Billionz Global Weekly Newsletter

Global Development & Global Equities

MARKETS UNNERVED AS TRUMP REAFFIRMS TOUGH TARIFF STANCE

Risk sentiment was dented as President Trump said the tariffs on Canada and Mexico would be hiked as scheduled on 4th March. The tariffs on China would also increase by 10% on the same day. He also added that reciprocal tariffs would go into effect on 2nd April. Trump said that Europe would face 25% tariffs as part of his reciprocal tariffs. The US Treasury secretary said that Mexico has proposed matching the US’ tariffs on China. He urged Canada to do the same as well. Trump’s talks with the Ukrainian president ended on a sour note. This has raised concerns in the Eurozone about the risk of the US cutting Ukraine loose and striking a deal with Russia that is unfavorable for Ukraine.

After disappointing Michigan consumer sentiment and Services PMI last week, this week we saw some more evidence of the US economy slowing down. Pending home sales were the lowest ever in January due to high mortgage rates and high home prices.

Jobless claims rose to the highest in 3 months, and personal spending was down 0.2% every month in January. There is chatter of a stagflation-like situation developing in the US. The market is pricing in 2.7 cuts by the end of 2025 compared to 1.8 cuts last week. The market is pricing in a 70% chance of a cut in the June Fed meeting.

India Q3 GDP and GVA prints came in line with expectations at 6.2% yoy. Q2 print was revised higher to 5.6% from 5.4% yoy.

India’s April- Jan fiscal deficit at Rs 11.7 lakh crs reached 74.5% of the full-year revised target compared to 63.6% in the corresponding period of the previous year.

NIFTY V/S GLOBAL MARKETS

The S&P 500 ended the week 1% lower on account of a strong recovery on Friday. The weak gross operating margin outlook of Nvidia dampened sentiment on Wall Street. This was after tepid guidance from Wall Street a week ago. DAX and FTSE were up 1.2% and %.,7% respectively. CAC ended the week 0.5% lower Equities across Asia sold off this week.

Major Asian indices witnessed notable declines, with the Nikkei falling 4%, Hang Seng down 2.3%, CSI300 slipping 2.2%, and Kospi plunging 4.6%. The Jakarta index saw the steepest drop of 7.8%, while Singapore’s Straits Times eased 0.9% and Malaysia’s KLCI declined 1%.

Domestic Equities

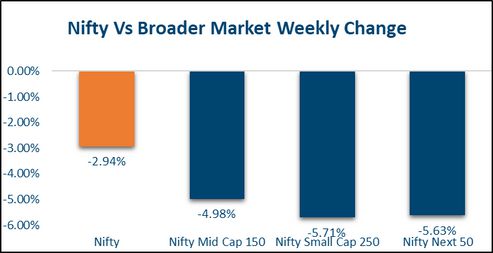

Nifty50 saw a sell off of 3% this week. Broader markets saw even deeper cuts. Midcap100 and Smallcap250 indices were down 5.1% and 5.7% respectively.

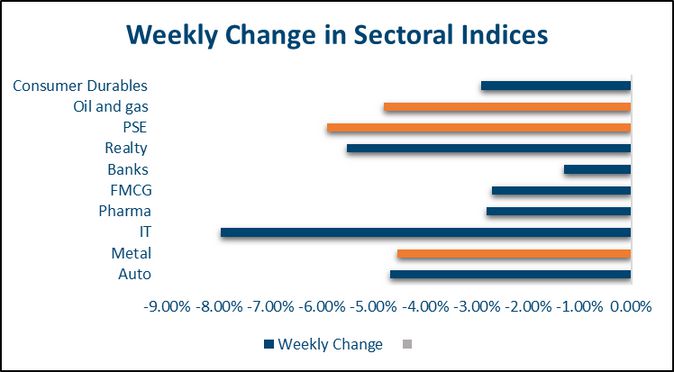

Below is how various sectoral indices performed:

IT -8%, FMCG -2.7%, Pharma -2.8%, Auto -4.7%, Bank Nifty -1.3%, Realty -5.5%, Metals -4.5%, Energy -5%, Consumer Durables -2.9%

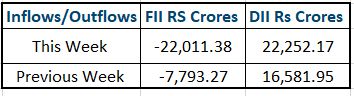

FPIs sold net USD 4bn in domestic Equities in February

The average sales surprise for Nifty50 has been about 11% and Earnings surprise has been -5.5% as per latest reported Earnings.

Based on trailing 12m and forward 12m, below is how the PEs stand:

Nifty50: 20.6, 18.5, Midcap100: 32, 27.7, Smallcap250: 23, 21

Fixed Income, IPO, and Institutional Deals

REAL ESTATE:

Foreign investment in India’s real estate market has been inconsistent in recent quarters, mainly due to high interest rates in Western countries and ongoing geopolitical tensions. Political changes in the U.S. further add to the uncertainty of Western capital inflows into the sector in 2025.

Despite these challenges, experts see a 9-10% increase in overall real estate investment as a positive sign for India’s property market. Notably, nearly 90% of foreign capital entering Indian real estate comes from Asia and Southeast Asia, with most investments directed toward the industrial and warehousing sectors, driven by strong growth prospects and increasing demand.

INITIAL PUBLIC OFFERING (IPO):

India’s IPO market has slowed down due to weak investor sentiment, declining stock prices, and poor post-listing performance. Many of the 44 SEBI-approved companies have postponed their IPOs, with some reconsidering valuations.

In January, ₹4,845 crore was raised through IPOs, a sharp decline from ₹25,500 crore in December. February saw ₹10,900 crore, largely driven by Hexaware Technologies’ ₹8,750 crore issue.

Despite the current slowdown, a market revival is expected in H2 2025, with major IPOs from Tata Capital, HDB Financials, Lenskart, PhonePe, and LG Electronics India, each exceeding ₹10,000 crore.

PRIVATE EQUITY AND VENTURE CAPITAL:

During the week ending February 28, private equity activity was dominated by healthcare deals, with overall transaction value more than doubling to $564 million—primarily driven by KKR’s acquisition of a controlling stake in Healthcare Global Enterprises Ltd from CVC Capital, which made up roughly 75% of the total.

Mumbai-based Motilal Oswal Alternates also made its first control-oriented move of the year by acquiring a majority stake in API maker Megafine Pharma Pvt Ltd.

M&A momentum continued with several crossborder transactions, including Mumbai’s Camlin Fine Sciences Ltd, which announced plans to acquire a majority stake in French firm Vinpai SA to enhance its product offerings in food and cosmetics.

FIXED INCOME:

Yield on the US 2y and 10y came off 19bps each to 4.18% and 4.21% respectively

10y Yields across the Eurozone and the UK were down 6-11bps

Yield on the benchmark 10y rose 2bps to 6.73%

1y OIS ended 5bps lower at 6.24%. 5y OIS ended 9bps lower at 5.99%

While FPIs have invested a net USD 1.66bn through the FAR route in Feb, they have pulled out USD 450mn via the general and VRR routes.

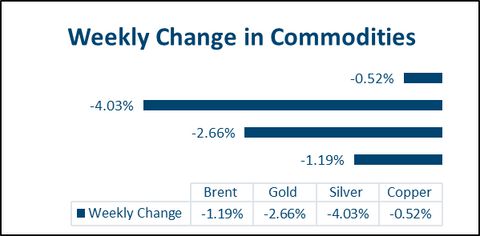

COMMODITIES:

Brent was down 2.2% for the week at USD 72.8 per barrel. US and European natural gas prices were down 9.5% and 6%, respectively

Base metals saw a asell-offf this week on risk aversion. LME Aluminum and Copper were down 3.1% and 2.1%, respectively

Precious metals sold off on Dollar strength. Gold was down 2.7%, and Silver was down 4% for the week.

Ideas and Opportunities

Our Views : What we like?

Equities:

Nifty50 is at a very crucial weekly technical support around 22100 (Lower Ichimoku cloud support and 38.2% Fibobacci retracement). Weekly close below this level would open doors for 20700, where there is a 50% retracement and a gap support.

We believe current levels are attractive in terms of valuations to invest in large caps for building a long-term investment portfolio. We prefer value over growth, defensives over high beta, and large caps over midcaps and small caps.

Fixed Income:

We believe there is still potential for US treasuries to rally. The 2s10s has flattened, and it could invert again as markets talk about a stagflation-like situation.

We expect the India 10y government bond yield to be steady in the 6.60-6.85% range over the next few weeks.

Levels around 5.90% seem attractive to pay on 5y OIS to convert floating rate liabilities to fixed rate.

Commodities:

We believe strength in previous metals could fizzle a bit on account of Dollar strength. We could see Gold and Silver correct from current levels by 2-4%

We continue to remain bearish on Brent. It is approaching our target of USD 70 per barrel.

We continue to remain neutral on Base metals.

FX:

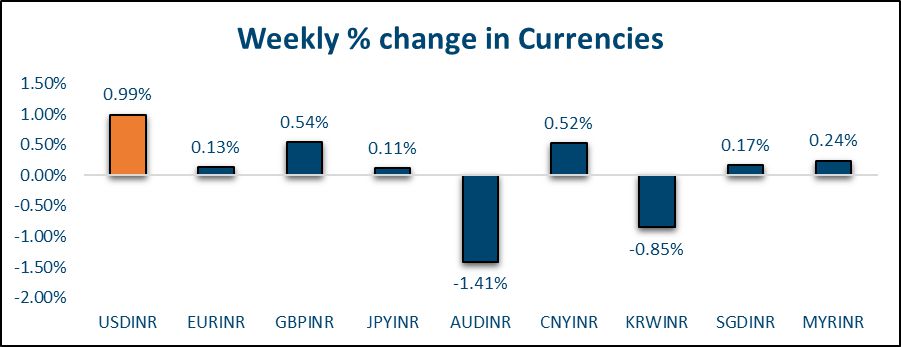

We continue to believe that the Dollar could see tailwinds on account of the uncertain outlook resulting from Trump’s trade policies.