetics’ $30 million round led by Playbook Partners, and a $23 million investment in CORE Energy by Pankaj Prasoon and Ashish Kacholia.

M&A activity fell sharply below $100 million amid the absence of large deals, unlike last week’s boost from Tata Motors’ Iveco transaction. Key deals included Oyo’s $50 million acquisition of MadeComfy, marking its Australia–New Zealand entry, and Vasa Denticity’s $15 million purchase of IDS Denmed, valuing it under $30 million.

REAL ESTATE:

International Finance Corporation (IFC) has committed up to $150 million as an anchor equity investor in HDFC Capital’s H-DREAM fund, targeting a $1 billion corpus (including a $500 million greenshoe). The fund will invest in affordable and mid-income housing projects while adopting IFC’s EDGE green building framework to align with global sustainability standards.

Meanwhile, Singapore-based CapitaLand Investment is planning an India-focused private equity fund dedicated to data centre assets. With four data centre projects already underway, the company aims to expand its footprint in this high-growth segment, according to Gauri Shankar Nagabhushanam, CEO of CapitaLand India Trust.

FIXED INCOME:

US 2y yield rose 9bps to 3.76%

US 10y yield rose 9bps this week to 4.28%. Yields across. 10y Yields across Eurozone and UK were up between 5-10bps

Yield on the benchmark India 10y rose 4bps to 6.41% this week.

10y AAA PSU spreads are around 47bps and 10y AAA NBFC spreads are around 100bps

Yield on the 1y OIS rose 5bps to 5.50% and that on 5y OIS dropped 4bps to 5.67%. Overnight call rate fixing happened at 5.63% on Friday. Earlier in the week it had been in 5.39-5.50% range.

FPIs have invested net USD 500mn in domestic debt in August so far.

COMMODITIES:

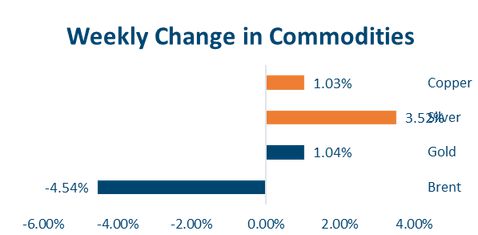

Brent crude fell sharply by 5.1% to USD 66.6, while industrial metals saw modest gains, with LME Aluminum up 1.7% to USD 2609 and LME Copper up 1.4% to USD 9762. Precious metals also advanced, as gold rose 1% to USD 3397 and silver gained 3.5% to USD 38.3. Overall, commodities posted mixed performance, with energy under pressure and metals trending higher. Brent saw the biggest weekly decline since June as Trump’s tariffs took effect. This is weighing on global growth outlook.

Our Views: What we Like?

Equities:

Now that 24500 has broken, we could see the Nifty50 come under pressure over the next few sessions. A move lower to 24150 and 23700 is likely.

Outlook is likely to be dampened on account of uncertainty emanating from the US-India trade war. Earnings, to,o have been a bit so, ft which makes lofty valuations, especially in the Midcap space, unsustainable.

We prefer sticking to the large cap space from a long-term investment horizon standpoint.

Bonds & Rates:

Domestic Bonds came under pressure on a hawkish MPC. Credit spreads have also been widening.

We believe close to 6.45-6.50% on the 10y would be good levels to add duration to the portfolio.

Commodities:

We see Brent trade in a USD 60-70 per barrel range over the medium term.

Precious metals could continue to remain supported amid Dollar weakness and global risk aversion.

FX:

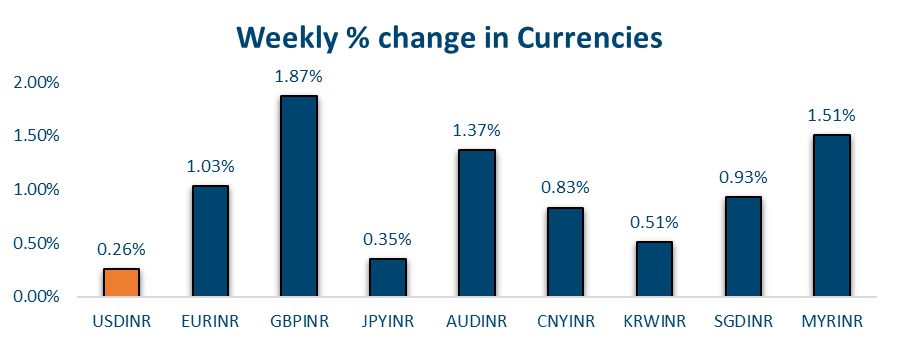

We expect the Dollar to continue weakening against majors.