Billionz Multi-Asset Weekly Newsletter

Pressure in Equities, Preference for Physical Assets

Global Developments:

- The week began with Trump announcing tariffs on European allies to coerce them into entering into an agreement on Greenland, but subsequently backtracked, saying he wouldn’t impose tariffs from Feb 1 (as he had threatened earlier).

- Incursion into Venezuela, aggressive stance on Greenland, intervention in Iran, concerns around Fed independence, lack of respect for established organizations like NATO, and COP are all factors that have triggered erosion of confidence in the dollar as a haven. It has accelerated the De-Dollarization process. This is most evident in previous metals, which just continue to soar. Gold neared the USD 5000 psychological mark while Silver breached the USD 100 mark!

- Japanese 10-year yield is the highest since Jun’97 at 2.26%. The 40-year yield had hit 4.23% and ended the week at 3.94%. One-sided Yen weakness and JGB selloff could trigger a systemic crisis (a VaR shock). The Fed is concerned about the same and conducted a rate check, which is typically seen intent to intervene.

- Domestic assets continued to underperform. The market is fixated on the trade deal. A depreciating Rupee is further fuelling anxiety among FPIs. Rupee, equities, and bonds are all under pressure.

- The RBI late Friday announced liquidity infusion of over Rs 2lakh crs through 91-day VRR (Rs 25000crs), Buy-Sell swap of USD 10bn (Rs 92000crs), and OMO purchase (Rs 1 lakh crs).

Global Equities

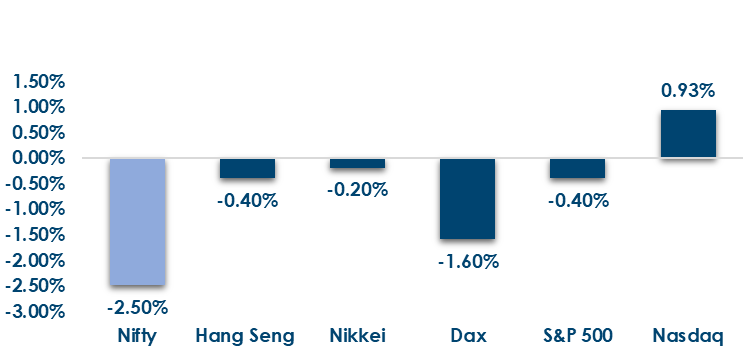

This is how Global Equities performed this week.

Domestic Equities:

- Global equities were mixed this week, with major indices mostly down (S&P 500 -0.4%, FTSE -0.9%, CAC -1.4%, DAX -1.6%, Nikkei -0.2%, Hang Seng -0.4%, Jakarta -1.4%) while Korea’s Kospi gained 3.1% and Singapore’s Straits Times rose 0.9%.

- Nifty50 trades at 20.7x trailing / 20.6x forward EPS, while Midcap100 sits at 33.3x / 28x and Smallcap250 at 28.2x / 25.3x.

- 16 out of 50 Nifty50 companies have reported Earnings so far, and while top-line growth has been around 4.5%, earnings growth has been -8.6%

- In terms of factors, dividends and market cap outperformed, while growth underperformed

- FPIs have sold net USD 3.7bn of domestic equities in January so far.

- FIIs recorded outflows of ₹14,651.99 Cr this week vs ₹14,265 Cr last week, while DIIs remained strong with inflows of ₹20,746 Cr vs ₹16,173 Cr in the previous week.

- Top gainers were Jindal Saw (+14.9%), Hindustan Zinc (+9.6%), and CreditAccess Grameen (+7.2%), while top losers were Kalyan Jewellers (-21.5%), Godrej Properties (-18.4%), and OneSource Speciality Pharma (-18.4%).

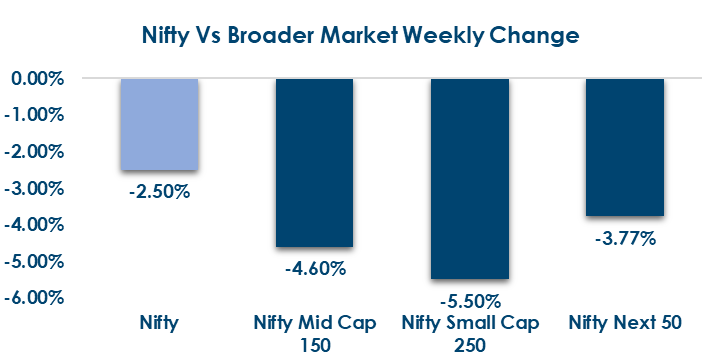

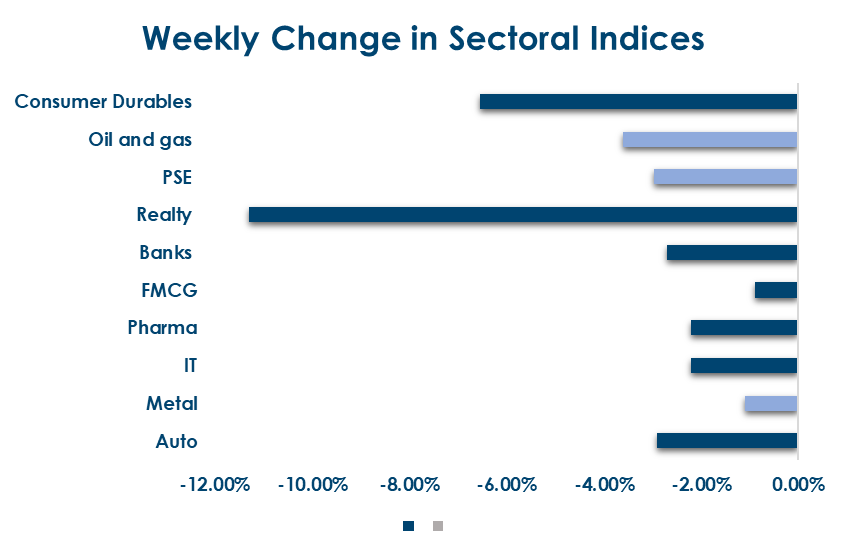

Below are the graphical representations of how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: US 2Y yield ended 1bp lower at 3.59%, and 10Y closed near 4.22% after rising to 4.29% during the week; Eurozone 10Y yields were mostly up 5–10bps (France flat, Greece +17bps) while 10Y JGB ended 1bp lower at 2.24% after spiking to 2.34%.

- India Rates & Flows: The 10Y benchmark traded in a 6.63–6.695% range and closed at 6.66%, while the OIS curve steepened with 1Y at 5.60% (+6bps) and 5Y at 6.14% (+12bps); FPIs have net bought USD 700mn of domestic bonds in January so far.

Real Estate:

- Japanese conglomerate Marubeni has teamed up with Mt. K Kapital as co-general partner in its $450 million India-focused AIF, signalling a move from balance-sheet investments to active fund-based investing and growing global interest in India’s private markets.

- Blackstone-backed ASK Asset & Wealth Management’s property fund invested ₹210 crore in two Gami Group residential projects in Navi Mumbai, showing rising confidence in micro-markets like CBD Belapur and Ghansoli, supported by the upcoming Navi Mumbai International Airport and better connectivity via Atal Setu.

IPOs:

- With no mainboard IPOs scheduled for Jan 26–30, attention stays on the SME segment. Five to six SME IPOs open for subscription this week, while recent issues like Shadowfax Technologies, KRM Ayurveda, and Digilogic Systems prepare to list, keeping activity steady.

- SEBI has cleared 13 companies across sectors, including hospitality, logistics, electronics, and data infrastructure (such as Pride Hotels), indicating issuers are ready to launch once valuations and market conditions improve, suggesting a selective resumption of mainboard IPOs.

Private Equity & Venture Capital:

- PE & VC activity marked a third consecutive robust week with 44 deals (vs 32 WoW), while total deal value more than doubled to $779 million. M&A activity remained steady with seven transactions, in line with recent trends

- Large transactions were dominated by PE capital, led by General Atlantic’s ~$272 million investment in Balaji Wafers. On the M&A front, Inspira Global acquired Everstone’s 11.26% stake in Restaurant Brands Asia for ~$57 million, reflecting sustained strategic interest in consumer-focused assets.

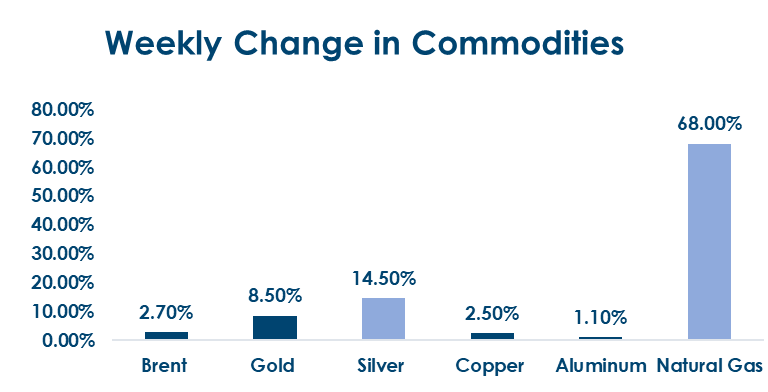

Commodities:

- Commodities rallied this week: Brent +2.7%, Natural Gas +68%, Aluminum +1.1%, Copper +2.4%, Gold +8.5%, Silver +14.5%.

- Precious metals continued to zoom on concerns over the Dollar. There is a definite urge to move towards a physical store of value from fiat currencies, given the current geopolitical uncertainties.

- US Natural Gas surged on a massive Arctic cold wave, which resulted in a sharp surge in demand for heating.

What’s New in the World of Wealth Management?

India’s capital markets are undergoing targeted regulatory and structural recalibration aimed at improving depth, access, and transparency. SEBI is considering easing fit-and-proper norms for brokers and intermediaries, which could expand participation and enhance market efficiency, while simultaneously moving to formalise the regulation of the unlisted share market to strengthen investor protection and governance in pre-IPO trades. On the investment side, market leadership is increasingly shifting toward capex-led sectors, reflecting confidence in India’s medium-term growth cycle driven by infrastructure, manufacturing, and industrial investment.

Alongside these market-level changes, policy and sentiment tailwinds remain supportive. A potential recalibration of the tax regime is expected to improve post-tax returns and attract a higher share of global capital, while global CEOs continue to rank India among the most attractive investment destinations, despite a challenging global backdrop. Together, these developments reinforce the view that India’s capital markets are becoming more institutional, growth-aligned, and globally relevant, supporting long-term wealth creation and capital formation.

Our Views: What we Like?

Equities: We see domestic equities continuing to remain under pressure. While the benchmark index is off about 5% from all-time highs, there is significantly more pain in midcaps, smallcaps, and microcaps. The budget may do little to change sentiment. Trade deal is a bigger factor. 24650 is likely to be a technical support for the Nifty50. We prefer to stick to value, quality, and large cap space. Among sectoral indices, we are overweight on IT.

Fixed Income: We expect the yield on the 10y to trade in a 6.60-6.70% range till the budget. There is a possibility that the government may choose to defer fiscal consolidation given the current domestic macro challenges. There would be panic in bond markets if this were to happen. A high nominal GDP growth expectation used for budgeting purposes may not go down well with markets, too, as it would be seen as being unrealistic (anything over 10%).

Commodities: Rally in precious metals is likely to continue, and any dip of 8-10% should be seen as a buying opportunity. There is a definite trend of preference to hold physical assets over fiat currencies, and we see this playing out over a protracted period of time.

FX: We continue to remain bearish on the Dollar overall and expect the Rupee to continue to underperform