Billionz Global Weekly Newsletter

Global Developments & Global Equities

BIG BEAUTIFUL BILL CLEARING THE HOUSE SENDS JITTERS THROUGH BOND, EQUITY MARKETS

Trump’s tax bill cleared the House of Representatives through the most slender of margins. The bill now advances to the Senate where it needs to get a simple majority I.e. 51 votes. There are currently 53 Republicans in the Senate. The administration has set a deadline of 4th July to pass the bill. If the Senate makes changes, the bill will again go back to the House.

The passage of the bill made the bond markets nervous as it is certain to widen US budget deficits and increase the US debt to GDP. The tepid response to the 20y bond auction sent the yields at the longer end soaring. It also dented sentiment in the equity markets.

Market has further trimmed expectations of a Fed cut. It now expects only 1.8 cuts by end of 2025.

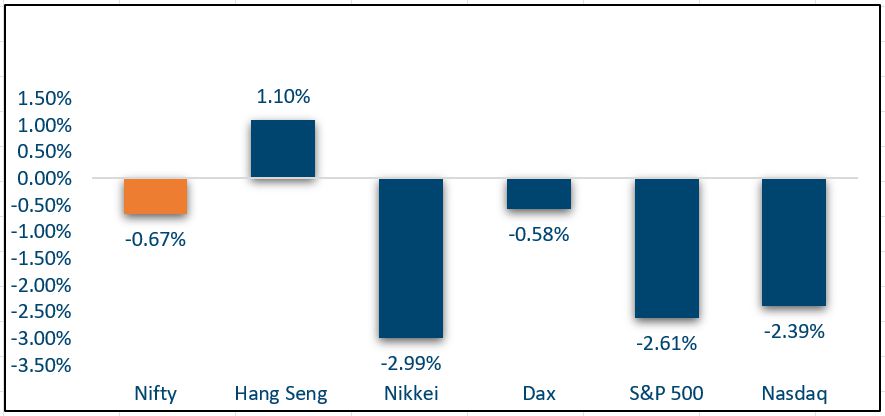

NIFTY V/S GLOBAL MARKETS

Equities globally had a tepid week. Nervousness in bond markets spilled over to equities

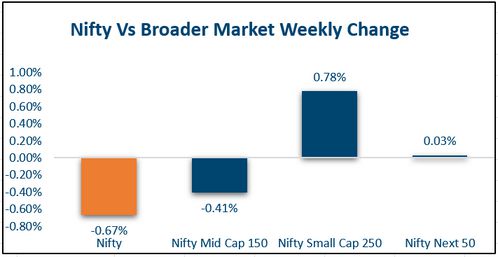

Domestic Equities

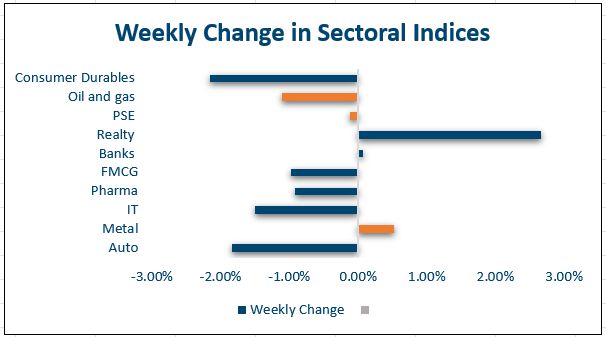

In terms of style, Quality, Liquidity and value outperformed while market cap and low volatility underperformed

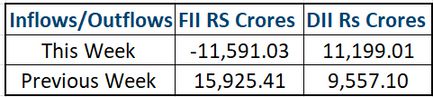

FPIs have invested net USD 1.6bn in domestic equities in May so far.

Below is how the valuations stand in terms of PE considering trailing and forward 12m EPS:

Nifty50: 22.8, 21, Midcap100: 36.6, 30, Smallcap250: 28.3, 27.6

In terms of factors, Liquidity and value outperformed while low volatility and market cap underperformed this week.

FIXED INCOME

The US yield curve bear steepened this week. Yield on the US 2y rose 2bps. Yield on the US 10y rose 6bps to 4.51% and that on 30y rose 13bps

10y yields across Eurozone and UK changed by anywhere between -3 to 2 bps.

30y Japan government bond Yields are at record highs. It had hit 3.18% intraweek but ended at 3.04%. Higher yields on JGBs are also likely to see Japanese investors shunning US treasuries. This is likely to exert further pressure on US Yields to the upside, especially longer end.

Yield on the old 10y benchmark ended 2bps lower at 6.25%

1y OIS fell 8bps to 5.54% while 5y OIS ended almost flat at 5.63% FPIs have pulled out USD 1.5bn from domestic debt in May so far

PRIVATE EQUITY & VENTURE CAPITAL

Private equity and venture capital activity in India slowed for the second consecutive week, with overall deal value dropping nearly 25% to $313 million from $412 million in the prior week. The number of deals also declined to 23, its lowest in two months, due to the absence of large-ticket transactions.

The largest disclosed PE deal involved the Canada Pension Plan Investment Board acquiring a 14% stake in a new packaging platform formed by PAG, combining Manjushree Technopack Ltd and Pravesha Industries Pvt. Ltd.

M&A activity remained muted with only three deals, down from six a week earlier. Waaree Energies’ ₹293 crore acquisition of Kamath Transformers led the segment. Nazara Technologies acquired UK-based Curve Games for ₹247 crore, while Rasna bought the beverage brand Jumpin, previously owned by Hershey’s, for an undisclosed amount.

INITIAL PUBLIC OFFERING (IPO)

several issues drew strong investor participation. The IPO of Belrise Industries saw nearly 5x subscription by closing, accompanied by a grey market premium of ₹23—signaling upbeat sentiment. Meanwhile, Virtual Galaxy Infotech listed with a 26% premium on the NSE SME platform after being oversubscribed over 231 times, highlighting robust appetite among investors.

The coming week is expected to remain active, with the ₹3,500 crore IPOs of both The Leela Hotels and Aegis Vopak Terminals scheduled to open on the same day. Additional public issues from Prostarm Info Systems, Astonea Labs, and Nikita Papers are also slated, suggesting continued momentum in the primary market.

Following a quiet three-month period, this renewed activity—driven by seven offerings in May—is being fueled by improved market stability, easing global tensions, and successful block deals. These factors have helped restore investor confidence and create a more conducive environment for quality issuers.

REAL ESTATE

India’s real estate sector continues to draw institutional capital, with increased focus on premium segments. ASK Property Fund, backed by Blackstone’s ASK Group, announced the first close of its luxury housing-focused fund, raising ₹500 crore. Launched with India Sotheby’s International Realty, the ASK Curated Luxury Assets Fund I targets ₹1,000 crore, with a ₹500 crore greenshoe option, and expects to close by year-end.

Meanwhile, Embassy Group secured ₹10.6 billion in strategic equity funding for its commercial arm, Embassy Developments. The deal highlights continued investor confidence in India’s Grade A office market and reflects broader momentum across both luxury residential and commercial real estate segments.

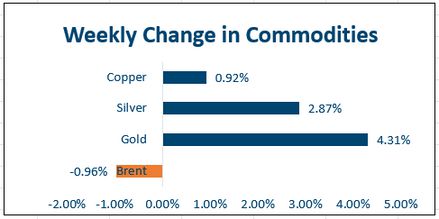

COMMODITIES

Typical risk off moves were seen across commodities. Brent ended the week 1% lower at USD 64.8 per barrel.

Previous metals surged on a sell off in long end US treasuries. Gold and Silver surged 4.8% and 3.7% respectively to USD 3357 and USD 33.5 per ounce respectively

Base metals were mixed with LME Copper gaining 1.7% and Aluminum dropping 0.7%. Dalian Iron ore fell 0.2%

Our Views: What we Like?

Equities

We believe valuations in the Midcap and Smallcap space remain elevated.

We recommend investing in selective large caps for those with a long term horizon. The trend in Nifty50 remains mostly sideways as we are likely in a phase of time correction.

Bonds & Rates

We see limited downside in 10y Yields from current levels. Sell off in longer end US treasuries will likely weigh on domestic Bonds as well.

We expect the terminal rate in this cycle to be 5.50%

We may see a bit of negative reaction in domestic bond markets as the RBI transferred a surplus of Rs 2.69 lakh crs, lower than market expectations of Rs 3 lakh crs.

Commodities

We believe we have seen the bottom in Brent. However we do not expect a sharp reversal. We can see consolidation in the USD 58-70 band

We are mildly bullish on Base metals.

We believe long precious metals is a crowded traded but if US treasuries continue to sell off, we may see further upside of 3-4%.

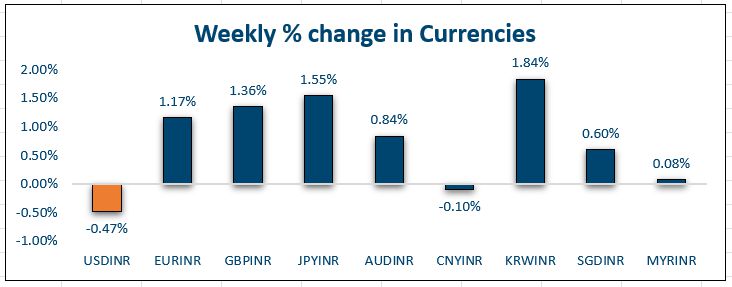

FX

We expect the Dollar to continue trading with a weak bias.