Billionz Multi-Asset Weekly Newsletter

Nifty in a Range as IT Falters; Precious Metals Remain Favoured

Global Developments:

- US Inflation Update: January headline CPI came in below expectations, indicating easing inflationary pressures.

- Fed Rate Expectations: The OIS market is now pricing in ~2.5 rate cuts by the Federal Reserve by the end of 2026.

- US Labor Market: The January jobs report, released earlier this week, remained solid, highlighting continued resilience in employment data.

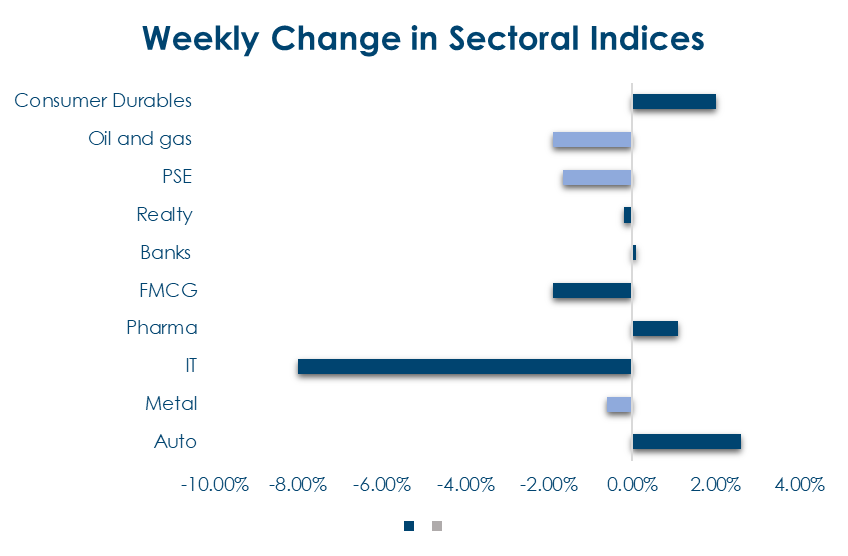

- Domestic IT Stocks: A sharp sell-off was witnessed amid AI disruption concerns. The IT index declined by over 8% during the week.

- Japan Markets: Japanese equities outperformed after PM Takaichi’s landslide victory in the general elections, reducing political uncertainty and boosting expectations of fiscal stimulus.

- Korea Markets: Korean stocks outperformed, driven by optimism in the semiconductor (chip) sector.

Global Equity Markets:

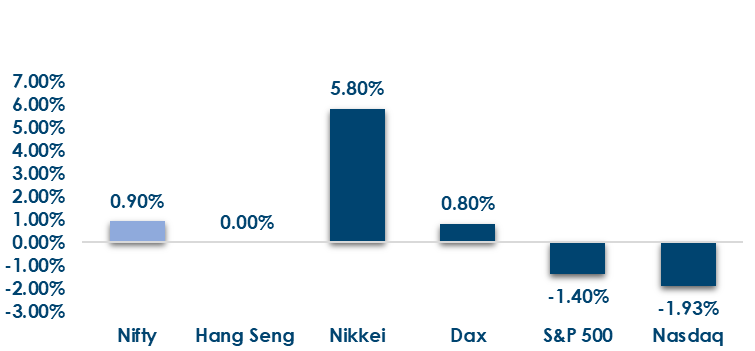

This is how global equities performed over the last week:

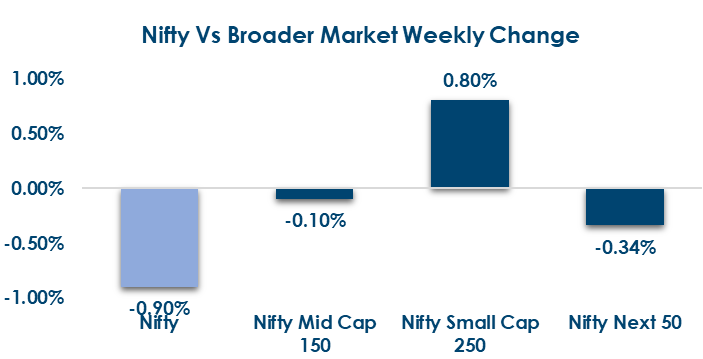

Domestic Equities:

- Major indices showed mixed performance this week, with strong gains in Kospi (+8.2%), Nikkei (+5.8%), and Jakarta (+3.5%), modest upticks in DAX (+0.8%), FTSE (+0.7%) and CAC (+0.5%), flat Hang Seng (0%), while S&P 500 declined (-1.4%).

- Nifty50 at 21.2x / 20.2x, Midcap100 at 34x / 28.2x, and Smallcap250 at 29.3x / 26.8x, indicating relatively richer valuations in the broader markets.

- In terms of factors/styles, momentum and low volatility outperformed, while market cap, quality, and value underperformed.

- The aggregate sales surprise for Nifty50 companies for Q3 was 5%, and Earnings surprise was 0%

- FPIs have invested net USD 2.1bn in domestic equities in February so far.

- FIIs turned net sellers at ₹4,019 Cr this week (vs. ₹2,057 Cr inflow last week), while DIIs remained net buyers at ₹6,884 Cr (vs. ₹2,210 Cr last week).

- Shipping Corporation (+19.2%), Kirloskar Oil Engines (+17.9%), and Engineers India (+17.7%) led gains, while Reliance Infrastructure (-13.3%), Firstsource Solutions (-12.5%), and eClerx Services (-12.4%) were top laggards.

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: 10Y yields softened across major economies—US (-15 bps), UK (-11 bps), France (-10 bps), Germany (-9 bps), India (-8 bps), Japan (-6 bps), and China (-2 bps)— reflecting a broad-based decline in global bond yields.

- India Rates & Flows: The domestic 10Y yield eased 8 bps to 6.68% amid abundant liquidity (overnight MIBOR ~5.08–5.09%; TREPS below 5%), with 1Y/5Y OIS down 3 bps/11 bps to 5.50%/6.07%; 3M T-bill at 5.27% vs 3M CD at 6.94%, 10Y AAA PSU/NBFC spreads at ~60/70 bps, while FPIs infused USD 1.1 bn into debt in February so far.

Real Estate:

- Budget 2026–27 continues its infra-led growth strategy with higher capex on railways, highways, logistics, and urban clusters—improving connectivity, reducing costs, and structurally supporting real estate demand across residential, commercial, warehousing, and Tier-2/3 markets.

- Despite growth tailwinds, weak RERA compliance —over 75% of state authorities not publishing mandatory annual reports (as per FPCE)—raises transparency concerns, underscoring the need for stronger governance to sustain buyer confidence.

IPOs:

- Fractal Analytics (~₹2,840 Cr) and Aye Finance (~₹1,010 Cr) are set to list on Feb 16, offering exposure to AI/analytics and NBFC segments, signaling renewed IPO momentum.

- Gaudium IVF & Women’s Health opens its IPO on Feb 20 (listing on Feb 27), reflecting an expanding capital-raising activity across the technology, financial services, and healthcare sectors.

Private Equity & Venture Capital:

- Deal activity rose for the second straight week with 36 fundraises (vs. 24 prior), and total capital crossing $612 mn, led by private equity investments across housing finance, renewables, and digital services.

- Consumer health saw marquee deals, including USV’s $175 mn acquisition of Wellbeing Nutrition, and Hindustan Unilever is increasing its stake in OZiva, highlighting strong consolidation in the segment.

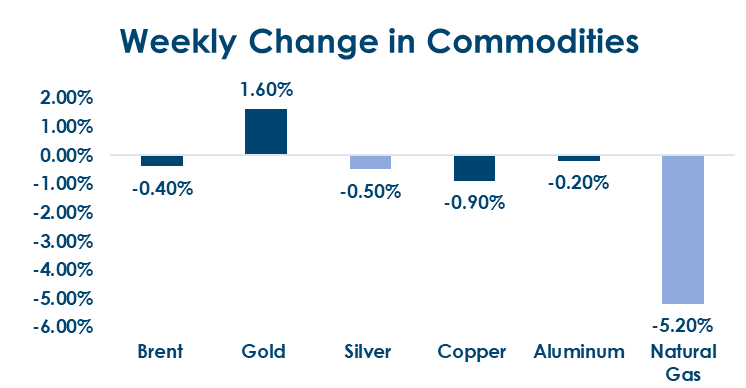

Commodities:

- Energy prices declined (Brent -0.4%, US Gas -5.2%, EU Gas -9%), base metals stayed subdued (Aluminum -0.2%, Copper -0.9%), while precious metals were mixed with Gold up 1.6% and Silver down 0.5%.

- Brent eased on optimism around US-Iran nuclear talks, and Natural Gas came off on warmer weather in the US and Europe, dampening heating-related demand outlook.

What’s New in the World of Wealth Management?

Indian capital markets continue to demonstrate structural resilience despite an uncertain global backdrop. As highlighted by SEBI, domestic participation, improving market infrastructure, and regulatory strengthening have enabled equities to absorb geopolitical volatility, AI-led disruptions, and global trade realignments without systemic stress. From our vantage point, while the long-term growth narrative remains intact, the recent phase of outperformance suggests that markets may undergo a period of near-term consolidation as valuations recalibrate and earnings dispersion plays out.

On the macro front, trade developments remain constructive. Ongoing FTA discussions with New Zealand and progress toward a broader trade framework with the United States signal medium-term tailwinds for exports, manufacturing and capital flows. However, we believe these structural positives are likely to reflect in price action gradually rather than immediately. In the near term, Indian equities may continue to move within a defined range before a decisive breakout, supported by earnings stability, policy continuity, and improving external trade visibility.

Our Views: What we Like?

Equities: Domestic Equities are underperforming global equities. Underperformance of the IT index this week is concerning. Q3 Earnings overall have been mixed, with industrial and manufacturing sectors doing well and IT earnings disappointing. Large-cap IT underperformance on AI disruption fears put pressure on the benchmark Nifty50 index this week. Technically, 24900 to 25900 is the range we seem to be in for now. We can continue to see consolidation in this range. Banks and Auto should continue to support the index.

Fixed Income: Government switched 2027 maturities to 2040 and then alleviated some pressure on Bonds, causing

yields to retrace. We expect the 10-year benchmark to trade in a 6.60-6.80% range over the next few weeks.

Commodities: We continue to believe that precious metals are a buy on dips. Gold around 4400-4500 is an attractive buy, and so is silver around USD 65-70 per troy ounce. We may see some headwinds for industrial/base metals in the times ahead.

FX: RBI seems to be protecting 90.80. With the flow picture having improved, we expect the Rupee to be range-bound and expect the RBI to be present on both sides.