Billionz Multi-Asset Weekly Newsletter

Markets Await Direction Amid Tariff Threats and Budget Cues

Global Developments:

- Global geopolitics: Headlines were dominated by the reported US capture of Venezuelan President Maduro. Markets are assessing the potential impact on crude supply and the likely timelines.

- US macro: December NFP came in weaker than expected at 50k vs 70k, while the unemployment rate was slightly lower at 4.4% vs 4.5%. Markets are now pricing in two 25 bps Fed rate cuts by the end of 2026.

- Trade & Tariffs: Domestic sentiment was impacted after Trump backed the Graham–Blumenthal bill, which proposed 500% tariffs on countries importing Russian crude. The US Supreme Court’s ruling on the legality of Trump tariffs will be closely watched next week.

- India growth outlook: Advance estimates peg FY26 nominal GDP growth at 8% and

- real GDP growth at 7.4%, compared to 6.5% real GDP growth in FY25.

Global Equities

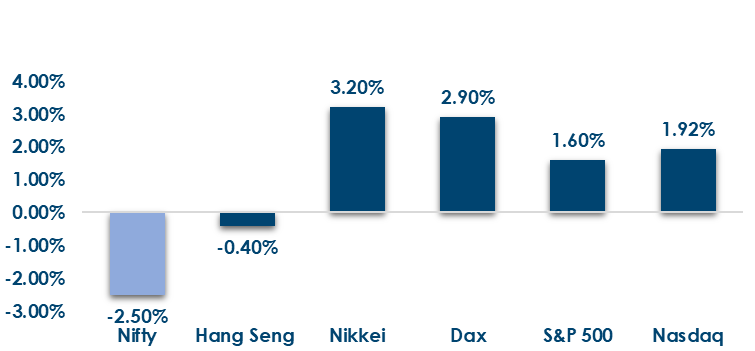

This is how Global Equities performed this week.

Domestic Equities

- Global equities ended the week mostly higher, led by strong gains in Asia (Kospi +6.4%, Nikkei & Taiwan +3.2%) and Europe (DAX +2.9%, CAC +2.0%), while US markets rose modestly (S&P 500 +1.6%); Hang Seng was the lone laggard (-0.4%).

- Based on trailing (past 12 months) vs forward (next 12 months) P/E, Nifty50 is fairly valued at 21.2x → 20.8x, while Midcaps (34.5x → 29.5x) and Smallcaps (29.9x → 25.6x) remain expensive but look more reasonable on expected future earnings.

- In terms of quality and low volatility, it outperformed this week, while growth underperformed

- FPIs have sold net USD 1.3bn of domestic equities in Jan so far

- FIIs remained net sellers at ₹9,050 crore, while DIIs continued buying with ₹17,338 crore inflows this week, slightly lower than last week.

- Ipca Labs (+12.2%), Netweb Technologies (+9.5%), and Emcure Pharma (+7.7%) led gains, while Transformers & Rectifiers (-18.5%), Elecon Engineering (-15.5%), and Premier Energies (-15.2%) were the top losers.

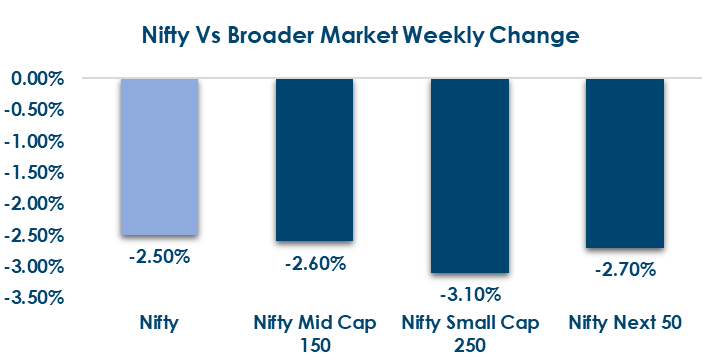

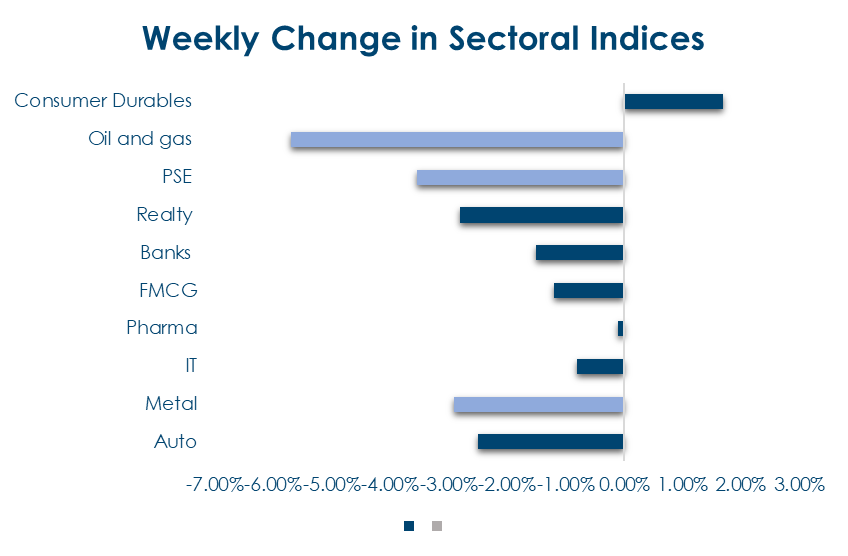

Below are the graphical representations of how key benchmark indices performed this week & how sectoral indices

performed this week:

Fixed Income:

- Global Rates: US yields saw a bear flattening (2Y +8 bps to 3.53%, 10Y flat at 4.16%), while UK and Eurozone yields softened, and Japan’s 10Y JGB eased to 2.08%.

- India Rates & Flows: The 10Y G-sec edged up to 6.64%, liquidity stayed near-neutral (MIBOR 5.34–5.54%, OIS largely unchanged), short-term rates remain mixed (3M T-bill 5.31%, CD 6.62%), and FPIs added USD 500 mn to debt so far in January.

Real Estate:

- Sundaram Alternates raised ₹1,000 crore for its 5th real estate credit fund (target ₹1,500–2,000 crore by March), focusing on senior secured lending to cash-generating residential projects, with 18–19% historical IRRs and exits above 20%.

- Certus Capital secured an anchor commitment for its second fund (target ₹500 crore), with TFCI committing ₹50 crore, aiming for ~20% gross returns across real estate opportunities in key urban markets.

IPOs:

- Busy IPO Week Ahead (Jan 12): Six IPOs are opening for subscription, led by Amagi Media Labs on the mainboard, alongside multiple SME offerings, highlighting continued primary market momentum.

- Listings & Market Focus: Five IPOs are set to list (1 mainboard – Bharat Coking Coal, 4 SMEs), boosting near-term liquidity. Investor attention will split between Amagi’s scale and valuation and selective SME performance, with listings indicating primary market risk appetite.

Private Equity & Venture Capital

- Deal activity in India picked up, with investments rising ~60% WoW to $404M across 27 deals. Largeticket deals remained limited, with only two deals above $100M accounting for ~75% of total value.

- Apax Partners acquired a minority stake in iD Fresh Food (~₹1,500 crore), while LKP Finance entered fintech via Gyftr acquisition, signaling selective but improving investor confidence.

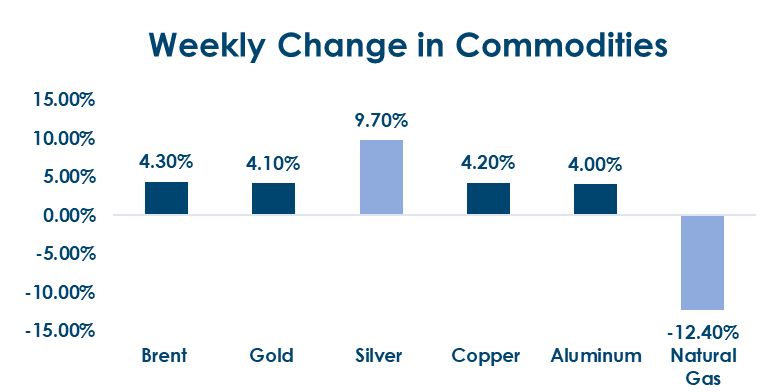

Commodities:

- Commodities rallied broadly this week, led by Silver (+9.7%) and Iron Ore (+5.8%), with Brent crude, base metals, and Gold up ~4%, while US Natural Gas was the only laggard (-12.4%).

- Precious Metals: Saw brief selling due to index rebalancing, but strong physical demand remains the key driver.

- Copper: Prices are firming up amid supply disruptions from Chile.

- Crude Oil: Supply concerns from Iran protests are outweighing expectations of Venezuelan oil returning to the market.

What’s New in the World of Wealth Management?

India’s capital and wealth management ecosystem is moving into a more institutionally mature phase, supported by regulatory depth and expanding market infrastructure. While household allocation to capital markets remains structurally under-penetrated relative to global peers, growth in mutual fund AUM, rising HNI participation, and a broadening private markets landscape continue to reshape domestic capital formation. This transition is creating stronger demand for sophisticated wealth solutions, alternative investments, and cross-border structures, positioning India for a deeper and more resilient financial ecosystem

A key catalyst in this evolution is the IFSCA-led reform agenda at GIFT IFSC, which is materially improving India’s competitiveness as a global financial hub. Recent reforms have simplified fund management norms, expanded eligible investment activities, eased compliance requirements for capital market intermediaries and strengthened the framework for Global In-House Centres (GICs). These measures are designed to attract global asset managers, private equity and hedge funds to domicile and manage capital from India, while also enabling domestic managers to scale offshore-facing strategies more efficiently. Collectively, the reforms lower friction in fund launches, improve talent access and enhance regulatory clarity — critical enablers for accelerating cross-border capital flows and advancing India’s ambition to become a regional wealth and asset management centre.

Our Views: What we Like?

Equities: Sentiment has been dampened by the possibility of the imposition of 500% tariffs by the US for procuring crude from Russia. We have ended the week at almost the lower end of the recent 25700-26400 trading range. We are exactly at the support zone. Our base case is for the range play to continue. Breakdown may occur if Trump actually goes ahead with 500% tariffs. We may see the market continue to look for direction ahead of the Union Budget. The domestic Q3 Earnings season will be in focus.

Fixed Income: Banking system liquidity turning neutral is putting pressure on CD-t-bill spreads. Buy-Sell swap will inject USD

90000crs into the system. We believe 6.60-6.70% range on 10y is attractive to add duration to the portfolio and to

execute a carry roll-down strategy

Commodities: We expect the rally in base metals to continue. Brent may face selling pressure around current levels given the

supply overhang and weak demand. Precious metals continue to remain buy on dips.

FX: Volatility in crosses has dropped sharply as majors i.e., EURUSD, GBPUSD, and USDJPY, are stuck in ranges. We expect the Dollar to trade with a neutral tone and expect the ranges to prevail.