Billionz Global Weekly Newsletter

Global Developments & Global Equities

RECIPROCAL TARIFF ANNOUNCEMENT ROCKS GLOBAL RISK SENTIMENT

The date that the world was looking at with bated breath was 2nd April aka… ‘the liberation day’. Trump administration unveiled the reciprocal tariffs and that sent shockwaves through the global financial markets.

These tariffs have the potential to rock existing global trade order and prove to be extremely disruptive. It will be interesting to see how countries respond I.e. whether they retaliate or renegotiate with the Trump administration.

There was classic risk aversion and flight to safety seen across assets. US March labor data that came out on Friday was mixed with headline NFP print beating estimates (228k vs exp 140k), Unemployment rate ticking higher to 4.2% from 4.1% and Average Hourly Earnings Growth coming in at 3.8% yoy against expected 4% yoy. Key data to look forward to in the coming week will be the US March CPI print and minutes of the latest Fed meeting. Market is pricing in 4 cuts by the end of 2025 compared to 3 as on last week.

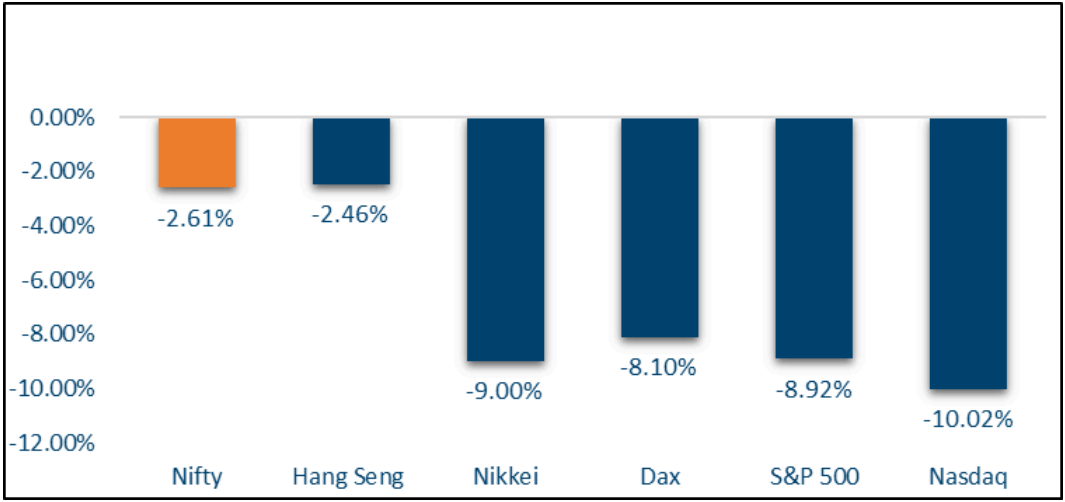

NIFTY V/S GLOBAL MARKETS

There was a bloodbath in global equities this week.

Domestic Equities

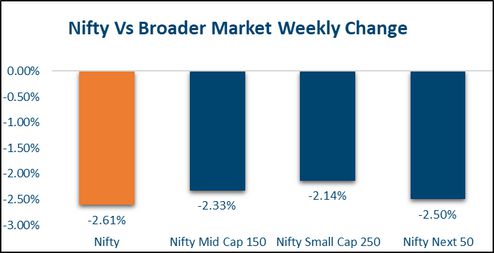

Nifty50 was relatively resilient, dropping just 2.7% to 22904. Broader indices were also resilient with Midcap100 and Smallcap250 indices down just 2% and 2.1% respectively for the week.

GIFT Nifty futures is indicating a further 2.7% cut for the Nifty on Monday open

In terms of style, growth and momentum underperformed while low volatility and liquidity outperformed.

Below are the valuations in terms of P/E across large, mid and smallcaps based on trailing 12m and forward 12m Earnings

Nifty50: 21.3, 19.3, Midcap100: 33.8, 28.2, Smallcap250: 24.4, 24.2

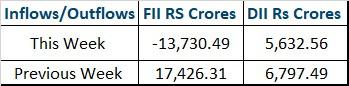

FPIs have sold USD 1.2bn of domestic Equities in the first few sessions of April

Fixed Income, IPO, and Institutional Deals

REAL ESTATE:

Foreign firms accounted for over 62% of office space leasing across India’s top nine cities in Q1 2025, led by tech, BFSI, and engineering sectors, according to CBRE. Bengaluru, Delhi-NCR, and Hyderabad saw the highest uptake, reaffirming their status as key business hubs.

Meanwhile, housing sales declined in Bengaluru and Delhi-NCR due to rising prices and job uncertainty, as per Knight Frank. Despite a 4% overall rise in residential sales across major cities, these two markets saw notable drops, while Mumbai, Pune, and Hyderabad maintained healthy demand.

PRIVATE EQUITY AND VENTURE CAPITAL:

Overall activity in the PE & VC space was muted for this week, weighed down by the absence of large transactions and limited private equity activity. Venture capital firms closed a few notable deals, but overall momentum remained weak.

Private equity and venture capital deal value dropped 66% to $281 million across 31 transactions, down from $817 million last week. The week’s highlight was a fresh investment in Haldiram’s by Alpha Wave Global and Abu Dhabi’s International Holding Company, following Temasek’s recent $1 billion bet—though financial details of the latest deal remain undisclosed.

M&A activity also slowed down this week with only four deals, down from 11 last week. The biggest was ITC’s takeover of Aditya Birla Real Estate’s pulp and paper business, amid pressure from cheap imports, weak demand, and rising input costs.

INITIAL PUBLIC OFFERING (IPO):

The IPO market remains quite active despite broader market volatility. Four SME IPOs are lined up between April 8–11, including Entice Retail, Technocrat Engineering, and Orbis Financial, aiming to raise funds for business expansion and working capital needs. In a major development, Tata Capital has confidentially filed for a ₹15,000+ crore IPO, marking one of the largest upcoming issues. The offer will include a share sale by Tata Sons and the International Finance Corporation (IFC). This move is part of Tata Group’s broader plan to list key financial services entities ahead of potential regulatory changes.

FIXED INCOME:

US yield curve saw a parallel shift lower on recession fears and safe haven demand. US 10y yield dropped 21bps to 3.99%, lowest level since Oct’24. US 2y yield too fell 23bps to 3.65%.10y Yields across Eurozone and UK were down 10- 22bps this week. Yield on the 10y JGB came off 32bps. Yield on the India benchmark 10y fell 12bps to 6.46% this week. Large part of the move happened before announcement of reciprocal tariffs as RBI announced a Rs 80000crs OMO purchase. By way of these OMOs, the RBI is replacing maturing VRRs by long term durable liquidity.5y OIS fell 17bps to 5.73%, lowest level since Feb’22. 1y OIS fell 13bps to 5.91%. There is expectation that the RBI will probably be able to cut rates deeper given the negative impact on growth from tariffs and also given how Rupee has appreciated in real terms in recent times. There is also chatter about the possibility of RBI cutting rates by 50bps at the policy in the coming week. The RBI rate decision is due on Wednesday. While the terminal repo rate in this cycle was earlier expected to be 6%, there is possibility that RBI may be able to cut the Repo rate to as low as 5.5% given the downside risks to growth.

FX and Commodities

FOREIGN EXCHANGE:

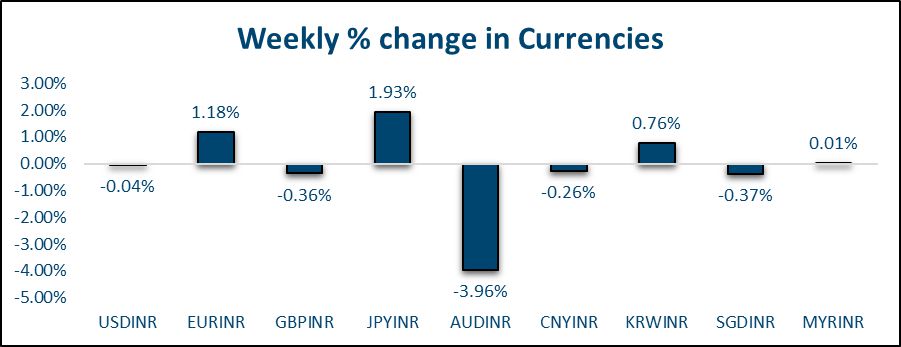

Dollar weakened significantly against majors, except commodity currencies. SEK (+11%) was the best performer followed by CHF, DKK, EUR, JPY and GBP, all of which appreciated 5.4-5.7% against the Dollar. Commodity currencies AUD (-2.9%) and NZD (-0.7%) were the major underperformers. As far as Asian currencies are concerned, currencies of those countries which were seen benefitting from either lower impact on economy on account of less reliance on exports to US or relatively lower reciprocal tariff rates (which would help them in increasing export share to US) outperformed at the expense of the rest. INR (+1.6%) and PHP (+2.7%) were the best performers while TWD (-1.2%), IDR (-1.6%) and THB (-1.5%) were the worst performers. Offshore Yuan weakened 0.5% against the Dollar this week. Rupee was volatile this week, trading a 84.95-85.75 range. It eventually ended the week onshore at 85.24, strongest since Dec’24. However, it weakened in offshore to end at implied spot of 85.53, tracking overall risk aversion and sell off in US equities. It was the third successive week of strength for the Rupee. Forwards got paid with 1y forward yield rising 16bps to 2.36% and 5y yield rising 34bps to 3.11%. This was because US Rates dropped more on fears of a recession. 3m ATMF implied volatility spiked 30bps to 4.05%

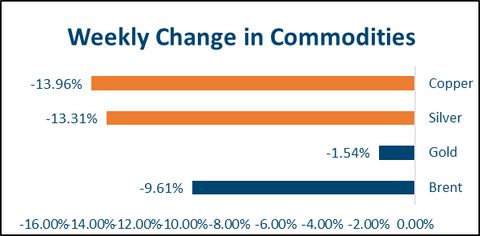

COMMODITIES:

Brent dropped 11% this week to USD 65.5 per barrel. Worsening the already poor sentiment from reciprocal tariffs, was OPEC’s decision to not only go ahead with it’s planned production increase but also nearly triple the expected increase figure. Base metals too had a torrid week with LME Copper and Aluminum 3 month contracts dropping by 10.4% and 6.6% respectively. Among precious metals, Gold was down 1.5% to USD 3038 and Silver was down 13.3% to USD 29.6

Our Views: What we Like?

Equities:

We see the recent lows around 21800 get retested on Nifty50 given this week’s price action. We are almost certain to break through the 22800 support on Monday. We remain cautious in the near term given the tariff related uncertainty. We prefer large caps over mid and smallcaps and value over growth. There is potential for the Nifty50 to correct another 5-8%. However that would present an attractive buying opportunity for long term investors. US equities were due for a correction given the froth. S&P500 is down about 12% in a month. Stocks like Apple, Meta, Nvidia, Amazon, Alphabet are down 15-20% in the last one month. We are watching this space closely as it would present an excellent buying opportunity. We are looking to add US equities to our model portfolio on first signs of the sell off abating.

Fixed Income:

We continue to remain bullish on US Rates and treasuries. 5y OIS at 5.73% looks attractive to pay to lock in a fixed rate. 10y benchmark bond yield could move lower to 6.35-6.40%. We remain bearish on credit spreads and expect them to widen.

Commodities:

We believe gold will continue to see safe haven demand while base metals and crude could continue to remain under pressure in the near term. Brent has broken a crucial support around USD 66 per barrel and could head lower towards USD 58-60 per barrel

FX:

We expect the Dollar to weaken against major currencies. Concerns over growth will likely dominate concerns over inflation. This might cause the market to expect faster rate cuts by the Fed.