Billionz Multi-Asset Weekly Newsletter

AI Fears Weigh on Nifty; Metals Remain the Bright Spot

Global Developments:

- Rising geopolitical tensions have triggered a flight to safety. US treasuries and precious metals have been bid up on safe-haven demand. President Trump said that he is not happy with how the negotiations with Iran are progressing and that he may have to use force. Countries have been asking citizens to leave Iran. The UK closed its Iranian embassy and withdrew staff from Tehran amid fears of imminent US strikes.

- Another key theme playing out is concerns around credit given to AI-led disruptions. There are chances that traditional businesses will default due to AI-led disruptions.

Global Equity Markets:

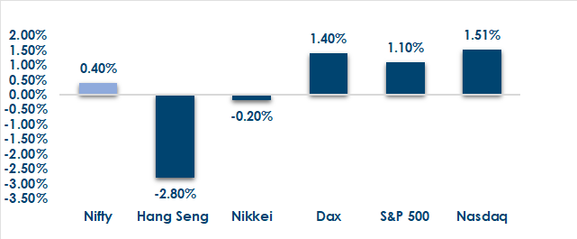

Global equities were mixed this week, with strong gains in Asia led by Kospi 7.5%, Taiwan 7.1%, and Nikkei 2.4%, while Europe was positive with FTSE up 2.1% and CAC 0.8%; the S&P 500 declined 0.4%, and Jakarta and Straits slipped 0.4% and 0.5% respectively.

Domestic Equities:

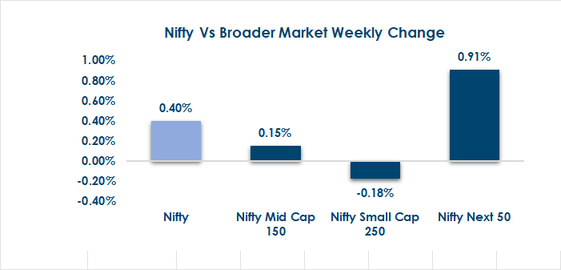

- In domestic equities this week, markets declined with Nifty50 down 1.5%, while Midcap100 and Smallcap250 fell 0.7% and 0.5% respectively.

- Valuations remain elevated in broader markets, with Nifty50 trading at 21x trailing and 20x forward earnings, while Midcap100 stands at 34x and 28x, and Smallcap250 at 29.2x and 26.2x, respectively.

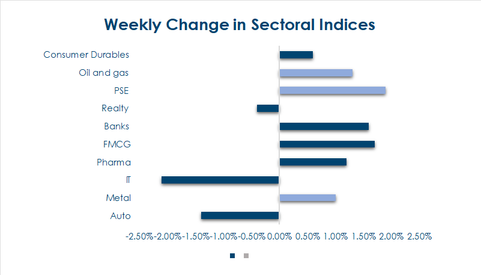

- Sectoral performance was mixed, with Metals and Oil & Gas up 2.1%, Pharma 2.2%, Energy 1.3% and Auto 1.1%, while Realty declined 4.9%, IT fell 4.3%, FMCG dropped 1.2% and Bank Nifty was down 1.1%, with Consumer Durables flat.

- In terms of factors, momentum, dividend, and value outperformed, while growth and liquidity underperformed

- FPIs have invested net USD 2.5bn in domestic equities in February

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: US Treasury yields declined, with the 2y down 6bps to 3.38% and the 10y lower by 9bps at 3.94%, while global 10y yields also softened across regions, led by South Korea 14bps, the US 9bps, and the UK 8bps, with Japan unchanged.

- India Rates & Flows: Domestic bond yields eased, with the 10y benchmark ending at 6.66% versus 6.72% last week, while 1y and 5y OIS fell to 5.48% and 5.99% respectively; money market rates remained stable with MIBOR at 5.13–5.17%, 1y T-bill at 5.51%, and 1y. CD at 6.91%, alongside net FPI debt inflows of USD 1.6bn in February. February.

Real Estate:

Nexus Select Trust, sponsored by Blackstone, has acquired a 50% stake in the under-construction Nexus Runwal Gardens Mall in Dombivli for Rs 434 crore, marking its first investment in a development asset and expanding its retail REIT platform to 19 assets. Separately, GIC is evaluating exit options from a long-held India real estate investment, continuing its strategy of monetising legacy exposures, including prior stake sales in ventures with DLF and the Runwal Group.

IPOs:

India’s primary market activity remains selective, with one mainboard IPO from Sedemac Mechatronics and one SME issue from Elfin Agro India opening this week, while fresh capital raising stays modest. However, nine companies are slated to list, supporting investor engagement. In a key development, the National Stock Exchange of India has invited bankers to pitch for its proposed IPO, which could raise around USD 2.5 billion based on current unlisted valuations

Private Equity & Venture Capital:

PE and VC deal activity rose to 40 transactions from 31 last week, but total deal value dropped 73% to about USD 243 million due to the absence of large ticket deals, with none exceeding USD 50 million. A key disclosed transaction saw General

Catalyst led a USD 20 million round in defence tech startup Constelli. M&A activity also improved to six deals from two, led by BillDesk’s USD 70 million acquisition of Worldline’s India payments business, signalling renewed consolidation in the sector.

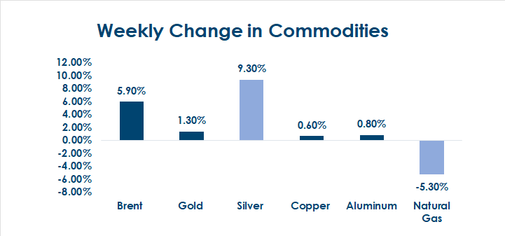

Commodities:

Precious metals led gains this week, with Silver surging 10.8% to USD 93.8 and Gold rising 3.4% to USD 5,278 on strong momentum and safe haven demand.

Base metals remained firm as LME Copper advanced 2.9% to USD 13,343 and LME Aluminum gained 1.2% to USD 3,140, reflecting resilient industrial sentiment.

Energy markets were mixed, with Brent crude up 1% to USD 72.9.

Natural gas underperformed as US natural gas fell 6% to USD 2.86 while European natural gas was largely flat at EUR 32.

What’s New in the World of Wealth Management?

India’s mutual fund landscape is undergoing a major regulatory reset as SEBI overhauls its scheme categorization framework to enhance transparency and investor clarity. The revamp introduces life-cycle funds with glide-path asset allocation, scraps the solution-oriented category (including retirement and children’s funds), and tightens portfolio overlap norms to curb duplication across sectoral and thematic funds. The changes also broaden how equity and hybrid schemes may deploy residual allocations — now permitting exposure to gold, silver and other assets — alongside mandatory monthly disclosures to ensure schemes are “true to label.”

In a parallel development, the NSE International Exchange has launched its Global Access platform from GIFT City, enabling Indian retail and NRI investors to directly invest in US-listed stocks like Apple and Microsoft, with plans to expand access to 30 global markets, including Europe, Japan and Australia over the coming months. The platform, compliant with RBI’s Liberalized Remittance Scheme (LRS), offers digital onboarding, fractional investing and low-cost access to overseas equities and ETFs without requiring a traditional demat account — marking a significant expansion of outbound investment channels for Indian investors.

Our Views: What we Like?

Equities: The IT Index is keeping the Nifty50 under pressure. It has dropped about 26% this month itself. The threat of AI

disrupting the business models of IT companies is unnerving investors. Korea and Taiwan are seen as AI beneficiaries, while India is seen as an anti-AI trade. After Friday’s sell-off, we have closed below the crucial 25400 support, and this brings 24600 in play again. We prefer sticking to quality and being overweight metals and underweight IT

Fixed Income: Yield on the benchmark 10y is likely to trade in the 6.60-6.80% range. Higher CD ratios have meant that demand for Gsec from banks has been lower than it otherwise would have been. However, we may see demand come in as LCR ratios drop.

Commodities: Brent is on the edge given US-Iran tensions. Metals overall continue to do well, especially precious metals. We prefer buying precious metals on any dip. Gold at USD 4600 and Silver at USD 75 could offer good entry points

FX: Vols continue to remain very low overall. We are slightly biased towards USD weakness on account of structural Reserve shifts (De-Dollarization theme).