Billionz Global Newsletter

Global Developments & Global Equities

LOOMING PUNITIVE TARIFFS CLOUD RATING UPGRADE AND GST REFORMS

Fed Chair Powell’s speech at the Jackson Hole symposium was quite dovish. There was a shift in focus to weakness in the labor market from persistently sticky inflation. U.S. equities and Bonds rallied post his speech, and the Dollar weakened. The market is pricing in 2 cuts by the Fed till the end of December. The September rate cut seems a done deal.

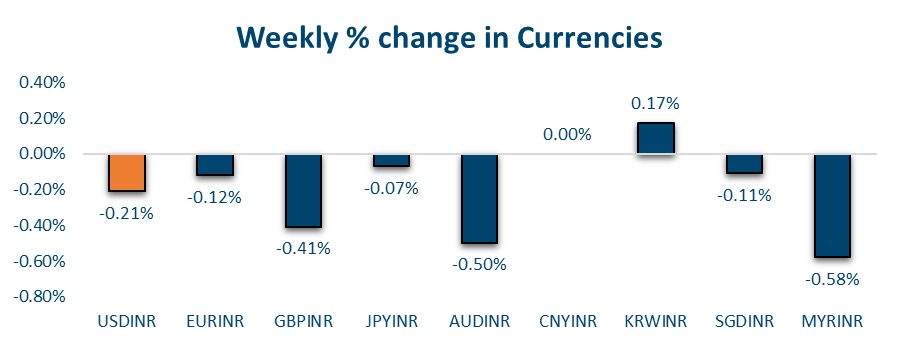

On the domestic front, tariff clouds are not allowing the positive developments in the form of a sovereign rating upgrade and GST reforms to shine through. The possibility that the RBI may use the Rupee as a lever to maintain export competitiveness is weighing on the Rupee, causing it to underperform amid broad Dollar weakness.

Punitive 50% tariffs are to come into effect from 27th August. Latest comments from trade advisor to Trump, Navarro suggests that the penal rate is likely to come into effect as earlier announced, dashing hopes of the 25% penalty being lifted post Trump-Putin meet

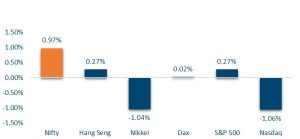

NIFTY V/S GLOBAL MARKETS

Global equity markets saw mixed performance this week. The S&P 500 gained 0.3%, while FTSE outperformed with a 2% rise. European indices like CAC inched up 0.6%, and DAX remained flat. In Asia, sentiment was weaker as Nikkei fell 1.6%, Kospi dropped 1.8%, and Jakarta slipped 0.9%, though Hang Seng and Straits posted modest gains of 0.3% and 0.5%, respectively.

Domestic Equities

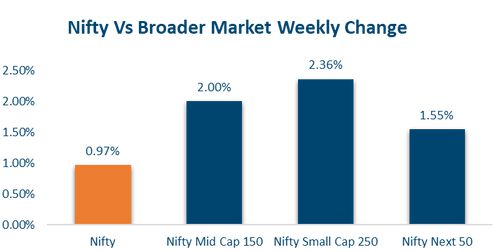

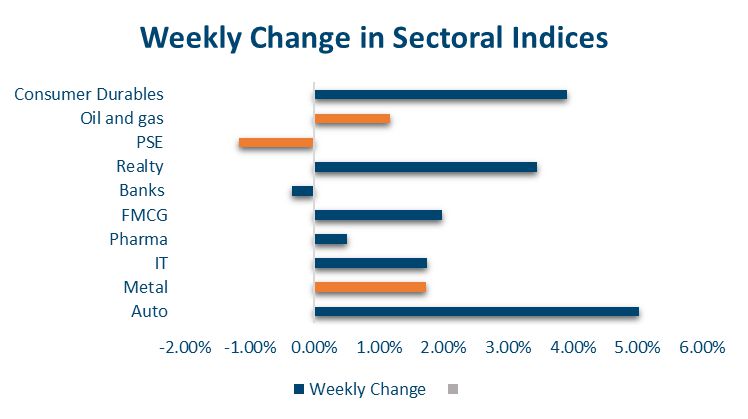

Domestic equity markets witnessed broadbased gains this week, with Nifty50 rising 1%, while Midcap100 and Smallcap250 outperformed, gaining 2% and 2.4%, respectively. Sectorally, Auto led the rally with a sharp 5% rise, followed by Realty (3.4%), Consumer Durables (2.7%), and FMCG (2%), while Bank Nifty slipped 0.4%. On the valuation front, Nifty50 trades at 22.1x trailing and 21.1x forward 12-month earnings, whereas Midcap100 and Smallcap250 remain relatively expensive at 31.4x/27.4x and 29.1x/26.5x, respectively.

In terms of factors, Value underperformed while Growth outperformed this week.

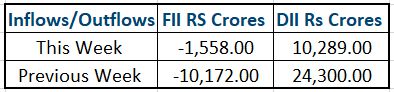

FPIs have sold net USD 2.5bn of domestic equities in August so far.

Fixed Income, IPO and Institutional Deals

INITIAL PUBLIC OFFERING (IPO):

The IPO market is gearing up for another busy week, with about 10 companies set to raise nearly ₹1,200 crore. Notably, Vikran Engineering and Anlon Healthcare together aim to mobilize around ₹893 crore, with their issues opening on August 26 and closing on August 29. This reflects sustained momentum in the primary market despite broader market volatility.

Vikran Engineering’s ₹772 crore issue, priced at ₹92–₹97 per share, includes a fresh issue of ₹721 crore and an offer-for-sale of ₹51 crore. Proceeds will primarily support working capital and corporate needs, making it one of the most closely watched offerings of the week.

In the SME space, Globtier Infotech is launching a ₹31 crore IPO at a fixed price of ₹72 per share from August 25. With several mainboards and SME IPOs lined up alongside multiple listings, the primary market is expected to remain vibrant in the coming days.

PRIVATE EQUITY & VENTURE CAPITAL:

Private equity and venture capital deal value surged last week on the back of a few large transactions, even as fundraising activity slowed. Sixteen companies raised $735 million in the five days ending August 22, nearly double the $371 million raised by 28 firms a week earlier. The top two PE/VC deals contributed about 78% of the total value.

The biggest was Macquarie Asset Management’s $405 million raise for its fleet electrification platform Vertelo, highlighting growing investor interest in India’s EV sector. Capital came from global players such as South Korea’s Green Climate Fund, Australian Ethical Investment, Allianz Global Investors, and Macquarie’s own green transition fund.

M&A volumes dipped to five deals from nine the previous week, but overall value was lifted by Wipro’s acquisition of Harman’s digital solutions business in India, showing how a single large buyout can shape weekly deal trends.

REAL ESTATE:

Mindspace Business Parks REIT has raised ₹550 crore via sustainability-linked bonds from IFC, becoming the first Indian REIT to issue such bonds under SEBI’s ESG framework. With a previous ₹650 crore raise in June 2024, total issuance now stands at ₹1,200 crore, reflecting its push to integrate ESG goals, boost energy efficiency, and expand greencertified spaces.

Proposed GST reforms, cutting rates to 5% and 18% and reducing cement tax from 28% to 18%, could ease housing costs by 2–4% if input tax credits are restored. However, the relief may be limited, given construction costs have surged ~40% since 2019, luxury housing prices exceed ₹5,000 per sq ft in metros, and developers typically pass on 5–6% of rising input costs to buyers.

FIXED INCOME:

US 10y yield fell 8bps this week. Powell’s dovish comments at the Jackson Hole symposium fuelled the rally. 10y yields across the Eurozone and UK were down 2-5bps this week.

Yield on the benchmark 10y rose 15bps this week to 6.55%. The impact of the rating upgrade has been completely wiped out. The belief that we are already at the terminal rate in this cut cycle and concerns over the fiscal impact of GST slab revision are causing nervousness in Bond markets.

10y AAA PSU and NBFC spreads are at 42bps and 71bps, respectively.

1y OIS was almost unchanged at 5.52% while 5y OIS rose 8bps to 5.74%. Overnight MIBOR fixings have been happening in a 5.48-5.57% range

FPIs have invested net USD 1.8bn in domestic debt in August so far.

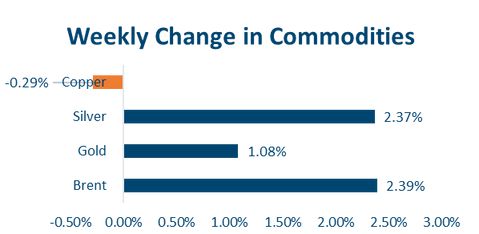

COMMODITIES:

Commodities saw mixed performance this week. Brent crude surged 2.9% to USD 67.7, while US natural gas plunged 7.5% to USD 2.7. Among metals, aluminum gained 0.7% at USD 2,624 and copper edged up 0.2% to USD 9,796. Precious metals were stronger, with gold rising 1.1% to USD 3,372 and silver advancing 2.3% to USD 38.9.

Our Views: What we Like?

Equities:

24650 is an extremely crucial gap support level for Nifty50. Till the time that holds, we remain biased to the upside.

We prefer large caps and select midcaps from a long-term portfolio construction point of view, and want to avoid the Small-cap and Microcap space for now

Bonds & Rates:

We believe current levels are attractive to add duration in U.S. Treasuries.

6.60-6.70% levels on the 10y would be good levels to further add duration to the portfolio.

We have been suggesting paying 5y OIS from below 5.7% levels. 5y OIS looks good to pay even at

current levels

Commodities:

We believe Brent has a floor in place at USD 60 per barrel. We do not see it go up in a hurry either.

We remain bullish on precious metals, more on Silver than on Gold.

FX:

We continue to expect the Dollar to trade weakening bias overall, especially against alternative Reserve Currencies such as JPY, EUR, and CHF.