Billionz Global Newsletter

Global Developments & Global Equities

DIRECT US INVOLVEMENT IN IRAN-ISRAEL CONFLICT MAY ESCALATE THE GEOPOLITICAL TENSIONS FURTHER

Iran-Israel conflict continues to keep markets on the edge. The U.S. military carried out massive precision strikes on the three key nuclear assemblies in the Iranian regime: Fordo, Natanz and Isfahan.

All 3 central Banks Fed, BoE and BoJ left rates unchanged this week. Fed dot plot is indicating 2 cuts by the end of the year. Fed Chair Powell highlighted uncertainty over economic Outlook. Market is also pricing in 2 cuts by the Fed till end of 2025.

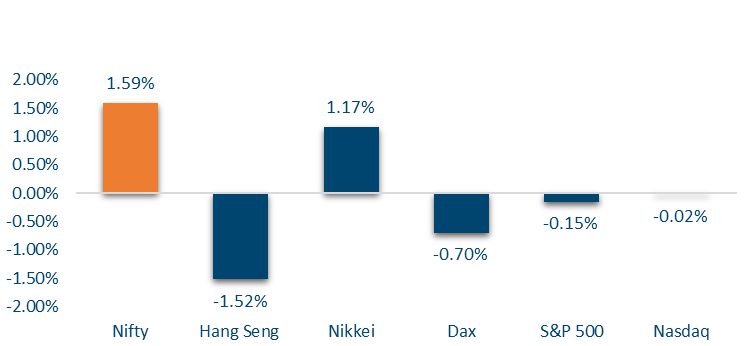

NIFTY V/S GLOBAL MARKETS

Global equities saw mixed performance this week, with Western markets like the S&P 500, FTSE, and CAC slipping amid cautious sentiment, while Asian indices—led by Kospi’s strong 4.4% surge and Nikkei’s 1.5% gain—outperformed, reflecting regional optimism and selective risk-on appetite.

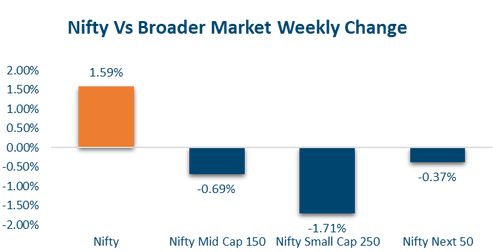

Domestic Equities

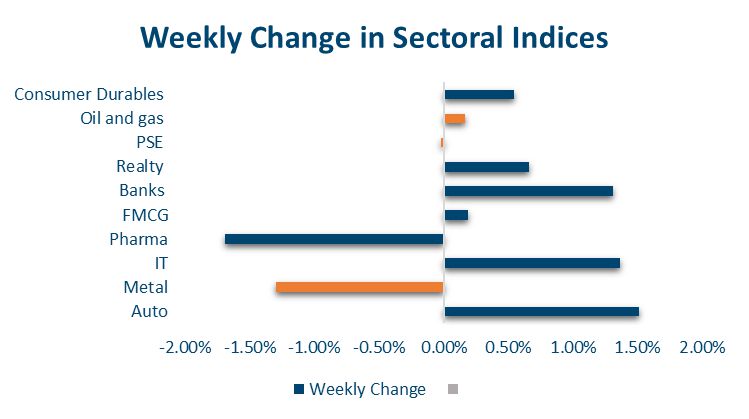

Large-cap indices like Nifty50 led gains this week, rising 1.6%, while mid and small caps declined, reflecting a flight to safety amid valuation concerns— especially as their PE multiples remain elevated. Sectorally, infrastructure, IT, and auto outperformed, while metals and pharma saw sharp declines, indicating selective investor interest in economically sensitive and defensive segments.

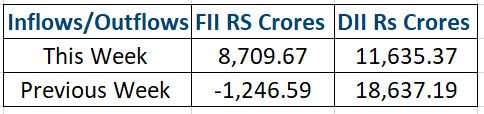

FPIs have sold net USD 0.5bn of domestic Equities in June so far

In terms of factors, markets cap and low volatility outperformed while value, liquidity and dividend underperformed

FIXED INCOME

US 10y yield ended the week 7bps lower at 4.38%. 2y yield was 6bps lower on the week at 3.91%

Yield on the India 10y benchmark ended 1bps higher at 6.31%

1y and 5y OIS are at 5.52% and 5.76% respectively. Overnight call rate has been fixing around 5.30%. TREPS has in fact been trading below the SDF rate, around 5.18% due to abundant liquidity surplus in banking system. Banks are parking more than Rs 3 lakh crs with the RBI in the overnight SDF window at 5.25%!

10y AAA PSU Bond spreads over Gsec is around 55bps and that of NBFCs is around 100bps

FPIs have sold net USD 3.1bn of domestic debt in June so far

PRIVATE EQUITY & VENTURE CAPITAL

Private equity and venture capital activity in India saw a notable slowdown this week, with only 16 deals reported—the lowest since January— compared to 24 transactions in the previous week. The total deal value stood at $495 million, primarily driven by a large real estate transaction.

The major contributor to this week’s deal value was global private equity firm Blackstone’s acquisition of Kolkata’s South City Mall, which accounted for more than three-fourths of the total. Another key transaction was the Series B funding round for Aspora, a remittance services provider, co-led by Sequoia Capital and Greylock Partners. With this, Aspora has raised approximately $93 million across three rounds in the last 10 months.

Separately, the M&A space recorded at least four transactions during the week. The highlight was fintech unicorn Razorpay’s acquisition of a majority stake in POP, a consumer payments platform backed by India Quotient and Unilever Ventures.

INITIAL PUBLIC OFFERING (IPO)

India’s IPO market is witnessing a strong revival, with several companies successfully listing and many more preparing to tap the primary market. Last week saw eight listings, including Sacheerome and Monolithisch India, which delivered impressive gains of over 50%. The buoyant sentiment was supported by healthy investor participation and positive secondary market cues.

Looking ahead, the upcoming week is expected to be one of the busiest in recent months, with 12 IPOs lined up to raise nearly ₹15,800–16,000 crore. The highlight will be HDB Financial Services’ ₹12,500 crore IPO, set to open on June 25, alongside offers from Kalpataru Projects, Ellenbarrie Industrial Gases, and Globe Civil Projects.

The overall pipeline reflects rising confidence among promoters and investors alike. With broad sectoral participation and sustained domestic inflows, India’s primary market seems well-positioned for continued activity in the months ahead, making it a significant contributor to capital formation in FY26.

REAL ESTATE

India’s real estate sector saw two major developments led by Blackstone this week. Its Knowledge Realty Trust raised ₹1,400 crore in a significant pre-IPO round, highlighting strong institutional appetite for commercial real estate.

Additionally, Blackstone acquired Kolkata’s South City Mall for ₹3,250 crore, marking one of the largest retail property deals in India. These moves reflect growing global investor interest in India’s high-quality real estate assets.

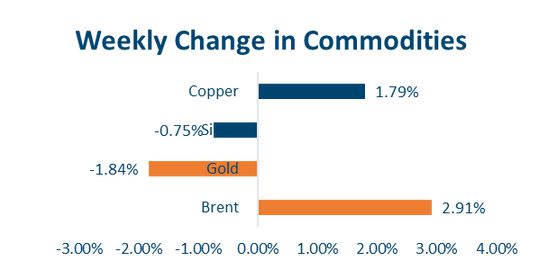

COMMODITIES

Brent rose 3.8% this week to USD 77 per barrel. European natural gas prices spiked 8% to EUR 41 per megawatt hour on account of the Iran Israel conflict.

LME aluminum was up 1.9% this week at USD 2549 per MT.

LME copper was down 0.1% at USD 9633 per MT. Precious Metals too saw some correction with Gold ending 1.9% lower this week at USD 3368 per ounce and silver ending 0.8% lower at USD 36 per troy ounce.

Option Strategies

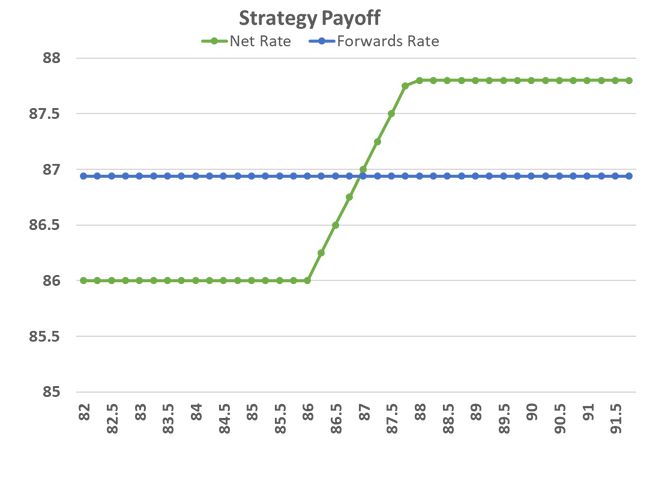

FOR EXPORTERS

Spot ref 86.59, Fwd 86.94, Tenor 3m

BP 86, SC 87.80, 50p premium each leg, Net Zero cost

Note: Exporters with partial open exposures and a stop loss around 86 can explore such option structures

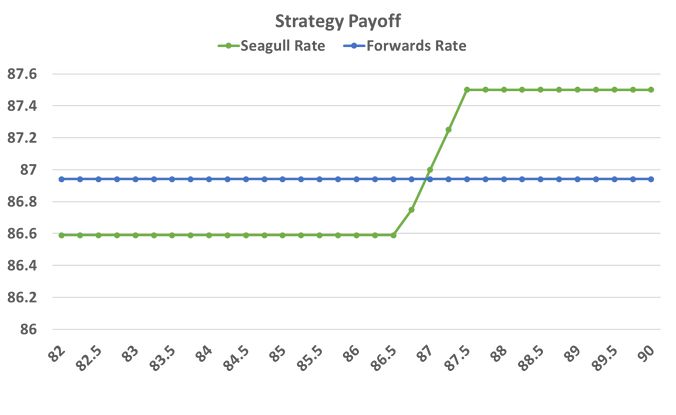

FOR IMPORTERS

Spot ref 86.59, Fwd 86.94, Tenor 3m, BC 87.50

SP 86.59, 66p each leg, Net Zero cost

Our Views: What we Like?

Equities

We expect domestic Equities to continue to remain resilient, especially the benchmark Nifty50, as long as it holds above the 24500 mark on a weekly closing basis

We prefer large caps over mid and small caps, and value and quality over growth and momentum

Bonds & Rates

Surplus liquidity in the banking system is likely to hold down money market rates

10y will be sensitive to Brent. A spike above USD 80 per barrel might result in further steepening of the yield curve

Commodities

We are slightly bullish on base Metals.

Our base case is for Brent to top around the USD 82 per barrel mark.

We are neutral on precious metals

FX

We might witness an immediate knee-jerk reaction of dollar strength on account of safe-haven demand and risk-off sentiment.