Billionz Multi-Asset Weekly Newsletter

Equities Catch Their Breath as Commodities Rally

Weekly Global Developments:

- Fed Policy Outcome: The Fed delivered a widely expected 25 bps rate cut, though the decision was not unanimous. 9 members voted for a cut, 2 preferred the status quo, and 1 voted for a deeper 50 bps cut.

- Powell’s Commentary: Chair Powell noted the decision was a close call, highlighting that prevailing conditions justified arguments for both a rate cut and maintaining current rates.

- Liquidity Measures: The Fed also announced USD 40 bn per month in T-bill purchases to support system liquidity and ensure smooth policy transmission.

- Forward Guidance: The median dot plot signals only one rate cut in 2026, contrasting with market expectations of just over two cuts by the end of 2026.

- Key US Data Ahead: November payrolls and retail sales data (Tuesday) will be closely watched for further cues on growth and consumption trends.

- Global Central Bank Watch: ECB & BoE policy decisions – Thursday & BoJ policy decision – Friday

Global Equities:

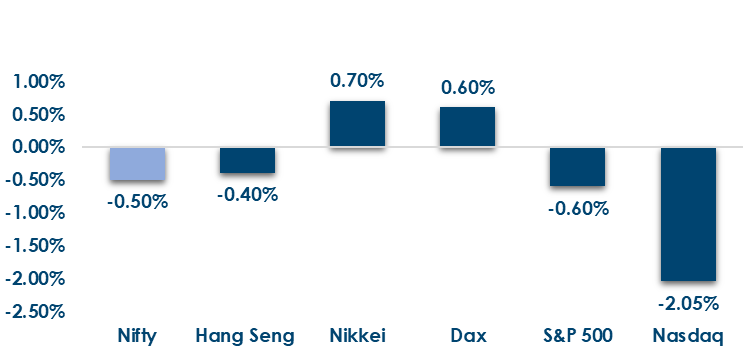

This is how Global Equities performed this week.

Domestic Equities

- Global equities saw mixed performance over the past week, with gains in Asia led by Kospi (+1.6%) and Nikkei (+0.7%), while US and European indices largely edged lower, including S&P 500 (-0.6%), CAC (-0.6%), and FTSE (-0.2%).

- Valuations remain elevated across the board, with the Nifty 50 trading at 21.5x TTM and 21.2x forward earnings, while midcaps are costlier at 34.9x and 29.2x, and smallcaps at 30.5x and 26.0x, showing only modest easing on a forward PE basis.

- FPIs have sold net USD 2bn of domestic Equities in December so far

- FIIs remained net sellers this week at ₹4,415.7 cr, though selling eased versus last week, while DIIs stayed strong buyers at ₹8,767.4 cr, continuing to cushion market flows.

- Transformers & Rectifiers, Hindustan Zinc, and GE Vernova T&D led gains, while Reliance Infrastructure, InterGlobe Aviation, and Reliance Power were the top laggards for the period

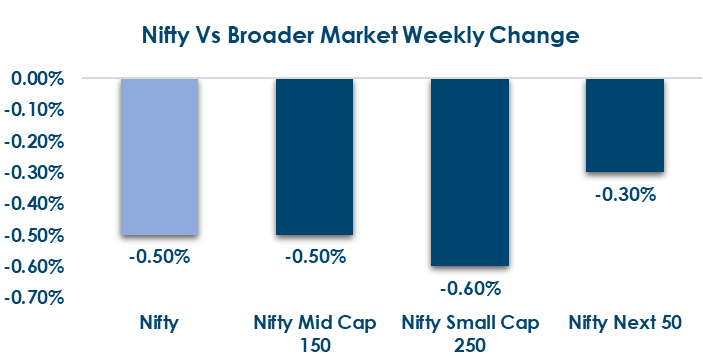

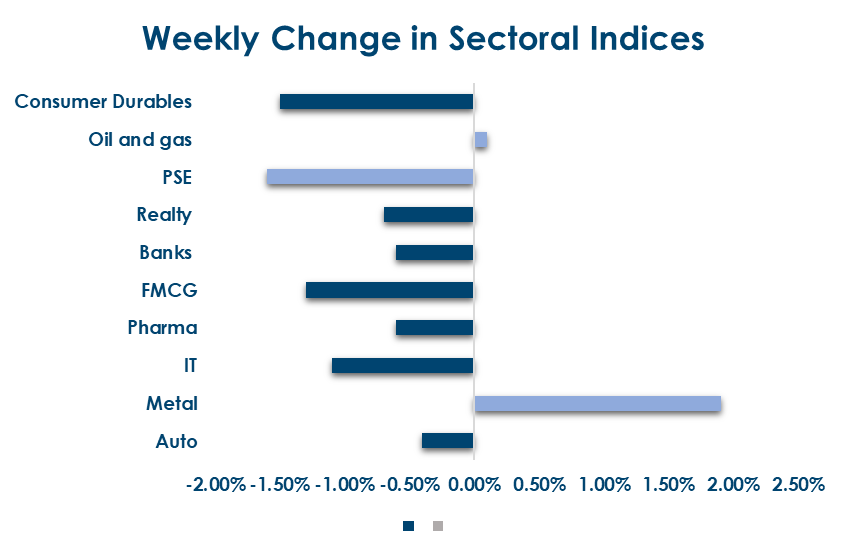

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices performed this week:

Fixed Income:

- Global Rates: US Treasuries saw a mild flattening, with the 10y yield up 2 bps to 4.18% while the 2y fell 5 bps to 3.52%; 10y yields remained largely steady across the UK, Eurozone, and Japan.

- India Rates & Flows: Domestic bonds sold off on expectations of an end to the rate-cut cycle and a lower-than-expected ₹1 lakh crore OMO, lifting the 10y G-sec 10 bps to 6.59% and 5y OIS to 5.92%, while liquidity stayed comfortable with a ₹1.5 lakh crore surplus, MIBOR at 5.24%, USD 800 mn FPI debt outflows, and spreads at 54 bps (AAA PSU) and 88 bps (AAA NBFC).

Real Estate:

- Investors are moving from direct real estate ownership to fund structures for better governance, diversification, and risk management, with frameworks like GIFT City, boosting institutional participation and India’s global competitiveness.

- The $300 million real estate fund launched by BNW Developments (Vivek Oberoi) with a UAE partner saw strong early commitments, highlighting demand for professionally managed real estate opportunities.

IPOs:

- IPO Activity Heats Up: India’s primary markets are witnessing one of the busiest IPO phases of the year, with a strong lineup including ICICI Prudential AMC, Corona Remedies, Wakefit Innovations, Nephrocare Health, and several others across mainboard and SME segments, reflecting robust investor appetite across sectors.

- Structural Trend Emerging: The much-anticipated ICICI Prudential AMC IPO highlights confidence in India’s financial and asset management space, while the broader surge in listings points to a structural shift, with an annualised USD 20 billion IPO run rate increasingly becoming the new normal for Indian markets.

Private Equity & Venture Capital:

- Funding rebounded to normal levels in the five days ended December 12, with $1.44 bn raised across 24 deals, more than double the previous week, largely driven by two large transactions accounting for over 90% of total value, including CCI’s approval of IHC’s ~$1 bn investment in Sammaan Capital.

- M&A activity slowed to eight deals, though ticket sizes were larger, led by Biocon Ltd’s $5.5 bn transaction to consolidate Biocon Biologics as a wholly owned subsidiary through a mix of share swaps and cash.

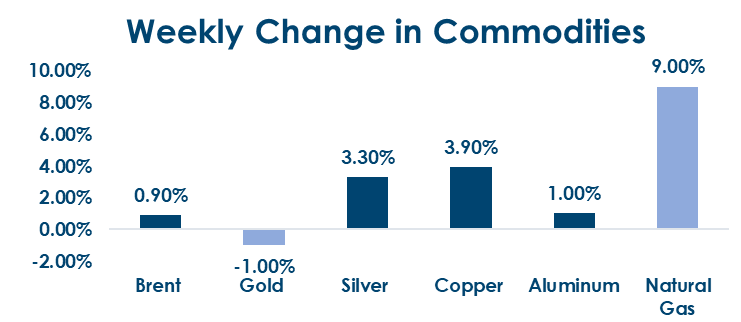

Commodities: Commodities were mixed: energy prices saw sharp weakness with Brent down 4.1% to USD 61.1 and US natural gas plunging 22% to USD 4.1, base metals softened modestly (Aluminium -1%, Copper -0.9%), while precious metals outperformed with Gold up 2.4% to USD 4,299 and Silver surging 6.2% to USD 61.96. LME 3M Copper hit a fresh all-time high this week of USD 11952 before giving up gains to end at USD 11515. Precious metals were buoyed by a weaker Dollar

What’s New in the World of Wealth Management?

India’s capital markets are undergoing a meaningful structural reset, driven by regulatory reform and evolving investor behaviour. The government’s move to comprehensively rewrite laws governing insurance and securities markets signals an intent to modernize legacy frameworks, improve regulatory clarity and attract long-term capital. Proposed changes include higher foreign participation limits in insurance and streamlined market regulations, which could deepen liquidity, broaden ownership, and align India’s markets more closely with global standards. At the same time, India’s savings landscape is shifting decisively toward financial assets, with domestic household savings increasingly flowing into equities, mutual funds and market-linked instruments. This domesticisation of flows has enhanced market stability but also raises concerns around risk awareness, valuation sensitivity, and the need for stronger investor education as retail participation rises.

Alongside financial markets, real assets—particularly premium and luxury real estate—are becoming an important capital allocation channel. Strong demand for high-end residential property across metros and emerging cities reflects rising wealth concentration, insourcing of global roles, and greater preference for tangible assets as a store of value. This trend is closely linked to capital markets, as equity wealth creation increasingly feeds into real estate investment, reinforcing asset-price cycles. Taken together, regulatory reform, domestic savings-led market participation and cross-asset capital flows are reshaping India’s capital markets into a more self-sustaining, domestically anchored system—offering depth and resilience, but also requiring disciplined regulation and informed participation to manage emerging risks effectively.

Our Views: What we Like?

Equities: Nifty recovered quite well over the last couple of sessions from the weakness seen earlier in the week. Nifty50 seems to

be taking support around the 50DMA of 25745. We remain constructive on Indian equities and are looking to add exposure, mainly through large caps. Among sectors, we are overweight on Banks and IT.

Fixed Income: We believe current levels of 10y are attractive to add duration to the portfolio. It is time to execute carry rolldown strategies. The yield curve is steep, and RBI OMO purchases may cap upside at the far end of the curve. Our 5y OIS target of 5.90% was reached this week

Commodities: We continue to remain bullish on precious metals in a weak Dollar environment. Stable risk sentiment overall should impart tailwinds to base metals as well. Energy complex, especially Brent, may remain under pressure due to oversupply concerns.

FX: We continue to expect the Dollar to trade with a weak bias. We see more Fed rate cuts in 2026 than what the market is pricing in, given weakening labor market conditions