Billionz Multi-Asset Weekly Newsletter

Sideways Markets, Strategic Minds: Asia’s Wealth Hubs Lead a New Investment Era.

US Developments:

- President Trump announced plans to impose an additional 100% tariff on China and

- to implement export controls on all critical software, effective November 1st.

- He stated that these measures would be withdrawn if China lifts restrictions on rare

- earth exports.

- The Trump administration began laying off Federal workers on Friday.

- Trump mentioned that a large number of Federal employees would be laid off and

- would not return even after the shutdown ends.

- The US government shutdown has now lasted 10 days, with no signs of agreement

- between Republicans and Democrats.

- These developments triggered a risk-off sentiment, leading to:

- Sell-off in US equities

- Drop in US Treasury yields

- The dollar is giving up earlier gains.

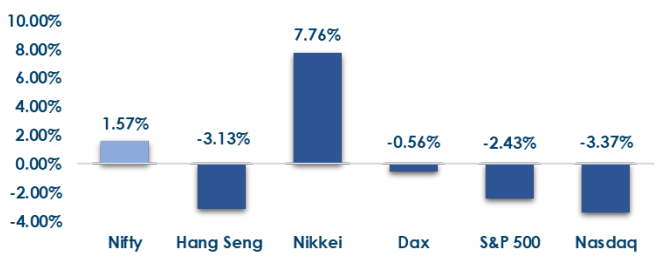

Global Equities

This is how Global Equities performed this week.

Domestic Equities

- PE Valuations (Trailing vs Forward Rolling 12M): Nifty50: 22.4 vs 21.8 | Midcap100: 32.9 vs 28.9 | Smallcap250: 29 vs

- 27.5 – Large caps are moderately valued, while mid and small caps trade at higher multiples with forward earnings

- indicating slight moderation.

- FPIs have sold a net USD 200 million from Domestic Equities in October so far.

- FII inflows turned positive this week at ₹2,975 crore after significant outflows of ₹8,347 crore last week.

- DII activity stayed strong with ₹8,391 crore inflows this week and ₹13,013 crore in the previous week.

- Top gainers in the market were Tata Communications (15.9%), PG Electroplast (14%), and BSE Ltd (13.9%).

- Top losers included Ola Electric (-8.2%), Aegis Logistics Ltd (-7.8%), and UNO Minda Ltd. (-7.3%).

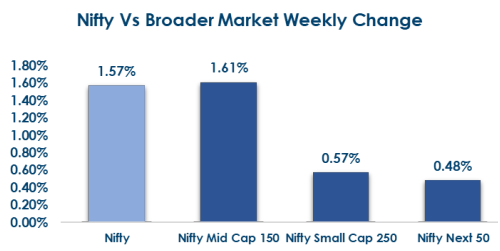

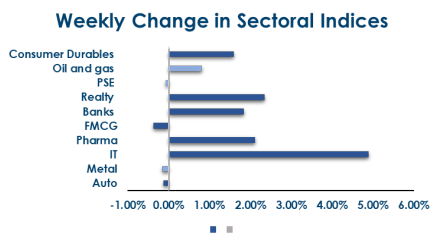

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices performed this week:

Fixed Income:

- US 2Y yields fell 9bps to 3.50%, and 10Y yields dropped 12bps to 4.03%. UK and Eurozone 10Y yields were down 6–8bps.

- Domestically, the 10Y G-sec ended at 6.54%, the week’s high, while the low was 6.49%. 1Y and 5Y OIS remained steady at 5.44% and 5.66%. FPIs have invested a net USD 500mn in equities this month.

- Short-term rates:

- 3M/6M/12M T-bills at 5.43%/5.51%/5.54%;

- 3M/6M/12M CDs at 5.93%/6.07%/6.33%.

- Credit benchmarks: 10Y AAA PSU at 7.12%, 10Y AAA NBFC at 7.34%.

Real Estate:

Private equity inflows into India’s real estate fell 15% YoY to $2.2B in H1 2025, impacted by higher interest rates and softer global sentiment. Domestic investors and AIFs remained active, especially in residential and logistics projects.

Sundaram Alternates closed its second real estate credit fund, SARE Credit Fund I, at ₹435 crore, delivering a 17% gross IRR, highlighting the rising role of private credit in funding developers amid slowing equity flows.

IPOs:

India’s IPO market remains active, with a brief pause next week. Attention turns to high-profile listings: Tata Capital (₹15,511 crore, Oct 6–8, price band ₹310–₹326) and LG Electronics India (₹11,607 crore, listing on Oct 14), both of which are attracting strong investor interest.

The broader IPO outlook stays positive, with India potentially raising $20 billion over the next 12 months, supported by strong domestic demand, NBFC listings, and sustained corporate confidence.

Private Equity & Venture Capital:

The market rebounded sharply after a brief slowdown, with deal value up ~30% to ~$700M across 38 transactions (vs. 23 last week), signaling renewed investor confidence. Three deals topped $100M, contributing over half the total value.

Key highlight: Prosus acquired a 10.1% stake in Ixigo via MIH Investments, reflecting strong global interest in India’s digital economy.

Deals in the renewable sector remained subdued, with just 2 transactions (vs. 9 previously). Notable deal: ReNew Energy sold a 300 MW solar project in Rajasthan to Sembcorp for $191M ahead of its domestic listing.

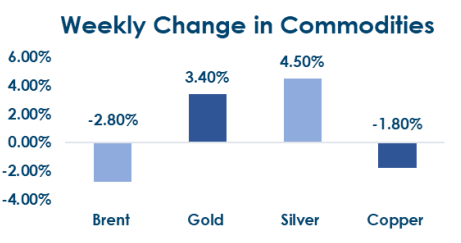

Commodities:

This week, energy prices saw declines with Brent crude down 2.8% and US natural gas falling 6.6%, while metals had mixed movements—aluminum rose 1.4% and copper slipped 1.8%. Precious metals outperformed, with gold gaining 3.4% and silver up 4.5%. Gold and Silver rallied this week, both taking out key psychological levels of USD 4000 and USD 50, respectively. Silver borrowing cost surged to unprecedented levels, sending the curve into backwardation. It indicates massive spot demand for delivery.

What’s New in the World of Wealth Management?

Wealth management in Asia is witnessing a major transformation, with Hong Kong and Singapore emerging as the twin pillars of a rapidly expanding family office ecosystem. Both cities are attracting ultra-high-net-worth families drawn by favourable tax regimes, regulatory clarity, and robust financial infrastructure. The ongoing intergenerational wealth transfer across Asia is driving the professionalisation of family offices, as families increasingly seek structured governance, succession planning, and risk management. Instead of competing, Hong Kong and Singapore are evolving as complementary hubs — with many families establishing a presence in both to balance geographical, regulatory, and geopolitical advantages.

The focus of family offices is also shifting from mere wealth preservation to building resilient, purpose-driven structures. There is growing emphasis on sustainable investing, diversification beyond traditional asset classes, and global portfolio exposure through private credit and alternatives. Families are prioritising governance, transparency, and cross-border tax efficiency, while adopting digital tools for reporting and analytics. Overall, Asia’s wealth landscape is entering a more mature phase — one defined by sophistication, sustainability, and strategic foresight.

Our Views: What we Like?

Equities:

Nifty50 has been range-bound in 24300-25600 for the last 5 months. We may continue to see a protected period of sideways price action and believe it is time for active sector allocation and stock selection rather than passive bets. We believe there is value in banks and IT. We see the RBI’s latest policy as a dovish hold, and banks are likely to do well in a low-interest-rate environment. A lot of negativity in terms of the US slowdown and protectionism seems to be in the price for IT stocks.

Fixed Income:

We expect the 10y to trade in a 6.45-6.65% range over the next few weeks. We believe any uptick on 10y towards 6.65% is a good opportunity to add duration to the portfolio. Current levels on 5y OIS are attractive to convert floating-rate liabilities to fixed.

Commodities:

We continue to remain bullish on precious metals amid uncertainties around trade and the US government shutdown. Overall, Dollar weakness imparts a tailwind as well. We are more upbeat on Silver than on Gold. We are neutral on Brent and Base Metals at this point.

FX:

We continue to believe, despite this week’s Dollar strength, that we are still in a phase of overall Dollar weakness, especially in the case of G10. We expect Dollar weakness to be less pronounced against Emerging market currencies, especially the Rupee.