Billionz Global Weekly Newsletter

Global Developments & Global Equities

RISK SENTIMENT RECOVERED AFTER US ANNOUNCED 90-DAY PAUSE FOR ITS

TRADE PARTNERS TO NEGOTIATE

The markets heaved a sigh of relief on Wednesday as Trump announced a 90 day pause on tariffs for all countries, except China. The reason for the 90-day pause could have been the turmoil in bond and stock markets. China however increased its tariffs on U.S. imports to 125% on Friday, hitting back against President Donald Trump’s decision to raise duties on Chinese goods to 145% and increasing the stakes in a trade war that threatens to upend global supply chains

US March CPI came in lower at 2.4% against the expected 2.6% YoY. Core CPI too was lower at 2.8% against the expected 3% YoY. However, Fed members have expressed concerns around the inflationary impact of tariffs.

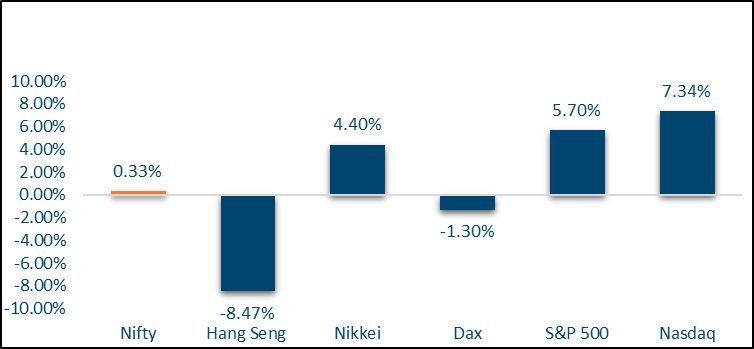

NIFTY V/S GLOBAL MARKETS

Global equities partially recovered from the bloodbath of last week amid risk on sentiment led by a pause of 90 days window for tariffs.

Domestic Equities

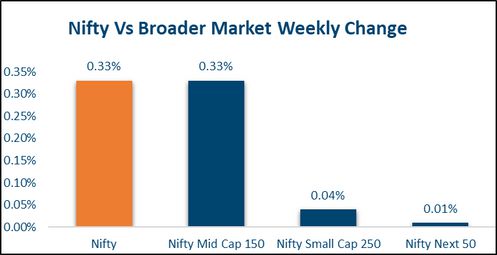

Nifty50 closed almost flat at 22800 levels. Broader indices were also in line with Midcap100 at -0.3% & Smallcap 250 ending flat.

Gift Nifty futures is indicating +0.4% for the Nifty on Monday open

Below are the valuations in terms of P/E across large, mid and smallcaps based on trailing 12m and forward 12m Earnings (10Y Historical PE)

Nifty50: 21.2, 19.2 (25.1), Midcap100: 33.7, 27.8 (40.1), Smallcap250: 24.5, 24.5 (35.1)

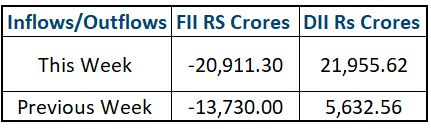

FPIs have sold USD 3.8bn of domestic Equities in the month of April

Fixed Income, IPO, and Institutional Deals

REAL ESTATE:

Family offices are moving away from direct property ownership toward alternative real estate investments, driven by generational shifts, liquidity needs, and evolving market conditions. While real estate remains a key asset, its dominance is declining as younger leaders prefer more flexible, low-maintenance options. Direct ownership—still common among legacy families —is being trimmed to around 3–4% by younger investors wary of resale challenges, taxes, and depreciation. Indirect avenues like REITs and real estate funds are gaining interest, with confidence slowly returning thanks to stronger sector performance. Segments like hotels, hospitals, and warehouses are increasingly attractive for their rental yields.

PRIVATE EQUITY AND VENTURE CAPITAL:

Funding momentum was seen to improve slightly in the second week of April, aided by a series of mid- and late-stage deals that were executed by investors such as WestBridge Capital, ICICI Venture, and Bessemer Venture Partners. PE and VC deal value was recorded at around $310 million across 29 deals, compared to $281 million across 31 deals in the previous week.

The largest transaction involved $60 million being raised by Bengaluru-based fintech Juspay in a Series D round that was led by Kedaara Capital, with participation from existing investors SoftBank and Accel. A partial stake in Juspay was also sold by Stockholm-listed fintech investor VEF AB for $14.8 million through a secondary sale.

M&A activity remained muted but included notable developments, such as the distressed sale of MissMalini Entertainment, owned by Good Glamm Group, which was acquired by Indore-based content and marketing agency Creativefuel.

INITIAL PUBLIC OFFERING (IPO):

In the upcoming week, no new IPOs are scheduled for listing on Indian exchanges, reflecting a temporary pause in market activity. This lull is attributed to global uncertainties, including tariff-related disruptions, which have led to a cautious approach among investors and a slowdown in IPO preparations.

Despite the current standstill, the IPO pipeline remains robust. The Securities and Exchange Board of India (SEBI) has recently approved IPO proposals from four companies: BlueStone Jewellery and Lifestyle, GK Energy, Aye Finance, and Anthem Biosciences. These approvals indicate a potential resurgence in IPO activity once market conditions stabilize.

FIXED INCOME:

U.S. Treasury yields rose as risk sentiment improved after a 90-day pause announcement. The 10-year yield jumped 31bps to 4.49%, and the 2-year rose 20bps to 3.96%. Anticipated tax cuts may add further pressure on long-term yields. Strong 10- and 30-year auctions provided some market stability, though liquidity concerns keep investors cautious. Eurozone and UK 10-year yields edged up 1–6bps. In India, the 10-year yield dipped 2bps to 6.44% after the RBI cut its repo rate for the second time and shifted its stance to accommodative, opening the door to more rate cuts. RBI also trimmed FY26 growth forecast to 6.5% (from 6.7%) and inflation to 4% (from 4.2%). The 1-year OIS fell 15bps to 5.77%, and the 5-year slipped 2bps to 5.71%.

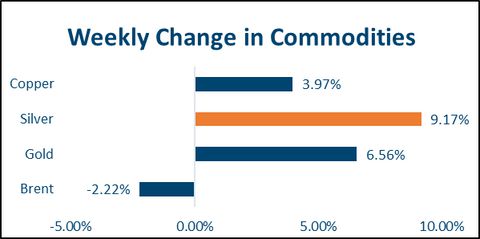

COMMODITIES:

Brent was down another 10% during the week as the intensifying trade war between the US and China triggered worries over demand for Oil. Later it recovered to close with marginal loss of 1.2%.

Gold was up 2% at $3,236.67, after hitting a record high of $3,243.82 earlier in the session. Gold is up over 6% this week while Silver is up 9% for the week.

Our Views: What we Like?

Equities:

On the domestic front, Nifty50 seems to be finding strong support in the 21700-21800 zone. Unless we see further turmoil in global markets, we expect those levels to hold. We remain cautious in the near term given the tariff related uncertainty. We will look to add large caps on dips and stick to the value style for now. We are looking to add US equities to our model portfolio on first signs of the sell off abating. We will monitor the progress on US-China trade relations closely and look to add China exposure on first signs of amelioration.

Fixed Income:

We continue to remain bullish on US Rates and treasuries. 5y OIS at 5.73% looks attractive to pay to lock in a fixed rate. 10y benchmark bond yield could move lower to 6.35-6.40%. We remain bearish on credit spreads and expect them to widen.

Commodities:

We believe gold will continue to see safe haven demand while base metals and crude could continue to remain under pressure in the near term. After a spectacular week for bullion, there can be a 4-5% correction, however, the medium-term trend is on the upside. Brent has tested the support of USD 58-60 levels in the last week. Another 8-10% price correction can be witnessed on an escalation of trade war & demand constraints, however, we expect a bounce in Brent prices on the back of risk on sentiment.

FX:

We expect the Dollar to weaken against major currencies. Concerns over growth will likely dominate concerns over inflation. This might cause the market to expect faster rate cuts by the Fed.