Billionz Multi-Asset Weekly Newsletter

Markets Consolidate, Geopolitics Power Commodity Outlook

Global Developments:

- The US Supreme Court struck down Trump’s sweeping global tariffs (imposed by invoking the International Emergency Economic Powers Act) on Friday in a 6-3 decision. Reciprocal tariffs and Fentanyl related tariffs will not hold.

- In response, Trump announced a 10% levy on all foreign goods effective 24th Feb. Trump said he would order a raft of trade investigations that should allow him to enact more permanent tariffs.

- Trump said that nothing has changed in the trade deal with India. \

- There is an ebb and flow of US-Iran tensions, and that is keeping markets, particularly Crude on edge.

- US PCE print was hotter than expected, and PMIs and Consumer sentiment were weaker than expected. Market is pricing slightly over 2, 25bps cut by the Fed till the end of 2026.

Global Equity Markets:

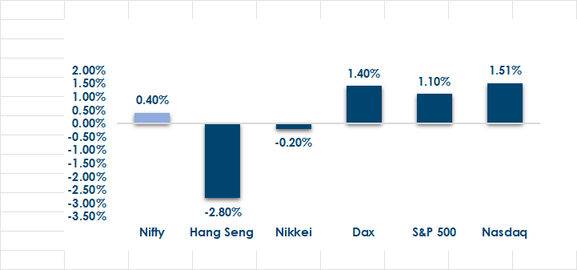

- Global markets rose in developed regions, with US and European indices advancing S&P 500 +1.1%, FTSE 100 +2.3%, CAC 40 +2.4%, DAX +1.4

- Asia was mixed, with KOSPI +9.6% and Taiwan +4%, while Nikkei 225 -0.2%, Hang Seng Index -2.8%, and Jakarta -0.2% declined

- Singapore’s Straits Times Index +0.7% rounded out mixed regional performance

Domestic Equities:

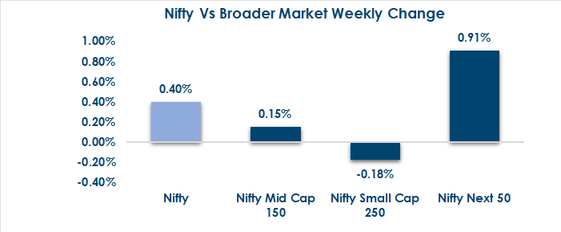

- Domestic equities were largely flat this week, with Nifty 50 +0.4%, Nifty Midcap 100 +0.1%, and Nifty Smallcap 250 -0.2%, reflecting muted investor activity across segments.

- Domestic equity valuations remain elevated, with Nifty 50 trading at 21.2x trailing and 20x forward EPS, Nifty Midcap 100 at 34.4x trailing and 28.1x forward, and Nifty Smallcap 250 at 29.3x trailing and 27.1x forward, reflecting relatively rich pricing across market segments.

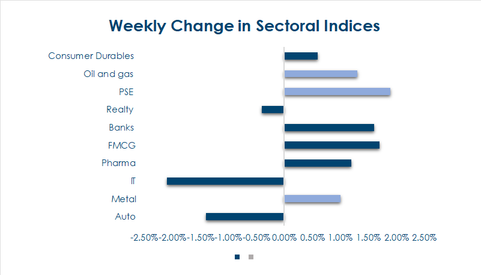

- Sectoral performance was mixed this week, with Bank Nifty +1.6%, FMCG Index +1.7%, Energy Index +2.4%, and Pharma Index +1.2% leading gains.

- Underperformers included IT Index -2.1%, Auto Index -1.4%, and Realty Index -0.4%, reflecting sector-specific headwinds.

- FPIs have invested net USD 1.9bn in domestic equities in February so far.

- In terms of factors, value and low volatility outperformed this week, while momentum and growth underperformed.

Below are the graphical representations of how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: Global sovereign yields were mixed this week, with US 10-year +3bps, UK -5bps, France -5bps, Germany -2bps, Japan -9bps, and China largely unchanged at +0.4bps.

- India Rates & Flows: Domestic bonds saw modest pressure, with the 10- year yield rising to 6.72% from 6.68% and 1- and 5-year OIS up 2bps each to 5.52% and 6.09%. Overnight liquidity remained ample, keeping MIBOR around 5.13– 5.14% and TREPS at 4.80–4.90%. Credit spreads were steady, with 10-year AAA PSU at 54bps and AAA NBFC at 78bps, while FPIs invested a net USD 1.6bn in domestic debt so far in February.

Real Estate:

- Lighthouse Canton expands India focus: Lighthouse Canton is evaluating new real estate investments in Mumbai and Bengaluru, deepening its India office and life sciences presence.

- Platform-led institutional backing: Its India’s strategy includes a Genome Valley asset acquired from Alexandria Real Estate Equities and supported by Ivanhoé Cambridge (under La Caisse).

- Office market financing improves: Embassy Office Parks REIT raised ₹1,400–1,550 crore in debt, reflecting stronger capital access and balance sheet optimisation in India’s office REIT segment.

IPOs:

- India’s primary market will see multiple mainboard IPOs during Feb 23–27, led by the ₹3,100 crore issue of Clean Max Enviro Energy Solutions, reflecting sustained capital-raising momentum.

- PNGS Reva Diamond Jewellery (₹380 crore fresh issue) plans retail expansion, while Shree Ram Twistex aims to fund capacity and efficiency enhancements, highlighting sector-wide growth investments.

- SME IPO launches and listings remain active, signalling healthy liquidity conditions and continued investor participation in equity capital markets.

Private Equity & Venture Capital:

- Funding jumps to $931M: 31 companies raised ~$931M in the week ended Feb 20, up sharply from $612M the previous week, despite similar deal volumes.

- AI drives inflows: Blackstone led a $600M round in Neysa, contributing nearly two-thirds of total PE/VC investments.

- Power M&A gains pace: Torrent Power agreed to acquire Nabha Power for $403M, while Inox Group acquired Wind World’s IPP portfolio.

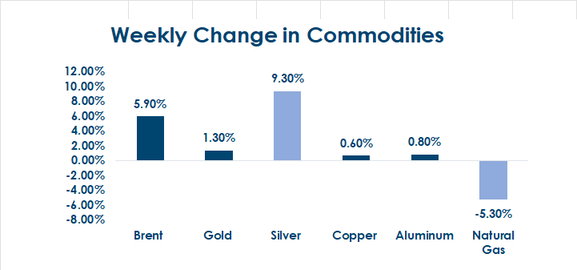

Commodities: Energy markets were mixed this week, with

Brent crude rising 5.9% to $71.8, while the US and European natural gas declined 5.3% and 1.5%, respectively, reflecting volatility across the global fuel benchmarks. Precious metals outperformed, with gold up 1.3% and silver surging 9.3%, while base metals saw modest gains (aluminium +0.8%, copper +0.6%) and iron ore corrected 4.2%. Risk of escalation in US-Iran tensions is pushing Brent higher.

What’s New in the World of Wealth Management?

Domestic brokerages have sought a six-month freeze on proposed RBI regulatory changes, citing operational challenges and the risk of disruption to client servicing and compliance processes. If implemented without an adequate transition window, tighter norms could increase costs, strain smaller intermediaries, and accelerate consolidation within the broking industry, ultimately favouring larger, well-capitalised players with stronger compliance infrastructure.

On the funding front, the RBI’s revamped External Commercial Borrowing (ECB) framework is expected to improve access to overseas capital for the real estate and infrastructure sectors. Greater flexibility and potentially lower borrowing costs could diversify funding sources and support project execution in capital-intensive segments. This is structurally positive for developers, infrastructure operators and REIT platforms, aiding balance sheet optimisation and supporting long-term asset creation.

Our Views: What we Like?

Equities: Domestic equities continue to consolidate. We have seen FPI flows return in February, which is a good sign. However, Nifty50 continues to remain range-bound in 24600-26400. It is quite a broad range, but there are ranges within. 25100 is now a crucial gap support, which could be tested if 25350 gives way, a level which held well this week. IT sector continues to remain a drag. 31300 is an extremely crucial level, which is about 2% lower than the current levels

Fixed Income: Despite ample liquidity in the banking system, supply pressures remain to the fore, making any rally in domestic Bonds short-lived. We expect the 10-year yield to trade in a 6.60-6.80% band over the next few weeks. 5y OIS has cooled off and should see support around 5.90-5.95% now.

Commodities: US-Iran tensions will likely continue to support Brent. Previous metals remain a buy on dips in our view, given the structural changes in global trade relationships and geopolitical dynamics. There is also a massive FOMO factor. Gold around USD 4600-4800 and Silver around USD 65-70 should see good support.

FX: The Dollar index has been consolidating in the 96-100 range since the middle of 2025. We expect this trend to continue.