Billionz Global Newsletter

Global Developments & Global Equities

VOLS DROP AS EERIE CALM PREVAILS ACROSS ASSETS CLASSES

Trump said this week that it is doubtful that he will fire Fed Chair Powell

US Headline and core CPI were mostly in line with expectations, while Retail sales beat estimates.

Market is pricing in 1.8 cuts by the Fed till end of 2025, i.e., 46bps and 4.8 cuts by end of 2026.

Markets are awaiting the July end deadline for trade negotiations, after which it will become clear what the tariff rates are going to be for major US trade partners.

The ECB rate decision is due in the coming week. ECB is expected to keep deposit rates on hold at 2%.

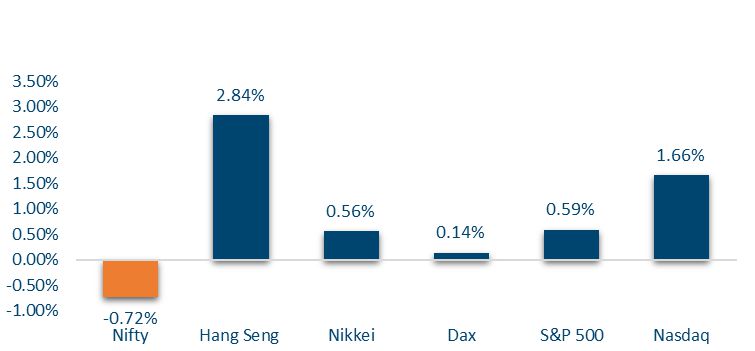

NIFTY V/S GLOBAL MARKETS

Global equity markets ended the week on a mixed note. The U.S. S&P 500, UK’s FTSE, and Japan’s Nikkei all gained 0.6%, reflecting investor optimism around earnings and a resilient economic outlook. Asian markets outperformed, with Jakarta (+3.8%), Hang Seng (+2.8%), and Straits (+2.5%) leading the rally, possibly driven by strong domestic flows and bargain hunting. Meanwhile, European indices like CAC (-0.1%) and DAX (+0.1%) remained largely flat, signaling cautious sentiment amid lingering growth concerns.

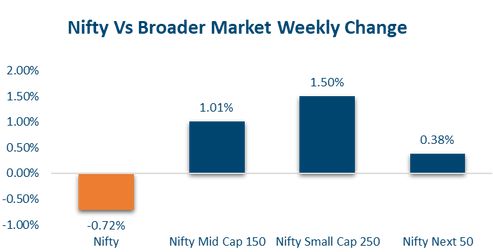

Domestic Equities

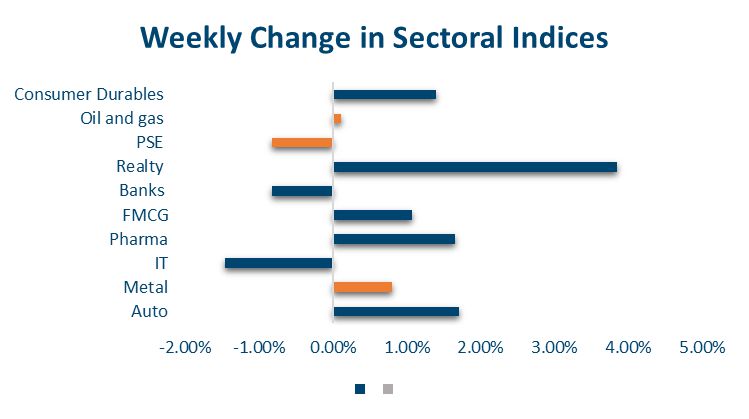

This week, broader markets outperformed frontline indices — while Nifty50 declined 0.7%, the Smallcap250 and Midcap100 gained 1.5% and 0.8% respectively. Sectorally, Realty led the rally with a 3.8% jump, followed by Auto and Pharma at 1.7% each, while IT and Bank Nifty saw mild corrections.

Valuation-wise, Nifty50 remains relatively moderate with a trailing/forward PE of 22.9/21.1. However, elevated valuations in mid and small caps (Midcap100: 33.8/29.5, Smallcap250: 32.1/28.3) suggest investor exuberance and potential caution ahead if earnings don’t catch up.

In terms of factors, Dividend yield and value outperformed while momentum and market cap underperformed

Out of the 11 out of 50 Nifty50 companies that have reported Earnings so far, the sales surprise has been 3.6% and Earnings surprise has been 7.9%

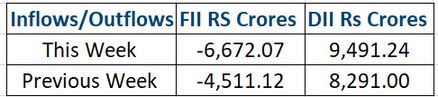

FPIs have sold net USD 643mn of domestic Equities in July so far

FIXED INCOME

Yield on the US 2y ended 3bps lower at 3.87% while the Yield on the US 10y ended 2bps lower at 4.42%

UK 10y yield rose 7bps to 4.67% this week while Yields on 10y Bonds of other European countries were down 3-4bps this week

Yield on the benchmark 10y ended almost flat at 6.306%. Domestic CPI print came in at 2.1% against expected 2.25% yoy

PSU 10y AAA G-spread is 66bps, NBFC 10y AAA is around 85bps and Corporate AAA spreads are around 92bps

RBI mopped up Rs 2 lakh crs through a 7 day VRRR on Friday (rolling over the maturing one). Overnight call fixings happened in 5.38-5.44% range this week.

1y OIS ended 4bps lower at 5.50% while 5y OIS ended unchanged at 5.70%

FPIs have invested net USD 1.3bn in domestic debt in July so far.

PRIVATE EQUITY & VENTURE CAPITAL

After a two-week lull, private equity and venture capital activity rebounded sharply in the week ending Friday, with 29 companies securing funding—up from 18 the previous week. Total funding surged over 50% to $474 million, largely fueled by big-ticket investments. The top two deals alone contributed around 80% of the total capital raised.

The largest deal saw Multiples PE, alongside Enam Group’s Akash Bhanshali and CaratLane founders Mithun and Siddhartha Sacheti, acquire a 32% stake in VIP Industries from promoter Dilip Piramal and family—marking a significant shift in the company’s ownership structure.

Meanwhile, mergers and acquisitions remained subdued with just five deals. A standout transaction involved a consortium led by Oberoi Realty acquiring debt-laden Hotel Horizon under insolvency proceedings, marking a full settlement of all outstanding dues and claims.

INITIAL PUBLIC OFFERING (IPO)

India’s IPO market is set for a busy week, with eight new issues opening for subscription and four listings scheduled. Notable mainboard IPOs include Indiqube Spaces, GNG Electronics, and PropShare Titania REIT, while SME offerings from Swastika Castal, Savy Infra, and others highlight activity across segments. Investors are also eyeing upcoming launches from NSDL and Brigade Hotels.

In the first half of 2025, India raised $4.6 billion from 108 IPOs, ranking among the most active global markets. Industrial sector listings led in volume, and sustained investor interest was supported by strong corporate earnings and economic momentum.

With a robust pipeline and active institutional participation, India’s IPO market remains resilient. Despite a slight dip in deal count, diverse sector representation and steady demand underscore long term market confidence.

REAL ESTATE

Embassy Office Parks REIT is negotiating with bankers to raise 20 billion rupees ($232.79 million) by issuing five-year corporate bonds, aiming to complete the transaction before the end of the month, according to sources familiar with the matter. The bonds are expected to attract considerable interest from mutual funds and insurance companies, supported by a top tier ‘AAA’ rating from Crisil.

This marks Embassy REIT’s second bond market outing this year, following its June placement of 7.5 billion rupees in 21-month bonds that carried a 6.9650% coupon, paid quarterly. The company is opting for a longer bond tenor this time to appeal to insurance investors as it seeks a higher funding amount.

COMMODITIES

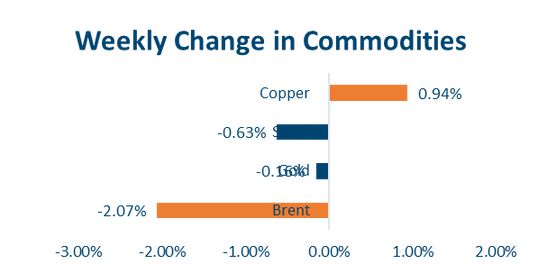

Commodity markets showed mixed trends. Crude prices slipped, with Brent down 1.5% to $69.3, reflecting weak demand sentiment. In contrast, US Natural Gas surged 7.5%, likely driven by weather related demand spikes or inventory data. Industrial metals like aluminum (+1%) and LME copper (+1.2%) gained on hopes of stronger global manufacturing activity. Meanwhile, precious metals saw mild corrections, with gold and silver down 0.2% and 0.6% respectively, amid stable dollar and yield moves.

Option Strategies

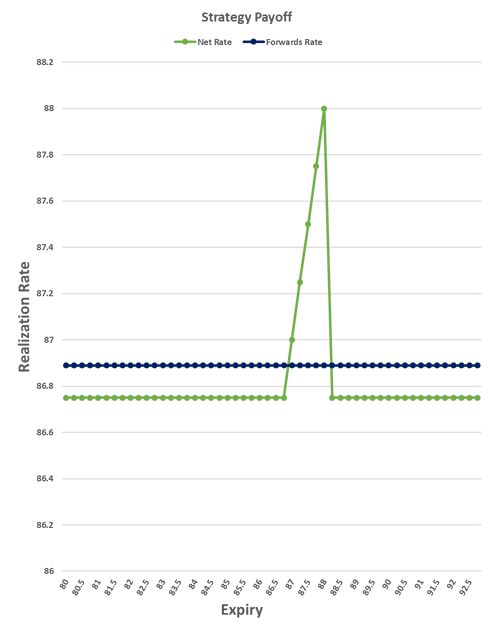

EXPORTER OPTION STRATEGY (KIKO)

Exporter strategy, Tenor 6m, Spot ref 86.13, Atmf 86.89

Buy put 86.75, Sell call 86.75, with eki at 88.10

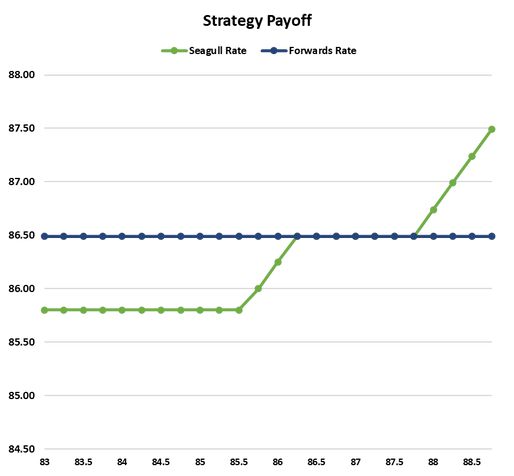

IMPORTER OPTION STRATEGY (SEAGULL)

Importer strategy, Tenor 3m, Spot ref 86.13, Atmf 86.49

Buy call Atmf, Sell put 85.80, Sell call 88.00

Our Views: What we Like?

Equities

Q1 earnings will be closely tracked. Valuations in the Midcap and Smallcap space are elevated, and any Earnings misses could result in a correction.

We prefer to stick to the Nifty50 space to build a long-term investment portfolio

Bonds & Rates

We expect yields on the benchmark 10y Gsec to remain steady.

Those with floating-rate liabilities can consider hedging at current levels by paying fixed OIS

We could, however, see widening of SDL and Corporate Bond spreads.

Commodities

We are mildly bullish on base Metals and neutral on Brent

Among Precious metals, we are more bullish on Silver compared to Gold. Silver could advance to beyond USD 40 levels soon

FX

We expect the Dollar to weaken against majors and remain steady against EM currencies.