Billionz Multi-Asset Weekly Newsletter

Geopolitics Roils Global Assets

Global Developments:

- Energy prices surged this week as the escalating US–Iran conflict spread across multiple Middle East countries, heightening geopolitical risks.

- US reassurances — including temporary permission to purchase Russian crude and potential insurance for shipments through the Strait of Hormuz

— did little to calm market concerns. - Donald Trump stated that the US will now accept only an “unconditional surrender” from Iran.

- US Treasury Secretary Scott Bessent indicated that the US is preparing its largest bombing campaign yet, expected on Saturday night.

- Rising inflation concerns triggered a global sell-off in bonds and equities, while the US Dollar strengthened against major and emerging market

currencies. - Market sentiment weakened further after Bessent suggested that Trump’s proposed 15% global tariff (currently at 10%) could be implemented soon.

- The US January Jobs Report disappointed, with Non-Farm Payrolls (NFP) coming in at –92,000, signalling weakness in the labour market.

Global Equity Markets:

Domestic Equities:

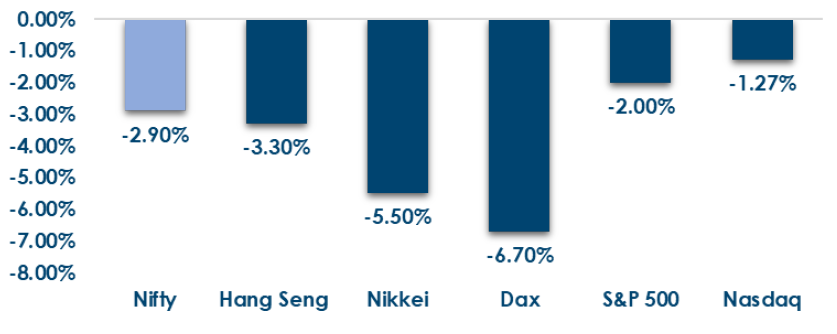

- Major global indices witnessed a sharp correction this week, with the Kospi leading losses at -14%,

followed by Jakarta (-8.6%), CAC (-6.8%), DAX (-6.7%), FTSE (-5.7%), and Nikkei (-5.5%), while S&P 500 (-2%),

Hang Seng (-3.3%), and Straits (-3.9%) also ended the week in the red. - On a trailing vs forward P/E basis, valuations remain elevated beyond large caps — Nifty 50 trades at 20.3x

/ 19.4x, while Midcap 100 and Smallcap 250 are significantly richer at 32.9x / 26.9x and 28.4x / 25.5x

respectively, highlighting the premium still embedded in broader market segments. - In terms of factors, momentum outperformed while Growth underperformed this week

- FPIs have sold net USD 2.3bn of domestic equities in March so far

- FIIs sharply increased selling this week with ₹21,831 Cr outflows versus ₹637 Cr last week, while DIIs

stepped up support with ₹32,787 Cr inflows compared to ₹4,335 Cr previously. - Solar Industries (+12.2%), Jupiter Wagons (+11.8%), and National Aluminium (+11.7%) led gains, while

Netweb Technologies (-16.6%), Mahanagar Gas (-14.0%), and Aegis Vopak Terminals (-12.5%) were the

week’s top laggards.

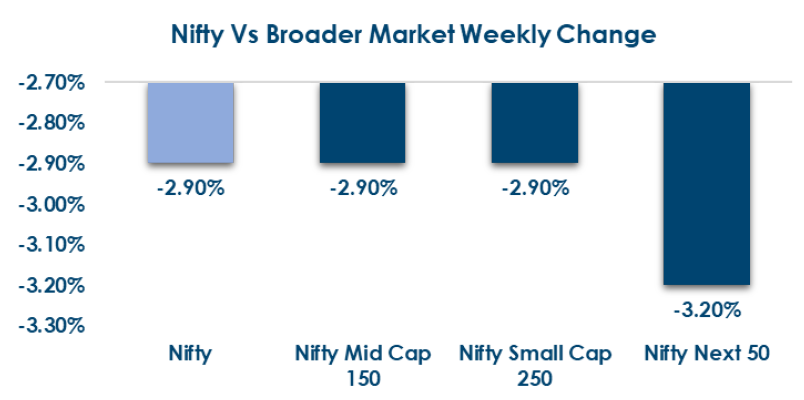

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: Global yields moved higher amid crude-led inflation concerns. US 2Y and 10Y closed at 3.56% and 4.14%, with 10Y yields rising across major economies, including the UK, France, Australia, and Germany.

- India Rates & Flows: Domestic bonds softened with the 10Y G-Sec at 6.69% (vs 6.66%). OIS rates rose sharply while system liquidity stayed comfortable at ~₹3 lakh crore surplus. FPI debt flows remain flat in March.

Real Estate:

Securities and Exchange Board of India (SEBI) settled allegations with Nexus Select Mall Management, manager of Nexus Select Trust, after a ₹24.37 lakh payment, closing the proceedings.

- The action related to not maintaining the ₹10 crore minimum net worth and delayed disclosure of a material financial change to the regulator. Backed by Blackstone, the REIT operates 19 malls across 15 cities and recently acquired a 50% stake in an under-construction mall. The action related to not maintaining the ₹10 crore minimum net worth and delayed disclosure of a material financial change to the regulator.

- Backed by Blackstone, the REIT operates 19 malls across 15 cities and recently acquired a 50% stake in an under-construction mall.

IPOs:

- Four IPOs — Rajputana Stainless, Innovision, Raajmarg Infra InvIT, and Apsis Aerocom — will open between March 9–11, targeting ₹6,600+ crore.

- The issues span NSE, BSE, and the NSE SME platform, with Raajmarg Infra InvIT expected to be the largest.

- Despite a strong pipeline, IPO launches have slowed as firms await better market sentiment and valuations.

Private Equity & Venture Capital:

- PE/VC deals fell 72% WoW to 11, while total funding declined 27% to $177.4 million, largely due to the Holi-shortened week.

- SFO Technologies raised $82 million, with continued investor interest in electronics manufacturing and defence supply chains.

- SAMHI Hotels acquired a 70% stake in RARE India, while QBE Insurance Group bought the remaining stake in Raheja QBE General Insurance.

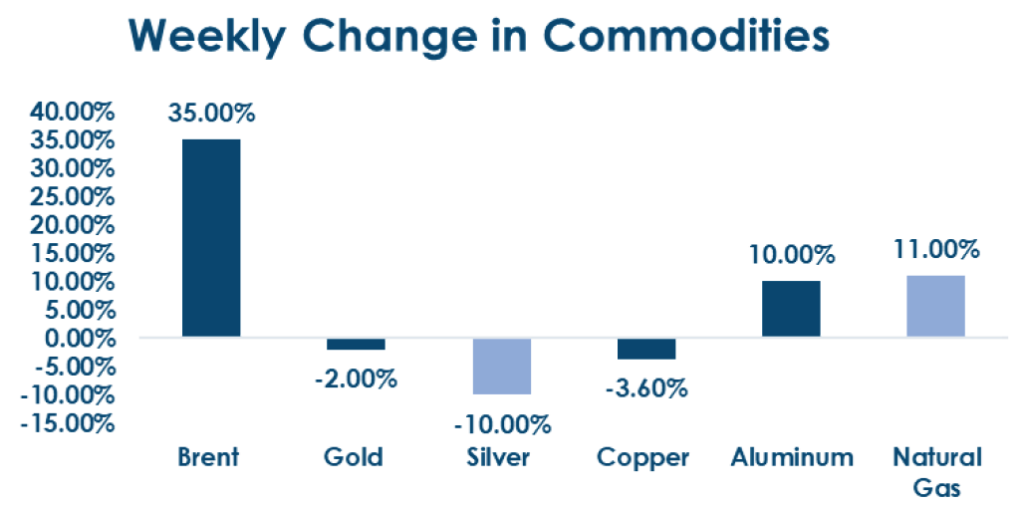

Commodities:

Energy prices soared this week as the US-Iran conflict deepened. US assurances did little to comfort the markets.

What’s New in the World of Wealth Management?

India’s market regulator, the Securities and Exchange Board of India, has urged banks, financial institutions, and

other regulators to strengthen enforcement of insider trading rules, particularly around safeguarding unpublished

price-sensitive information (UPSI). SEBI Chair Tuhin Kanta Pandey noted that the risk of insider trading is not limited

to corporate executives but can also arise from intermediaries, consultants, regulators, or others who gain access to

sensitive information in a fiduciary capacity. The regulator has increased scrutiny in recent years, probing 287 insider

trading cases in FY2024-25 compared with 175 the previous year, highlighting a growing regulatory focus on market

integrity. The push for tighter compliance frameworks and coordination among regulators is aimed at strengthening

investor confidence and improving transparency across India’s capital markets.

A recent commentary highlights that the Reserve Bank of India’s proposed framework to curb mis-selling of

financial products could become a significant development for India’s financial distribution ecosystem. The new

rules aim to strengthen consumer protection by increasing accountability of banks and financial institutions in the

sale of investment and insurance products, an area that has long been criticised for aggressive sales practices and

opaque disclosures. While the regulatory intent is widely seen as positive for retail investors, the commentary notes

that the real impact will depend on consistent enforcement and meaningful penalties, which could ultimately shift

the industry toward more transparent and client-centric advisory practices.

Our Views: What we Like?

Equities: The crucial 24600 support on Nifty50 got taken out this week. This is the level we had rebounded from on

budget day. The same is now likely to act as a resistance. There is a gap support at 24170, which is now a crucial

level on the downside. If that gets taken out, we could head to 23600-23800. From a long term perspective, we

believe every dip of 3% is a good level to enter. We prefer to stick to quality and value. We prefer being overweight

in Metals, Banks, and Energy, and underweight in IT and Realty

Fixed Income: Rates sold off this week on inflationary concerns, given the Brent move. While move in Gsec may be muted on OMOs, given that supply for the current fiscal is over, Rates may continue to sell off. If elevated crude prices persist, the RBI may be compelled to consider tightening. RBI announced a Rs 1 lakh crs OMO purchase after market close yesterday. We expect the 10-year to trade in a 6.60-6.85% range for the coming few weeks

Commodities: We are seeing bizzare correlations play out. One would expect base metals and to drop and precious metals to rally during risk off times, particularly given inflationary concerns. However this week we saw exactly the opposite. We believe this breakdown in correlations may not play out for long and therefore prefer buying

precious metals on dips. Silver around USD 70-75 and Gold around USD 4600-4800 are good levels to enter.

FX: We are likely to see the currencies of energy-deficient countries underperform till the conflict continues