Billionz Global Weekly Newsletter

Global Developments & Global Equities

RISK ASSETS RALLY AS TRADE UNCERTAINTY DIMINISHES

Risk sentiment improved this week as trade tensions eased. US and China agreeing to reduce tariffs for a 90 day window over last weekend and approach trade talks constructively comforted markets.

Prospects of a US-Iran nuclear deal also bolstered sentiment.

US data this week including CPI, PPI, Retail sales ex auto and industrial production was all weakened than expected. This, coupled with lowering of inflation expectations (due to trade tensions easing) means the Fed can turn a bit dovish now. However, the rates market is still just pricing in 2 cuts till the end of 2025.

Rating agency Moody’s cut US credit rating by one notch to Aa1 from Aaa. It changed the outlook to stable from negative. Though the announcement just came before US bond markers shut and US 10y rose 5bps in an immediate reaction, we will have to see of there is any follow through on Monday.

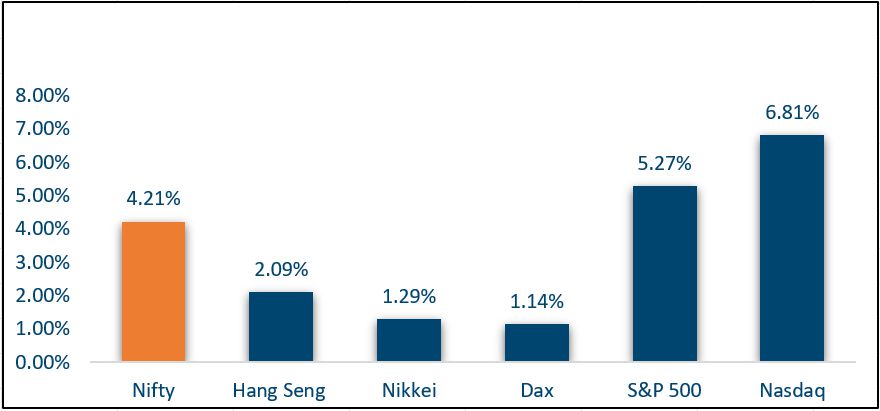

NIFTY V/S GLOBAL MARKETS

Equities globally had a good week. Easing of global trade tensions has eliminated a lot of uncertainty over the short term.

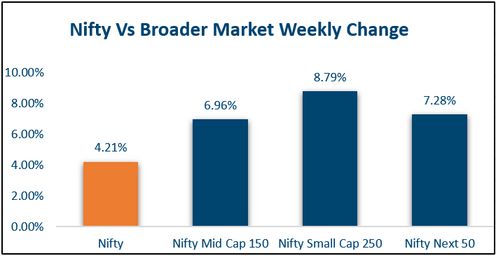

Domestic Equities

Moreover easing inflation in the US, coupled with lowering of inflation expectations gives Fed headroom to cut Rates. This too is being taken positively by equity markets.

S&P500 ended the week 5.3% higher and is now back in positive territory on a YTD basis. It is up 23% from 7th April lows and is just about 3% shy of all time highs.

Below is how the valuations stand in terms of PE considering trailing and forward 12m EPS:

Nifty50: 23, 21, Midcap100: 38, 30, Smallcap250: 28, 27.5

In terms of factors, Liquidity and value outperformed while low volatility and market cap underperformed this week.

FIXED INCOME

US Yields had spiked earlier on in the week but retraced on weak US CPI PPI, Retail sales and Industrial production data. 2y ended at 4% and 10y at 4.48%. While UK 10y yield was flat, 10y yields across Eurozone were down anywhere between 4-10bps this week

Domestic April CPI print came in at 3.16% yoy on low food inflation. This has in most likelihood sealed the June rate cut of 25bps. 1y and 5y OIS were down 2bps for the week and ended at 5.62% and 5.64% respectively

Yield on the old 10y benchmark fell 10bps to 6.27% aided by soft domestic inflation print and also a move lower in US treasury yields post weak US data.

Banking system liquidity is in surplus of around Rs 2 lakh crs. Overnight call rate has been fixing below the repo rate consistently, around 5.90%.

PRIVATE EQUITY & VENTURE CAPITAL

Private equity and venture capital activity slowed during the five-day period ending Friday, with deal volume down to 28 from 32 and 30 in the previous two weeks. Total investments dropped 40% to $412 million, with only one deal exceeding the $100-million mark—down from three last week.

The sole large-ticket deal involved a $171 million investment in NBFC IKF Finance Ltd. by Norwest Venture Partners and Motilal Oswal Alternates, contributing nearly 40% of the week’s total funding. JSW One Platforms followed, reaching a $1 billion valuation in a round backed by Principal Asset Management, OneUp, and JSW Steel.

M&A activity also remained subdued, with deal count falling to 6 from 10 week-on-week, and several transaction values undisclosed. Notably, ASG Hospital acquired a majority stake in Thane based Dr. Gadgil Eye Hospital, further expanding its eyecare network.

INITIAL PUBLIC OFFERING (IPO)

About four IPOs—two on the Mainboard and two on the SME platform—are scheduled for launch next week, signaling a slight uplift in investor interest. Borana Weaves, a Surat-based synthetic textile firm, will raise ₹145 crore from May 20–22, with funds earmarked for a new unit and working capital. Grey market premiums indicate potential listing gains of around 27%. Belrise Industries, an automotive components company, will open a ₹2,150 crore IPO on May 21 to support expansion and acquisitions.

Separately, More Retail, backed by Amazon and Samara Capital, plans a ₹2,000 crore IPO in 2026 aimed at debt reduction and expanding to 3,000 stores by 2030. The upcoming IPOs showcase a diverse sector mix and are expected to attract strong interest from both institutional and retail investors.

REAL ESTATE

An IPO has been launched by Dubai Holding, one of the UAE’s largest landowners and developers, for its Dubai Residential REIT, with up to $487 million expected to be raised. The listing represents the first REIT IPO in Dubai since Talabat in December, and only the second in the UAE this year, despite a robust pipeline of upcoming offerings. A 12.5% stake is being offered, valuing the REIT at up to $3.9 billion, with AED 1.1 billion in dividends projected for 2025.

In India, a public advisory was issued by SEBI following the voluntary surrender of registration by Strata SM REIT. It was clarified that no funds had been raised nor assets acquired by the REIT prior to its exit. SEBI has advised investors to verify the registration status of REITs before investing, reinforcing the regulator’s commitment to transparency and investor protection in the country’s evolving REIT landscape.

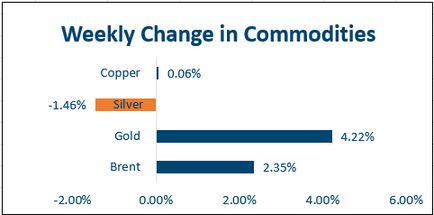

COMMODITIES

Brent ended the week 2.4% higher at USD 65.4 per barrel. News of likelihood of US-Iran nuclear deal (I.e. US relaxing sanctions on Iran in exchange of Iran halting nuclear program) and EIA data indicating inventory build capped gains.

LME Aluminum was up 2.7% for the week and Copper was flat. Iron ore was up 1.7%

Precious metals came off as risk sentiment improved. Gold ended the week 3.7% lower at USD 3203 and Silver ended 1.3% lower at USD 32.3 per troy ounce.

Our Views: What we Like?

Equities

We remain constructive on domestic equities given the price action, performance of broader markets and breadth this week and move move our pivot higher to 24300 from 23500. As long as market holds above 24300, it continues to remain a buy on dips market.

Valuations in large cap space seem relatively attractive (though higher by historical standards) from a long term investment perspective. Valuations in Midcaps and Smallcaps are overstretched.

Bonds & Rates

We see the terminal repo rate as 5.50% in current rate cut cycle.

We see limited room for 10y Yields to drop further from current levels. We may bottom out in the

6.15-6.25% zone.

Commodities

We believe that a medium term bottom is in place in Brent as prices are not moving lower despite positive news flow.

We believe Gold and Silver could see some correction in near term. Long precious metals had become a crowded trade.

With trade tensions easing, we may see base metals trade with a positive bias.

FX

We believe the Dollar will continue to trade with a weaker bias.

However, the Rupee is likely to continue to underperform.