Billionz Global Weekly Newsletter

Global Developments & Global Equities

DOMESTIC ASSETS RESILIENT DESPITE ESCALATION IN BORDER TENSIONS; MIGHT RALLY ON FIRST SIGNS OF LASTING CALMNESS

In a latest development on trade, US President Trump said great progress has been made on trade talks between US and China. A total reset has been negotiated in a friendly and constructive manner, he added.

Trump administration decided not to go ahead with AI chip restrictions imposed by Biden administration that were due to come into effect from 15th May

The US Fed left Rates unchanged and highlighted increasing possibility of a stagflationary situation

US April CPI will be the key data to look forward to in the coming week. Market is pricing in 2.6 cutd by the Fed until end of 2025 compared to 3.2 cuts last week

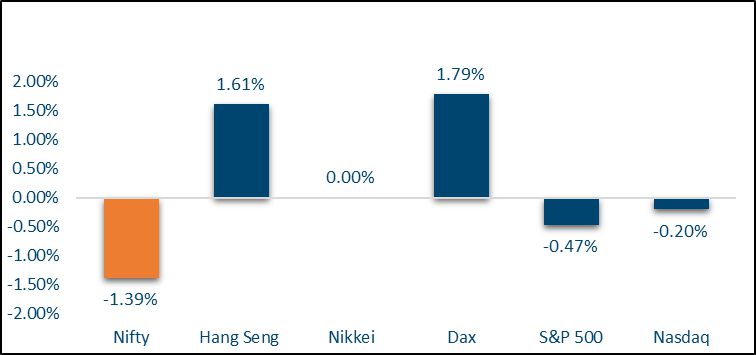

NIFTY V/S GLOBAL MARKETS

US equities took a bit of a breather this week while European and APAC equities did well.

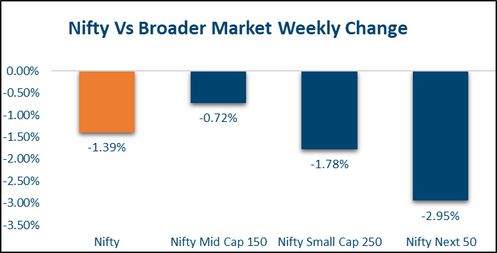

Domestic Equities

Out of the 32 Nifty50 companies that have reported Q4FY25 Earnings so far, Average Revenue surprise has been 1.6% and Average Earnings surprise has been 3.8%. Over the previous 7 quarters Revenue surprise has been on an average 13%

Below is how the valuations stand in terms of PE considering trailing and forward 12m EPS:

Nifty50: 22.5, 20.2, Midcap100: 36.7, 29.3, Smallcap250: 26.4, 25.2

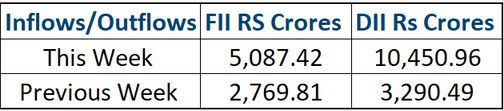

FPIs have so far invested net USD 1.7bn in domestic equities in first few sessions of May so far, continuing the momentum from last week of April

In terms of style, size and liquidity outperformed while value and Dividend yield underperformed this week

FIXED INCOME:

Yield on the US 2y edged up 6bps to 3.89% and that on the 10y rose 3bps to 4.38%

10y Yields across Eurozone and UK were up 3 5bps.

Yield on the old 10y benchmark traded a 6.31 6.44% range this week and eventually ended at 6.38, 4bps higher than last week’s close.

1y OIS was almost unchanged at 5.64% for the week while 5y OIS rose 6bps to 5.66%

10y AAA PSU spreads are at 50bps and 10y AAA NBFC spreads are at 78bps

RBI announced relaxations in limits for FPIs to invest in corporate bonds this week.

PRIVATE EQUITY AND VENTURE CAPITAL

Private equity and venture capital investments in India nearly doubled to $690 million across 32 deals in the week ending Friday, up from $396 million across 30 deals the previous week. The actual figure is likely higher due to undisclosed deal values.

The week’s largest deal saw PB Health raise $218 million in a seed round, with $50 million contributed by Silicon Valley-based General Catalyst. Meanwhile, Singapore’s sovereign wealth fund GIC invested approximately $120 million in Dr Agarwal’s Health Care Ltd, raising its stake to around 7.5%.

The M&A space was highlighted by a major deal in which a 20% stake in YES Bank is set to be acquired by Japanese lender Sumitomo Mitsui Banking Corporation (SMBC). The transaction, valued at over $1.5 billion, involves the purchase of a 13.19% stake from SBI and an additional 6.81% from other banks.

INITIAL PUBLIC OFFERING (IPO)

India’s IPO market remained muted, influenced by global economic uncertainties and rising geopolitical tensions with Pakistan. Notably, Avanse Financial Services and Anthem Biosciences postponed their IPOs, reflecting cautious investor sentiment. Ather Energy proceeded with its Rs. 2,981 crs. IPO but faced a lukewarm response, with shares declining over 4% on debut, underscoring challenges in the electric vehicle sector.

Coming week, several IPOs are opening for subscription. In the SME segment, Integrity Infrabuild Developers Ltd and Accretion Pharmaceuticals Ltd will open their IPO. Virtual Galaxy Infotech Ltd IPO is active, with a price band of ₹135–₹142 per share, open from May 9 to May 14

REAL ESTATE

Property Share Investment Trust, co-founded by ex-Blackstone executive Kunal Moktan and Hashim Khan, has filed draft papers with SEBI to list its second Small and Medium REIT (SM REIT) scheme. The new scheme, PropShare Titania, aims to raise around ₹472 crore via IPO, following its first scheme, PropShare Platina, which targeted ₹350 crore. The platform received its SM REIT licence in August 2023.

Bengaluru-based Simpliwork Offices, backed by the Sattva Group, plans to double its managed office space from 4.2–4.5 million sq. ft. to 9–9.5 million sq. ft. over the next two years. The board approved expansion focuses on high-demand, established markets with continued strong demand across existing micro-markets.

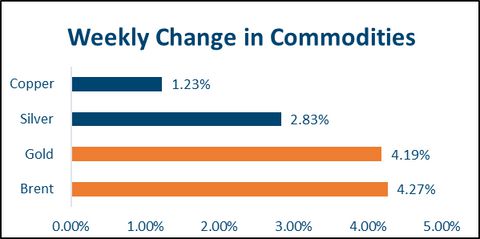

COMMODITIES

Brent saw a technical bounce back this week and ended 4.3% higher at USD 63.9 per barrel

Precious metals gained with Gold ending 2.6% higher at USD 3324 and Silver 2.2% higher at USD 32.7 per troy ounce. Gold hit an all time high of USD 3435 intraweek

3M LME Aluminum ended flat this week at USD 2417 and Copper advanced 2.6% to USD 9445. Dalian Iron ore ended 0.6% lower.

Our Views: What we Like?

Equities

We continue to believe that the trend in Nifty50 is higher, as long as 23500 holds. We prefer value and quality over growth and momentum. Large cap names in Pharma and FMCG could outperform given that Earnings have also been supportive.

Fixed Income

We see the terminal repo rate as 5.50% in the current rate cut cycle. This is reasonably well priced in, in both Bonds as well as Rates. We therefore see limited room for downside in 10y Gsec Yield from current levels. 10y US treasuries are however looking attractive at current levels of around 4.40%

Commodities

We expect Gold to take a breather after the tremendous rally. Silver may have further upside left. While we may not see an immediate move higher in Brent, we could have seen a bottom in Brent at sub 60 levels. We continue to remain neutral on Base metals

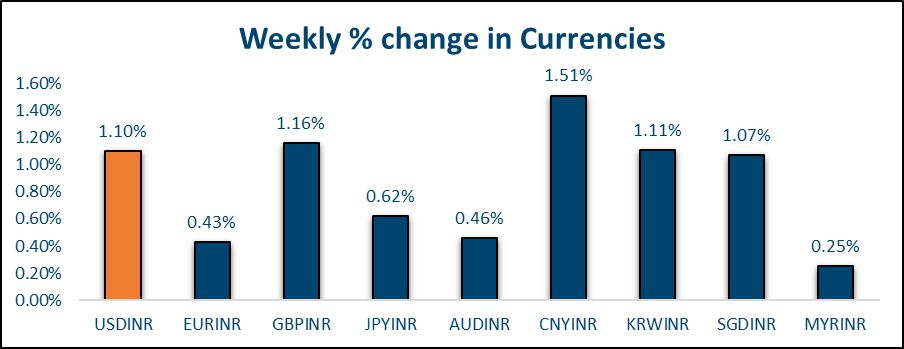

FX

We continue to believe that the US Dollar will get sold off on upticks We do not see runaway depreciation in Rupee on account of idiosyncratic factors as RBI has enough ammunition to intervene.