Billionz Multi-Asset Weekly Newsletter

Markets Unsettled as War Risks Intensify

Global Developments:

- Trump delivered a national address on Wednesday evening. The market was expecting timelines for when the war would end. However, the comments were extremely general and vague. While he mentioned that the US would get out of Iran in 2-3 weeks, he said the US would hit Iran hard in that period. He has also asked allies to work towards reopening the Strait of Hormuz.

- Meanwhile, blows continue to be exchanged between Israel and Iran and the US and Iran. Iran striking essential facilities in the Middle East is a key risk for supply chains.

- Domestically, focus will be on the RBI policy in the coming week. Emergency, out-of-policy action cannot be ruled out either, and we may see the RBI indicate the possibility of that in the upcoming policy. There is a strong possibility of a 25bps rate hike to tame inflationary pressures and control the Rupee.

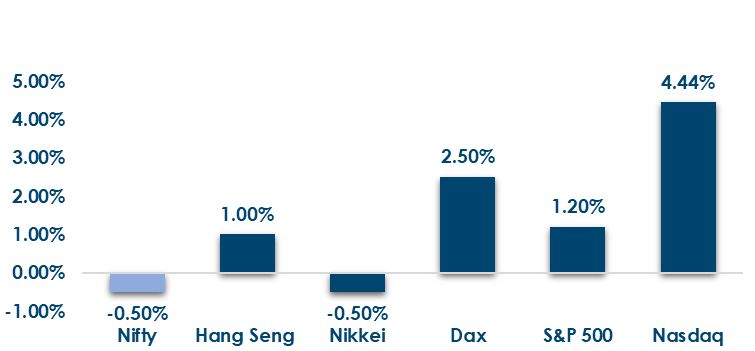

Global Equity Markets:

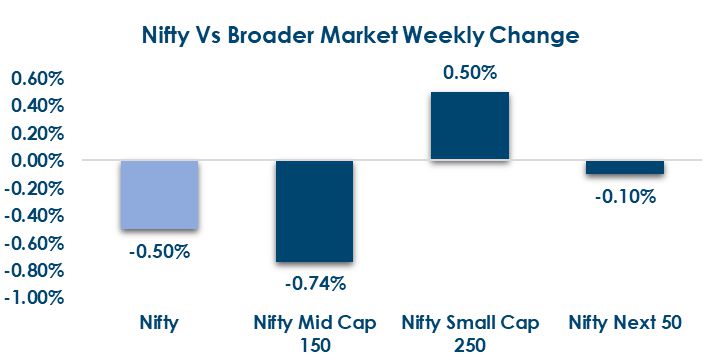

Domestic Equities:

- Global markets were mixed this week—Europe led gains (FTSE +4.7%), the US saw modest upside (S&P 500 +1.2%), while Asia remained largely weak.

- Nifty TTM PE stands at 20, Midcap100 TTM PE stands at 33.2, and Smallcap250 TTM PE is at 26.7.

- FPIs pulled out net USD 12.7bn from domestic equities in March, the biggest single-month outflow since Oct’24

- FII and DII inflows moderated this week, with FIIs at ₹11,163 Cr and DIIs at ₹14,894 Cr, both lower than the previous week’s stronger inflows

- Top movers this week saw Latent View (+19.9%), Ola Electric (+16.8%), and Avenue Supermarts (+11.8%) leading gains, while Acutaas Chemicals (-17.1%), LG Electronics India (-14.2%), and Authum Investment (-13.6%) lagged.

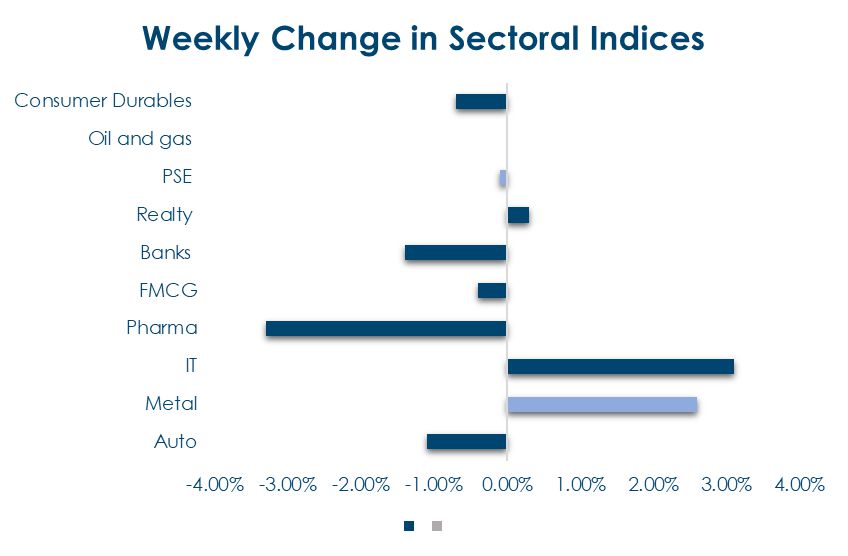

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: Global 10Y yields softened across major economies (UK, France, Germany), while Japan and China saw a slight uptick.

- India Rates & Flows: India 10Y yield jumped 19bps to 7.13% (near 2-year highs) amid fiscal concerns and rising crude-led inflation expectations, with short-end rates firming (OIS, CD), liquidity easing (cooler MIBOR, high SDF parking), continued FPI outflows (~$900mn in March), and SDL cut-offs crossing 8%—signaling elevated borrowing costs.

Real Estate:

- Institutional activity in real estate remained robust, with Mindspace REIT acquiring a 2.6 mn sq ft Chennai commercial asset for ~₹2,541 crore at a discount to valuations— reflecting disciplined capital deployment and portfolio strengthening.

- The deal, sourced from sponsor K Raheja Corp under a ROFO arrangement, marks its second Chennai acquisition; coupled with a ₹675 crore preferential issue, it signals strong balance sheet flexibility and growth momentum.

IPOs:

- Primary market activity to stay subdued: No mainboard IPOs lined up; activity driven by Safety Controls & Devices Ltd’s ₹48 crore SME IPO (Apr 6– 8), focused on working capital, debt repayment, and general corporate needs.

- Selective activity in alternative assets: PropShare Celestia REIT IPO (~₹244.65 crore, opening Apr 10) aims to acquire a fully leased Grade A+ commercial asset in Ahmedabad, reflecting a limited and niche issuance pipeline.

Private Equity & Venture Capital:

- PE/VC activity slowed during the holidayshortened week, with ~$822M raised across 21 deals—lower than the previous week due to the absence of large-ticket transactions and a more selective funding environment.

- Deal activity stayed steady (~10 deals), highlighted by Nazara’s $100+ Mn gaming acquisition and DWS Group’s stake in Nippon Life India AIF, indicating continued strategic consolidation across sectors.

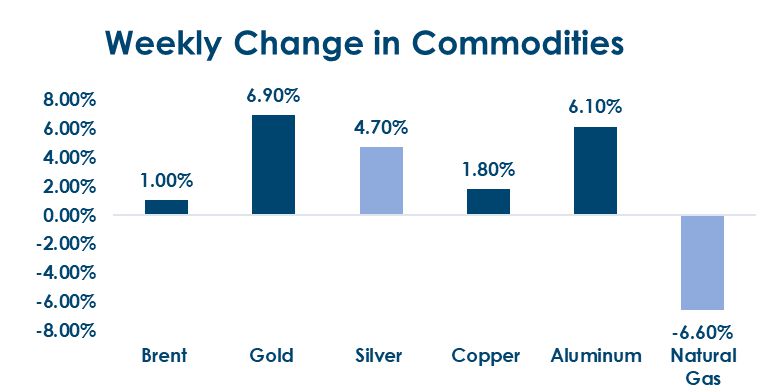

Commodities:

- Commodities saw mixed momentum this week, with energy volatile (Brent +1%, WTI +18%, natural gas down), metals firming (aluminium +6.1%, copper +1.8%), and precious metals rallying strongly (gold +6.9%, silver +4.7%).

- Energy prices continue to remain extremely volatile and sensitive to war related news. Attacks ok Energy facilities in Kuwait have stoked a fresh bout of nervousness. WTIBrent spread inverted this week as Trump’s national address did little to comfort the markets and infact added to the anxiousness as he said US would hit Iran hard over the next 2-3 weeks.

What’s New in the World of Wealth Management?

A key trend emerging in capital markets is the increase in transaction costs for derivatives trading, following the

recent hike in Securities Transaction Tax (STT) effective April 1, 2026. STT on futures has risen from 0.02% to 0.05%,

while options have increased from 0.1% to 0.15%, directly impacting trading profitability. Unlike profit-based taxes,

STT is levied on turnover, meaning it applies regardless of gains or losses—making it particularly significant in highfrequency

and expiry-driven trading strategies. This shift effectively raises breakeven thresholds for traders and

could discourage excessive speculative activity, especially among retail participants.

Additionally, regulatory tightening is extending to leverage within the system, with the Reserve Bank of India’s

revised norms on bank guarantees (effective July 1) expected to further impact derivatives markets. As a significant

portion of industry margins is backed by bank guarantees, reduced leverage could lead to a near-term decline in

trading volumes by 10–15%, according to market estimates. While the adjustment is likely to play out gradually, the

combined impact of higher transaction costs and tighter leverage norms signals a structural shift toward a more

disciplined and risk-aware trading environment.

Our Views: What we Like?

Equities: 22100, levels on the Nifty50 from which we rebounded this week, have become a very crucial level. There is a major trend line support there. The possibility of a bounce towards 23100 and 23600 cannot be ruled out. However, of 22100 breaks, we could look at another 5% downside from that level. We recommend increasing allocation to equities at current levels from a long-term investment point of view. We are overweight in the IT sector as we believe a lot of negativity is already in the price.

Fixed Income: A 10-year Gsec yield above 7% seems extremely attractive from a long-term perspective. We expect the RBI to

announce OMOs to soothe sentiment. 10-year SDLs close to 8% are also extremely attractive from a long-term

investment standpoint.

Commodities: Energy prices are likely to remain extremely sensitive to headlines. Break above USD 120 on Brent could result in a vertical move higher of about 15-20%

FX: The dollar continues to remain volatile but within a range against majors. 1.14 on Euro, 1.31 on Pound, and 160 on JPY are the key levels to watch. These are the support levels for respective currencies against the Dollar. RBI’s measures may reduce the pressure on the rupee over the near term. The offshore-onshore spread may remain elevated. Onshore Rupee may adjust as per NDF moves overnight, and chances of gap moves are higher.