Billionz Multi-Asset Weekly Newsletter

Energy Shock Rattles Markets, Rupee Hits Fresh Lows

Global Developments:

- Energy Crisis Deepens: Rising uncertainty over continuity of industrial activity and daily life as the global energy situation turns increasingly grim

- War Escalation Hits Supply: Conflict in the Middle East has intensified, with direct targeting of energy infrastructure—shifting the concern from logistics (Strait of Hormuz) to actual production disruptions.

- Longer-Term Supply Risks: Even post-conflict, supply restoration may be delayed due to damage to production facilities, keeping markets tight

- Temporary Relief from US: The US has released ~140 million barrels of Iranian crude held at sea to ease supply pressures, though this is largely viewed as a short-term cushion

- Geopolitical Uncertainty Persists: While President Trump is winding down US military involvement, the outlook hinges on Iran’s response, which has already demanded assurances against future attacks

- Central Banks Stay Cautious: Major central banks—Fed, ECB, BoE, and BoJ— held rates steady this week, maintaining a hawkish stance amid rising inflation risks driven by energy shocks.

Global Equity Markets:

Domestic Equities:

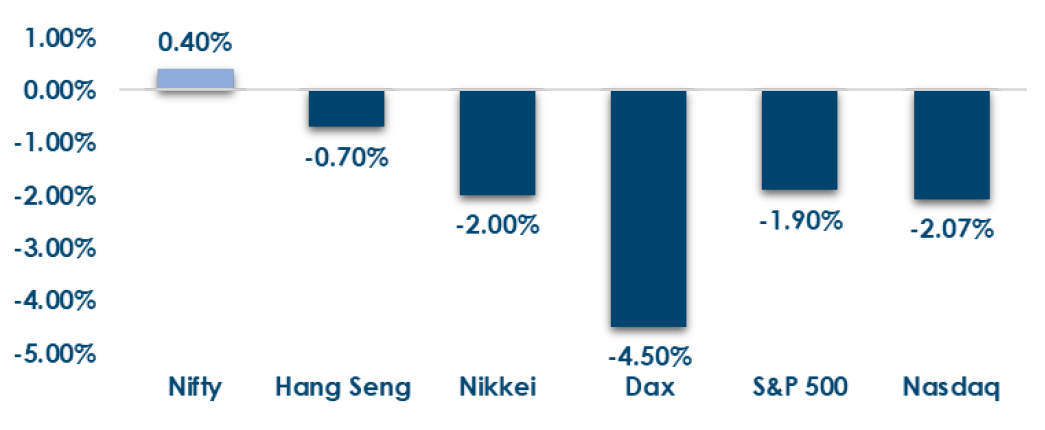

- Global equities saw broad weakness this week, with major indices like the S&P 500 (-1.9%), DAX (-4.5%), FTSE 100 (-3.3%) and CAC 40 (-3.1%) declining, while select Asian markets showed resilience with KOSPI (+5.3%) and Straits Times Index (+2.2%) posting gains.

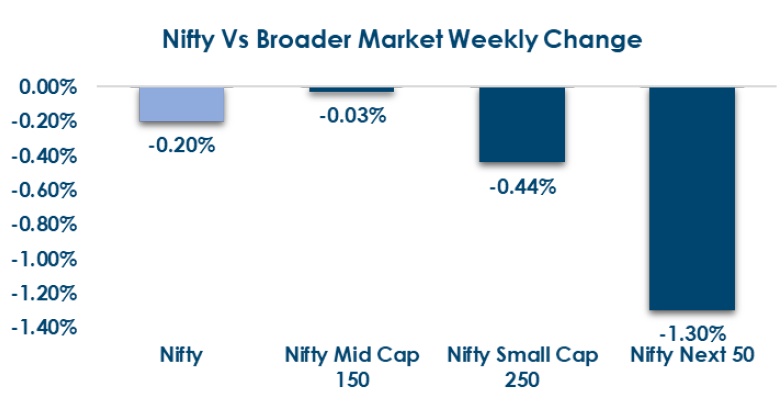

- Valuations: Nifty50 remains relatively cheaper at 19.2x/18.2x, while Midcaps (31.3x/25.6x) and Smallcaps (27.2x/24.6x) continue to trade at a premium.

- In terms of factors/styles, momentum outperformed while growth underperformed this week

- FPIs have sold net USD 9.6bn of domestic equities in March so far

- Institutional activity softened this week, with both FII (₹29,898 Cr) and DII (₹30,642 Cr) inflows declining versus last week.

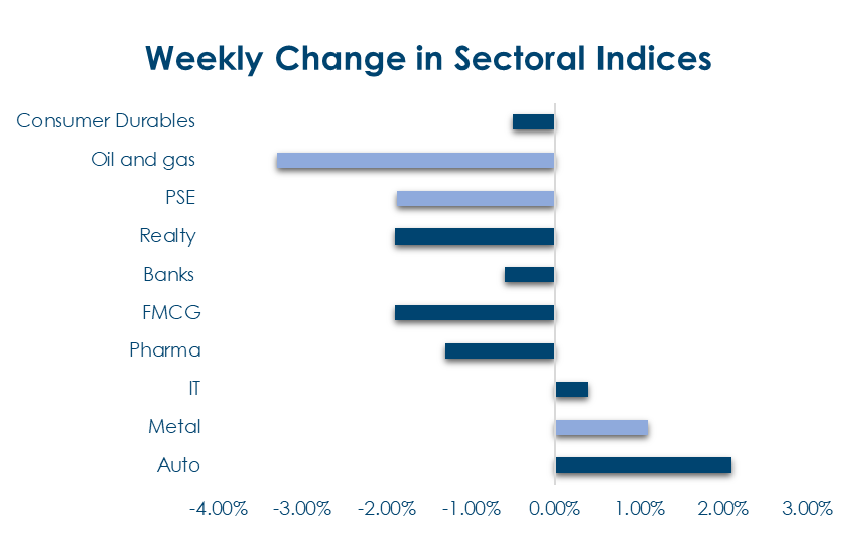

- Olectra Greentech led gains (+24.6%) while IDBI Bank topped losses (-20.7%), with notable moves across power, energy, and metals.

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: Bond yields rose sharply across major economies amid rising inflation expectations driven by higher energy costs, led by the UK (+22bps), Italy (+24bps), and the US (+16bps), while Japan stayed stable andChina saw a slight decline

- India Rates & Flows: Yields edged higher with the 10Y at 6.74% (+5bps) and 5Y at 6.46% (+10bps), while liquidity tightened towards neutral; short-end rates stayed firm (1Y CD ~7.21%, T-bill ~5.60%) and FPIs remained sellers (~USD 1.6bn in March).

Real Estate:

- BInstitutional focus remains on incomegenerating assets, with NDR InvIT acquiring a Pune warehousing asset (~₹203 Cr) backed by long-term leases (~8.7 years), reflecting strong demand in logistics real estate.

- The acquisition expands its portfolio to 67 warehouses across 17 cities (~22.17 mn sq ft), highlighting continued scale-up and investor preference for stable, yield-driven assets supported by e-commerce and manufacturing demand.

IPOs:

- IPO Pipeline: 4 IPOs (~₹2,010 Cr) lined up across segments, reflecting strong liquidity but with potential demand fragmentation.

- Key Highlights: Powerica leads, alongside Amir Chand Jagdish Kumar, Sai Parenterals, and SME player Tipco Engineering; proceeds focused on growth and deleveraging.

Private Equity & Venture Capital:

- Investments surged to ~$660 Mn across 27 deals, led by KKR’s $310 Mn investment in Allfleet India, with overall activity remaining skewed toward smaller, selective mid-market deals.

- Deal activity stayed steady (~10 deals), highlighted by Nazara’s $100+ Mn gaming acquisition and DWS Group’s stake in Nippon Life India AIF, indicating continued strategic consolidation across sectors.

Commodities:

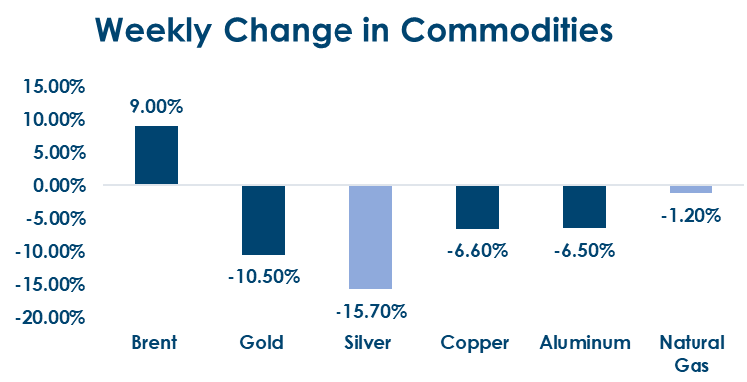

- Commodities saw sharp divergence this week, with energy leading gains (Brent +9%, European gas +18%) while metals and precious metals corrected steeply (Gold -10.5%, Silver -15.7%, base metals ~6% down).

- Precious metals cracked this week (even more than base metals). This is despite risk-off and USD weakness.

What’s New in the World of Wealth Management?

Amid heightened global volatility, market participants are increasingly emphasising investor discipline and longterm

positioning. Harish Ahuja from the National Stock Exchange of India advised retail investors to avoid panic

selling, highlighting that the current correction is part of a broader global trend driven by geopolitical tensions.

Despite near-term fluctuations, India’s macroeconomic fundamentals remain resilient, supported by steady GDP

growth and improving industrial indicators, reinforcing the case for staying invested through cycles.

At the same time, regulatory focus in capital markets is shifting toward tightening oversight in emerging asset

classes, particularly crypto. A recent report by the Financial Action Task Force underscored risks associated with

offshore virtual asset service providers (VASPs), validating India’s stance on stricter compliance requirements. The

debate is now evolving beyond enforcement, with policymakers balancing investor protection and market

development, indicating a push toward building a more transparent and regulated digital asset ecosystem

alongside traditional capital markets.

Our Views: What we Like?

Equities: After the news of an attack on energy facilities, Nifty50 gave up all initial gains of the week and retraced from

highs around 23900, ending just above 23100. We could see more pain in the short term as industrial and

manufacturing output could be hurt by the energy crunch, leading to a sharp revision downward in earnings

estimates. 21800 is the next key level on the Nifty50. On the flip side, a Break above 23900 could now signal a

reversal on the upside. We believe this correction is a good entry point for those looking to construct a long-term

portfolio. Market cap and sectoral allocation is the key as several themes are playing out

Fixed Income: We have seen a sell-off in rates on account of inflationary expectations. However, bonds continue to remain

relatively resilient due to a lack of supply and RBI buying in primary as well as secondary markets. We expect the

yield on the 10y IGB to trade in a 6.65-6.85% range over the next 6 weeks.

Commodities: We believe the current bizzare correlations will likely not play out for too long and precious metals will see dip

buying amid current uncertain times. We remain bullish on Silver and Gold and believe one should definitely

have allocation to these in long term portfolios.

FX: The dollar index has retraced from the top of its range of around 100.50. It has been trading in a 95.50-100.50

range over the last several months.