Billionz Multi-Asset Weekly Newsletter

Global Development

- The US government shut down as Democrats and Republicans failed to agree on a spending plan.

- Healthcare spending remains the key contentious issue.

- Government employees furloughed; essential workers working without pay.

- Shutdown expected to last at least into next week.

- The US jobs report for this week has been postponed due to the shutdown.

India / RBI Updates:

- RBI keeps policy rates unchanged but signals possible future easing.

- Introduces measures to ensure credit flow and transmission of previous rate cuts.

- Banks are allowed to fund M&A transactions.

- Risk weights for project finance are now stage-dependent.

- Thresholds raised for loans against shares and IPO financing.

- Proposes removing the ceiling on lending against listed debt securities.

- Supports exporters: extends the merchanting trade window and EEFC account conversion period at GIFT IBUs.

- The retracts rule discourages lending to ultra-large corporate borrowers.

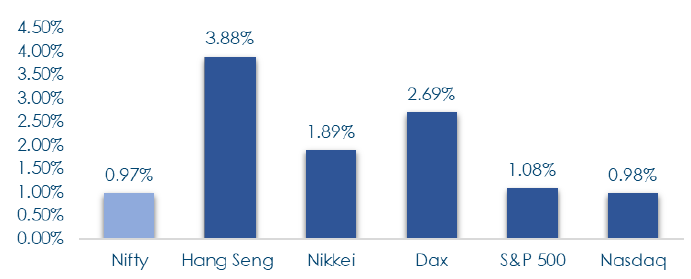

Global Equities:

This is how Global Equities performed this week.

Domestic Equities:

- PE valuations across key indices (trailing/forward 12m EPS): Nifty50 22 / 21.2, Midcap100 32.1 / 27.7, Smallcap250 28.9 /27.3, Nifty Next 50 23 / 23.1. The market expects 4.9% EPS growth for Nifty50 over the next 12 months.

- In terms of factors, Value outperformed while Growth underperformed this week.

- FPIs sold net USD 2.7bn of domestic equities in September. It was the third straight month of outflows. In the first few sessions of Oct, FPIs have sold net USD 433mn.

- Top Gainers: Prozone Realty (+34%), Sai Silks (+21%), Sammaan Capital (+19.7%)

- Top Losers: BME Ventures (-28.9%), Wonder Electricals (-12.7%), VMS TMT (-11.2%)

- Flows: FII -₹8,347 cr | DII +₹13,013 cr (vs -₹19,570 cr & +₹17,411 cr prev. week)

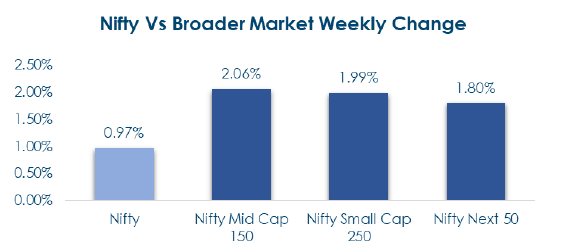

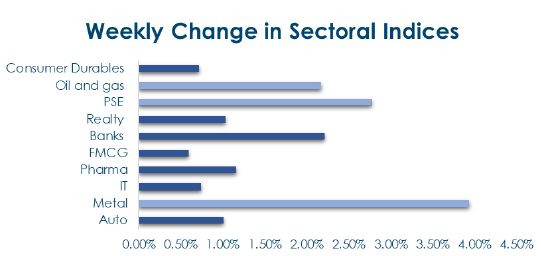

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices performed this week:

Fixed Income

- US Yields: 2y +4bps to 3.58%, 10y -2bps to 4.12%; UK & Eurozone mostly steady

- India 10y G-sec: 6.50–6.61%, closes at 6.51%; new 10y cutoff 6.48%

- OIS & Liquidity: 1y OIS 5.43%, 5y OIS 5.66%; banking surplus Rs 1.7L cr, call rate 5.40%

- Credit Spreads: 10y AAA PSU 48bps, AAA NBFC 82bps

- FPI Flows: +USD 1.3bn in Sep; +USD 300mn in early Oct

Private Equity & Venture Capital

- Deals fell to 23 from 38; total value halved to $540M from $1.2B.

- Top funding: Hillhouse Investment $205M in an education company.

- Other notable raises: Vitruvian Partners (Hiranandani Financial Services, PostHog $75M, Kapiva $60M, Apex Hospitals $30M.

- Activity picked up: 9 deals vs 6 last week.

- Highlight: Abu Dhabi’s IHC invests nearly $1B to acquire a controlling stake in Sammaan Capital.

- Other deals: RateGain acquires US travel marketing platform Sojern; Lupin buys VISUfarma; Indegene acquires BioPharm Parent (US); BLS International buys Trefeddian Hotel, UK.

IPOs

- India’s IPO action heats up next week with marquee listings grabbing attention.

- Tata Capital IPO (₹15,512 cr): Oct 6–8, price band ₹310–₹326; mix of fresh issue & offer for sale; strong anchor support already secured.

- LG Electronics India IPO (₹11,607 cr): Oct 7–9, price band ₹1,080–₹1,140; fully offer for sale; one of the largest consumer electronics listings in recent years.

- Overall pipeline: ~29 IPOs next week across sectors, including pharma, infrastructure, mainboard & SME listings (e.g., Rubicon Research, Anantam Highways Trust).

- Market watch: Tata Capital and LG IPOs expected to set the tone for investor appetite in this busy IPO season.

Real Estate

- WSB Real Estate: ₹150 cr ($17M) invested in Bengaluru warehousing; 74% stake with KSH Infra. Mark’s second logistics bet after residential AIFs.

- WeWork India IPO: Price band ₹615–648/share; valuation ~$980M. Opens Oct 3, 46.3M shares sold by Embassy & WeWork affiliate.

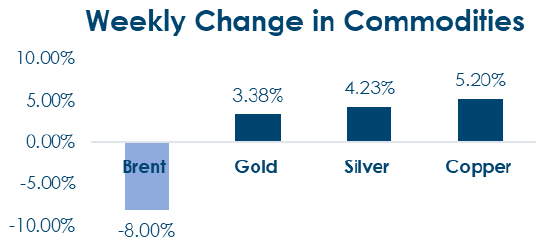

Commodities

- Crude has been under pressure amid expectations that OPEC+ will discuss fast-tracking supply hikes

- Copper rallied on supply disruptions from Indonesia

- Gold gained for the 7th straight week as the US government shutdown added to uncertainty.

What’s New in the World of Wealth Management?

The RBI has introduced significant reforms to expand corporate credit access and stimulate capital market activity. Banks are now allowed to finance mergers, acquisitions, and IPOs more freely, facilitating corporate growth and market participation. Additionally, the cap on loans against shares and listed debt securities has been raised fivefold to ₹1 crore, providing greater liquidity to large companies. These measures aim to ease credit flow to corporates and support investment activity across sectors.

RBI has also proposed a major overhaul of external commercial borrowing (ECB) regulations, allowing companies to raise up to $1 billion or 300% of their net worth, whichever is higher. Firms regulated by RBI, SEBI, IRDAI, or PFRDA will no longer face borrowing limits under this framework, signaling a liberalization of access to foreign capital. Together, these reforms are expected to create a more dynamic corporate financing environment, enabling businesses to pursue growth opportunities while supporting overall market stability.

Our Views: What we Like?

Equities

Time correction continues in Nifty50. 24300-25300 seems to be the range for now. We believe the break is more likely

to happen on the upside eventually. It is time for active sector allocation and stock selection, as beta moves may be

elusive. Among sectors, we prefer staying away from IT. We prefer Auto, FMCG, and consumer Durables.

Fixed Income

Close to 6.60% levels on the 10y are attractive for adding duration to the portfolio. Current levels on 5y OIS are

attractive to convert floating-rate INR exposures to fixed.

Commodities

We continue to remain bullish on precious metals given the weak Dollar outlook and shutdown-induced uncertainty. We

believe Silver may outperform Gold. We are also upbeat on base Metals. We remain neutral on Brent.

FX

We continue to remain bearish on the Dollar, especially against majors. The dollar may not weaken as much against EM

currencies.