Billionz Multi-Asset Weekly Newsletter

Earnings Drag Weighs on Equities as Precious Metals Maintain Momentum

Global Developments:

- Geopolitics continues to set the tone for markets overall. The possibility of the US intervening in Iran is keeping risk sentiment on edge.

- The Trump administration’s undermining of the authority of the Fed is seen as structurally bearish for the Dollar. Department of Justice’s criminal probe into Fed Chair Powell has raised concerns over Fed independence.

- The US core CPI came in a bit lower than expected this week.

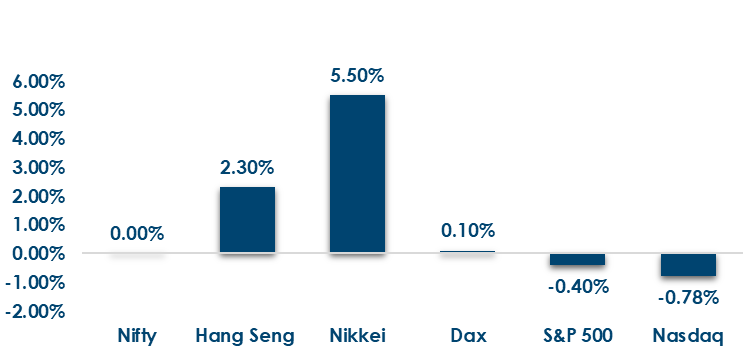

Global Equities:

This is how Global Equities performed this week.

Domestic Equities:

- Domestic equities continue to underperform. The Earnings season has not begun too well, with bottom-line pressures evident in Earnings reported so far.

- The Nifty50 range has shifted lower to 25500-25900 from 25700-26300. A break below 25450 could open room for another 3-4% downside.

- Budget, earnings, and news around the trade deal would be the major drivers for equities.

- Our base case is for range-bound trading to continue.

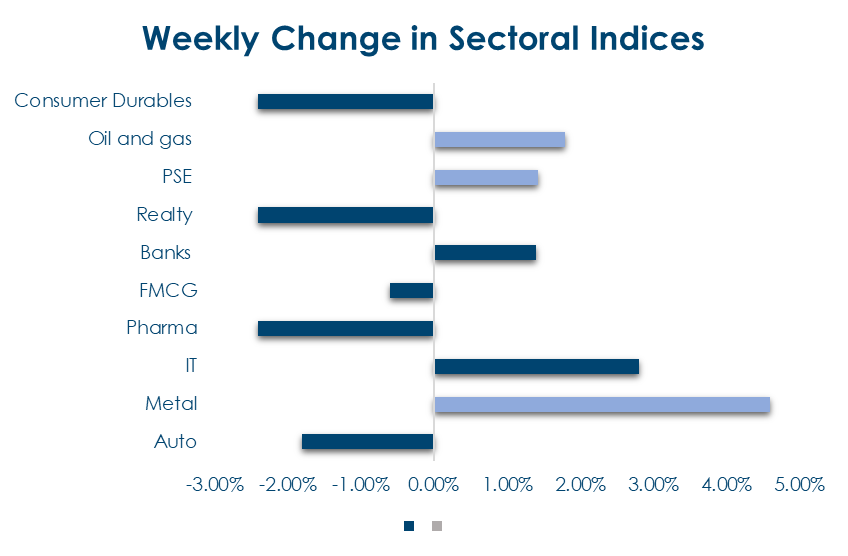

- We expect banks and IT to outperform, and Auto and Realty to underperform

- FIIs remained net sellers this week (₹14,265 cr outflow), while DIIs continued strong buying at ₹16,173 cr, broadly in line with the previous week.

- IFCI, Angel One, and Vedanta led the gains, while HBL Engineering, L&T Technology Services, and GE Vernova T&D India were the top laggards this week

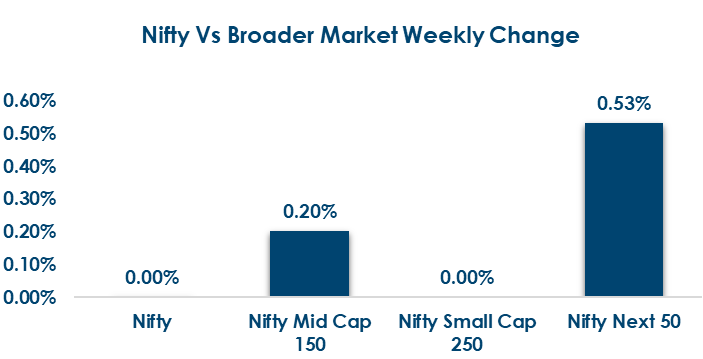

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income

- Global Rates: Global yields edged up, with US 2Y and 10Y yields rising 5 bps each, Eurozone 10Y yields largely flat (-2 to +2 bps) except Portugal (+12 bps), while Japan’s 10Y climbed 9 bps to 2.17%, its highest level since 1998.

- India Rates & Flows: Indian bond yields moved higher, with the 10Y benchmark up 4 bps to 6.68% (low of 6.57%) amid concerns over delayed Bloomberg index inclusion. Short-term rates also firmed—1Y and 5Y OIS rose to 5.54% and 6.02%, liquidity stayed in moderate surplus with overnight calls at 5.39–5.43%, FPIs invested USD 250 mn in bonds in January so far, 1Y T-bill stands at 5.61%, 1Y CD at 6.94%, and 10Y AAA PSU/NBFC spreads over G-sec are at 44 bps and 67 bps.

IPOs:

- Seven companies, including Gaudium IVF, Runwal Developers and Augmont Enterprises, have received SEBI approval to launch IPOs, signalling a strong pipeline for the coming year

- The primary market stays busy next week with the ₹1,907 crore Shadowfax IPO, three SME issues opening, and multiple listings, including Bharat Coking Coal and several SME debutants.

Real Estate:

- Nexus Select Trust plans to raise up to $250 million via debt to fund acquisitions, refinance borrowings, and enhance assets, with IFC committing through NCD subscriptions.

- Marubeni has invested ~₹250 crore in Kolte-Patil’s Pune residential project via long-tenor, zero-coupon NCDs, riding on strong housing demand from the Hinjawadi IT-driven ecosystem.

Private Equity & Venture Capital

- Deal activity picked up with higher transaction volumes, indicating broader participation, though overall investments eased and large-ticket deals remained absent, with capital concentrated in financial services and health-tech.

- Activity moderated during the week, marked by fewer and smaller transactions, with select mid-sized acquisitions in the education and hospitality segments.

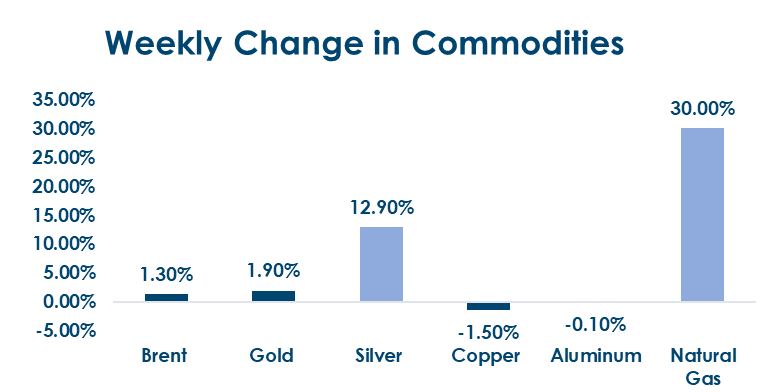

Commodities:

- Energy was mixed (Brent +1.3%, US gas -2.1%, Europe gas +30%), base metals softened, while precious metals outperformed with gold up 1.9% and silver surging 12.9%.

- While base metals cooled slightly, precious metals continued to rally. Gold and Silver hit fresh record highs.

What’s New in the World of Wealth Management?

India’s capital markets are undergoing a structural transformation, driven by the growing dominance of DIIs and sustained retail participation. Reforms by SEBI, the rapid expansion of the SIP ecosystem, and a gradual shift of household savings from physical assets and bank deposits to market-linked instruments have materially strengthened the depth and stability of domestic flows. This has reduced market dependence on foreign capital and enhanced India’s ability to absorb global volatility. Reflecting this maturity, India has emerged as the global leader in IPO volumes, underscoring both strong issuer confidence and a broadening investor base across sectors and market capitalisations.

On the regulatory front, SEBI continues to refine market structure to improve efficiency and align with global best practices. The regulator has introduced changes to the equity cash segment’s closing price discovery mechanism through a closing auction framework, aimed at enhancing transparency and reducing volatility. In parallel, SEBI has proposed a new trade settlement pathway to lower operational and funding costs for offshore funds, a move expected to improve ease of access for global investors while reinforcing India’s position as a well-regulated, scalable, and institutionally robust equity market.

Our Views: What we Like?

Equities: Domestic equities continue to underperform. The Earnings season has not begun too well, with the bottom-line

pressures evident in the earnings reported so far. The Nifty50 range has shifted lower to 25500-25900 from 25700-26300. A break below 25450 could open room for another 3-4% downside. Budget, earnings, and news around the trade deal would be the major drivers for equities. Our base case is for range-bound trading to continue. We expect banks and IT to outperform and Auto and Realty to underperform.

Fixed Income: Domestic bonds continue to remain under pressure despite OMOs. Indian Bonds not getting immediately included in the Bloomberg aggregate index was a dampener this week. However 6.60-6.70% zone has been a major resistance on the 10-year. We expect no major surprises in the upcoming budget, and that should ease nerves in the bond market. The focus, as always, will be on the gross borrowing number.

Commodities: We expect the rally in precious metals to continue as it is a structural theme. Base metals too are likely to see positive traction. We believe rally in Brent towards USD 65-66 per barrel can be sold into