Billionz Multi-Asset Weekly Newsletter

Markets Bounce, But Fragile Peace Keeps Risks Elevated

Global Developments:

- After threatening to almost ruin Iran if they fail to open the Strait of Hormuz before a deadline, President Trump backed down, and the markets rejoiced as the worst seems to be behind for now

- However, the ceasefire was on shaky ground, and there was disagreement on whether the Israel-Lebanon combat was part of that.

- High-stakes peace talks between the US and Iran are to happen in Pakistan over the weekend

- Trump has now warned that the US will resume its military action with even more intensity if a peace deal isn’t reached.

- While crude cooled off, the risk premium has not completely gone away, and we don’t seem to be completely out of the woods yet.

Global Equity Markets:

Domestic Equities:

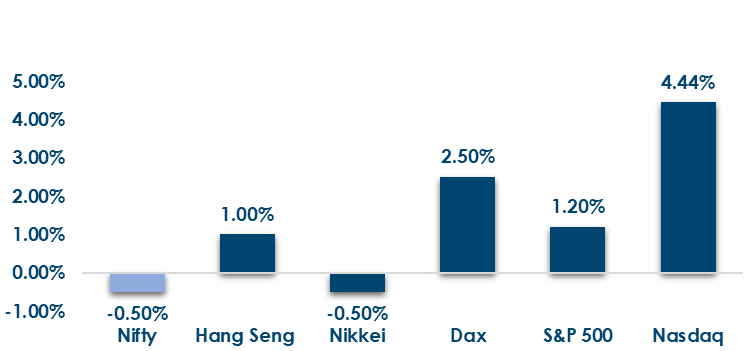

- Broad-based rally led by Asia—KOSPI (+11%), Nikkei 225 (+7.4%), and Taiwan (+7.2%). Europe remained strong with CAC 40 (+5.3%) and FTSE 100 (+4.3%), while the S&P 500 gained 3.6%.

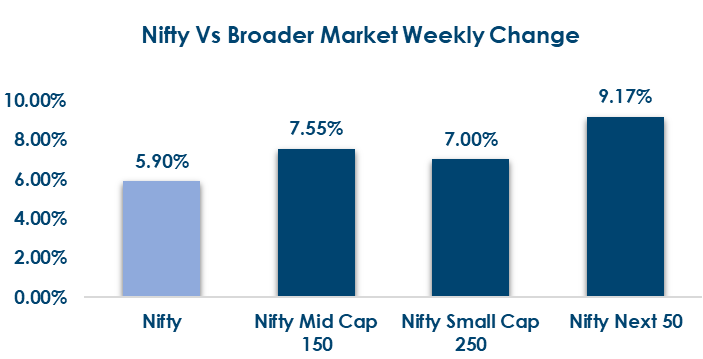

- Benchmark indices continue to trade at elevated levels, with Midcaps leading at 35.8x, followed by Smallcaps at 28.5x, while the Nifty50 remains relatively moderate at 21.1x.

- India VIX dropped from 25.46 to 18.85

- FPIs have sold net USD 5.1bn of domestic equities in April after selling net USD 12.7bn in March

- FIIs stepped up buying this week at ₹12,543 Cr, while DIIs remained strong contributors at ₹13,514 Cr, though slightly lower than last week.

- Ola Electric Mobility surged 44.3%, leading the gainers, while Jain Resource Recycling declined 7.9%, topping the losers’ list.

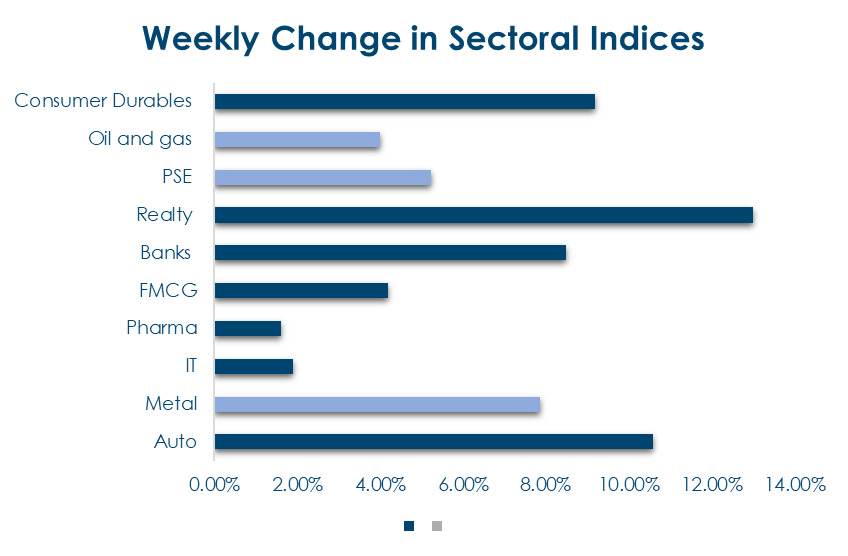

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: Global yields edged higher, led by Germany (+6bps) and Japan (+4bps), with France also firming, while the US and UK remained largely stable and Australia saw a sharp decline (-7bps).

- India Rates & Flows: Domestic yields softened with the 10Y G-Sec down 22bps to 6.91%, supported by RBI’s unchanged stance and surplus liquidity (>₹4 lakh Cr); OIS curve eased sharply, short-term rates remained anchored below repo, and FPIs turned net sellers with ~$1.5bn outflows in April so far.

Real Estate:

- ASK Property Fund exited two residential debt investments (~₹400 crore) in Mumbai & Gurgaon within a short timeframe, delivering strong returns (IRR ~18–21%).

- Continues strong exit track record (including ~2.1x from a Noida project), with a diversified pan-India portfolio and over ₹9,100 crores of capital raised.

IPOs:

- Primary market activity remains muted with no major mainboard IPOs; key highlight is the ₹1,340 crore Citius TransNet InvIT offering, signalling sustained interest in yield-focused infrastructure assets.

- SME segment sees limited but steady traction, led by Mehul Telecom’s ₹27.73 crore IPO, indicating cautious yet continued participation in smaller listings.

Private Equity & Venture Capital:

- PE/VC activity rebounded with 26 deals, but total funding fell 37% to ~$515M, signalling a tilt toward smaller deals; financial services & real estate dominated (~74% of value), reflecting preference for asset-backed, scalable models.

- Key highlights & M&A trend: KreditBee raised $280M (Series E) and SILA Solutions secured $100M; deal flow remained early/mid-stage-heavy, while M&A slowed to 8 deals with no $1B+ transactions, indicating cautious, targeted consolidation.

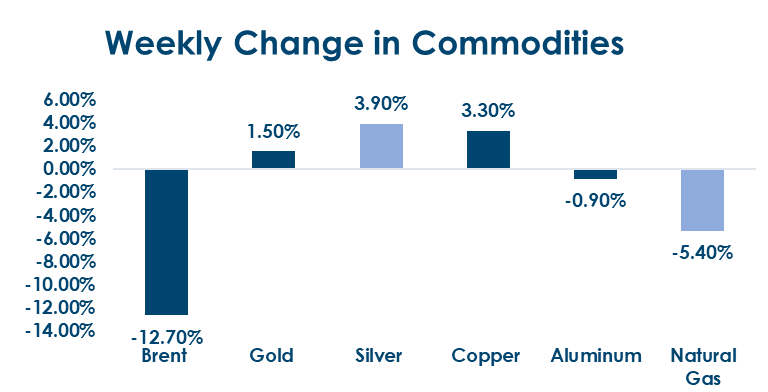

Commodities:

Commodities were broadly weak, led by a sharp

fall in crude (WTI -13.4%, Brent -12.7%), while

natural gas also declined; base metals were

mixed with copper gaining, and precious metals

remained resilient with gold and silver rising.

What’s New in the World of Wealth Management?

Regulatory focus remained sharp this week, with the RBI moving to tighten oversight on offshore rupee derivative trades by mandating greater reporting from banks. The step aims to improve transparency in a segment that has contributed to currency volatility. Additionally, recent restrictions on banks’ overnight positions have added to near-term pressure on the rupee, highlighting the central bank’s balancing act between currency stability and market liquidity.

On the earnings front, Tata Consultancy Services kicked off the IT results season with a steady Q4 performance, supported by a strong deal pipeline and growing AI-led opportunities. However, cautious management commentary and macro uncertainties kept sentiment muted, with expectations of conservative FY27 guidance across IT majors as geopolitical risks and AI-driven pricing pressures weigh on growth outlook.

Our Views: What we Like?

Equities: We had highlighted last week that 22100 was an extremely crucial level on Nifty50 and that a possibility of bounce back to 23100 and 23600 cannot be ruled out. We have risen past that now. However, we do not see a complete V-shaped recovery and believe 24400 is an e extremely strong resistance. We remain overweight on Banks, the financial sector, and IT in our model portfolio. March AMFI data was extremely encouraging, with Equities seeing net inflows of over Rs 40000crs, and midcap, flexicap, and Smallcap funds receiving more inflows compared to large-cap funds.

Fixed Income: We had highlighted that above 7% on 10-year bonds are extremely attractive levels to add duration to the portfolio. Successful Measures taken by RBI to cool off USDINR have given it headroom to keep rates on hold. One can look to pay 5y OIS on dips to 6.10%

Commodities: We prefer adding gold and silver on dips. These will do well in a weak-dollar environment. Precious metals are following the dollar theme rather than the risk theme. We are bullish on Aluminum as well. Brent has resisted thrice at USD 120 per barrel. Break of that level could trigger massive stops and result in a vertical move. However, that is not the base case. At the same time, the probability is more than that of an extreme tail risk event.

FX: The 95.50-100.50 range continues to hold extremely well on the Dollar index. USDINR is likely to meet real demand on every dip.