Billionz Global Newsletter

Global Developments & Global Equities

S&P500 SOARS TO RECORD HIGHS, NEGATIVE EARNINGS SURPRISES WEIGH ON DOMESTIC EQUITIES

Negative Earnings surprises and elusive trade deal with the US, with 1st August deadline approaching are keeping markets nervous. This resulted in domestic Equities and Rupee underperforming this week.

Among Asian countries, Vietnam, Indonesia and Philippines have already secured deals with US. Trump said that there is a 50-50 chance of a US EU trade deal and that it may not reach a trade deal with Canada. As the 1st August deadline approaches, we can expect more drama on this front.

Other key events to look forward to in the coming week will be the Fed rate decision on Wednesday and BoJ rate decision on Thursday

On the data front, US July Jobs report is due on Friday

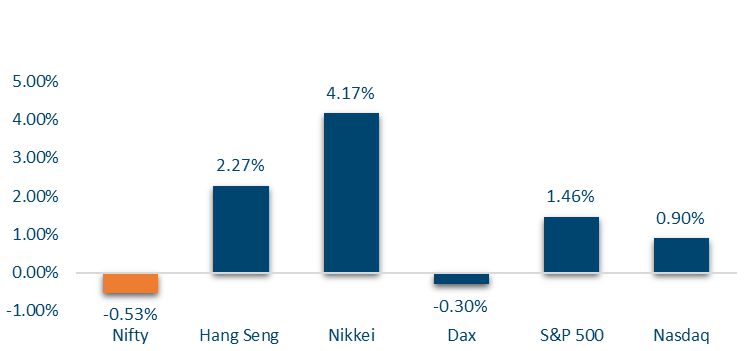

NIFTY V/S GLOBAL MARKETS

Global equity markets saw mixed performance this week. The Nikkei led gains with a sharp rise of 3.9%, followed by Jakarta (3.2%) and Hang Seng (2.3%). The S&P 500 and FTSE also posted solid gains of 1.5% and 1.4%, respectively. Meanwhile, Germany’s DAX dipped 0.3%, reflecting some weakness in European equities.

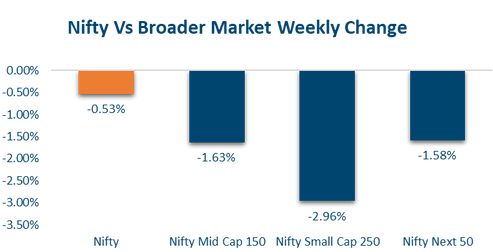

Domestic Equities

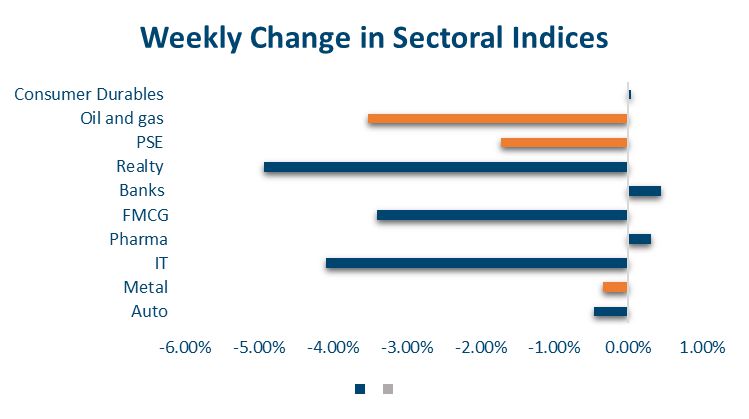

This week, Indian benchmark indices saw a decline, with Nifty50 down 0.5%, Midcap100 falling 1.9%, and Smallcap250 slipping 3%. Valuation-wise, Nifty50 trades at a trailing/forward PE of 22.8/21.1, while Midcap100 and Smallcap250 remain expensive at 33.2/29.0 and 31.0/27.5, respectively. Among sectoral indices, Bank Nifty (+0.4%) and Pharma (+0.3%) were the only gainers. Realty (-4.9%), IT (-4.1%), and FMCG (-3.4%) led the losses. Broader markets underperformed large caps across the board.

For the 22 Nifty50 companies that have reported Earnings so far, sales surprise is 7.2% and Earnings surprise is 5.4%

In terms of factors, Growth and Momentum outperformed this week while Dividend Yield and Quality underperformed

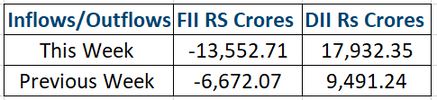

FPIs have pulled out net USD 750mn from domestic Equities in July so far

FIXED INCOME

Yield on the US 2y ended 6bps higher at 3.92% Yield on the US 10y ended 1bps higher on the week at 4.39%.

10y Yields across Eurozone countries were up 11 13bps this week on a hawkish ECB

Yield on the 10y JGBs also rose 9bps to 0.84%

Yield on the India 10y ended 4bps higher at 6.35% this week.

1y OIS ended 3bps higher at 5.53% and 5y OIS also ended 3bps higher at 5.73%. Overnight call fixing had spiked to 5.82% on Wednesday. On Friday, it cooled off to 5.44%

10y PSU AAA spreads are about 50bps and 10y AAA NBFC spreads are about 90bps

FPIs have invested net USD 950mn in domestic Equities in July so far.

PRIVATE EQUITY & VENTURE CAPITAL

Private equity and venture capital deal activity declined last week, with total investments falling 54% to $215 million due to the absence of large ticket deals. The number of transactions dropped slightly to 24, with the top two deals accounting for half the week’s funding.

Key investments included GupShup’s capital raise from Globespan Capital and EvolutionX, along with mid-sized deals in Kumar Vibe Properties, Netrasemi, and Superk, which raised around $37 million collectively.

M&A activity rose marginally in volume but surged in value to over $1.2 billion, led by Tilaknagar Industries’ $486 million acquisition of Imperial Blue from Pernod Ricard and Titan’s $283 million purchase of Dubai’s Damas. Other major deals included Natco Pharma’s $226 million stake buy in South Africa’s Adcock Ingram and Sun TV’s $135 million acquisition of UK-based cricket team Northern Superchargers.

INITIAL PUBLIC OFFERING (IPO)

The IPO market saw a mixed week with strong listings from Cryogenic OGS (up 196%), Anthem Biosciences, and Ellenbarrie Industrial Gases, while others like Pushpa Jewellers and Vandan Foods listed below the issue price, showing selective investor appetite.

Next week is set to be active with 13 IPOs—including 5 mainboard and 8 SME issues—looking to raise over ₹7,300 crore. The spotlight is on NSDL’s ₹4,011 crore IPO, which opens on July 30 and closes August 1, entirely offer-for-sale, priced between ₹760–₹800 per share.

NSDL’s IPO is generating significant interest due to its attractive pricing, reportedly 22% below its last unlisted value. A strong grey market premium suggests potential listing gains of ~20%, which could set a positive tone for the primary market going forward.

REAL ESTATE

Mindspace Business Parks REIT, backed by K Raheja Corp, has completed its first third-party asset acquisition by purchasing Q-City, a premium commercial office asset located in Hyderabad’s Financial District, for ₹511.8 crore. The acquisition was executed through Horizonview Properties Pvt. Ltd., a special purpose vehicle of the REIT. The asset, previously owned by Mack Soft Tech, will now be rebranded as “The Square, 110 Financial District.”

In a separate development, Kumar Vibe Properties—a joint venture between Kumar Properties & Infrastructure and Vibe Realty—has secured ₹115 crore in funding from Nisus Finance. The capital will support three residential and commercial projects across Mumbai and Pune. Gopal Sarda, CEO of Vibe Realty, noted that this financial infusion not only ensures funding stability but also strengthens the firm’s positioning in key real estate markets.

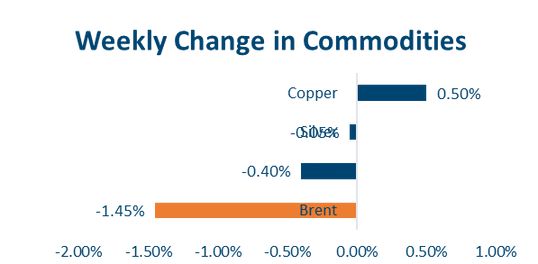

COMMODITIES

Commodity markets were mixed this week. Brent crude declined by 1.2% to $68.4, while US natural gas saw a sharp drop of 12.8% to $3.11. Industrial metals remained largely flat, with aluminum up 0.2% and copper down 0.1%. Precious metals also stayed range-bound—gold dipped 0.4% and silver remained unchanged.

Option Strategies

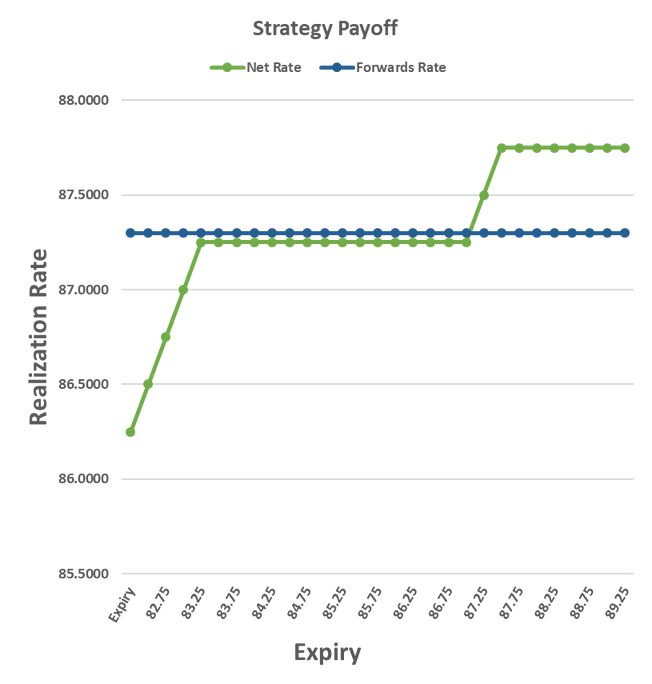

EXPORTER OPTION STRATEGY (KIKO)

Spot Ref – 86.50, ATMF – 87.30, BP – 87.25, SC – 87.75, SP- 83.50

Tenor 6 Months

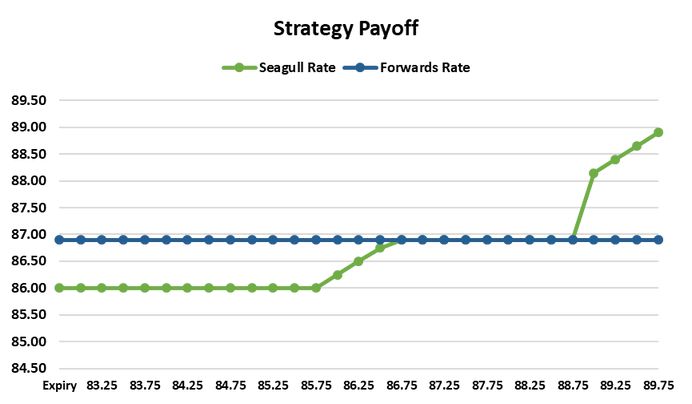

IMPORTER OPTION STRATEGY (SEAGULL)

Spot Ref – 86.50, BC – ATMF – 86.90, SC – 88.00, SP- 86.00, Cost less than 0 paisa, Tenor 3 months

Our Views: What we Like?

Equities

Nifty50 price action over the last couple of sessions has got us to turn a bit cautious over the medium term from neutral.

24470 will be an extremely crucial support for the Nifty5.0, and we may see that get tested

Negative Earnings surprises in the Midcap space may make current lofty valuations unsustainable.

From a long-term investment perspective, we are more comfortable sticking to Nifty50 and that too defensives, rather than venturing out in the Midcap and Smallcap space.

Bonds & Rates

Yield on the benchmark 10y may test 6.45-6.50% from current levels.

We believe the 5-year OIS is bottoming out and offers a good opportunity to those looking to pay

Commodities

We are neutral on Crude and Base Metals over the medium term, given tariff-related uncertainty.

We believe Precious metals, though, are a buy on dips as we see Dollar weakness against majors.

FX

We expect the dollar to remain weak against alternative Reserve currencies.