Billionz Multi-Asset Weekly Newsletter

Nifty Eyes 26,300 Breakout; IT & Banks in Focus.

US Developments:

- The current US government shutdown is now the second-longest ever, into its 25th day.

- The September CPI print was delayed because of the shutdown. Both headline and core CPI prints came in a tad lower than expected at 3% yoy. It is possible that the Oct CPI print may not be released. However, with inflation gradually easing and labor market conditions weakening, we are likely to see two more cuts by the end of 2025. This would take the Fed funds rate to 3.50-3.75% from the current 4-4.25%. In fact, the next Fed meeting is due next week itself, on Wednesday, in which the Fed is likely to cut by 25bps.

- The US imposed sanctions on Russian oil giants Rosneft and Lukoil, which together account for 5% of the global crude output.

- Trump claimed that China and India were scaling back crude purchases from Russia upon his request.

- Optimism around the India-US trade deal has lifted sentiment onshore, and Trump’s meeting with Xi on the sidelines of the APAC summit (which could lead to a trade truce between the US and China) in South Korea next week has lifted global risk sentiment.

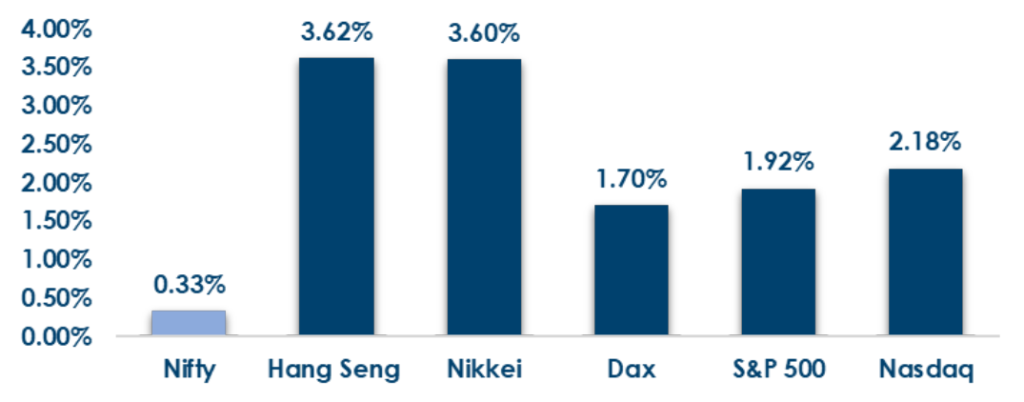

Global Equities

This is how Global Equities performed this week.

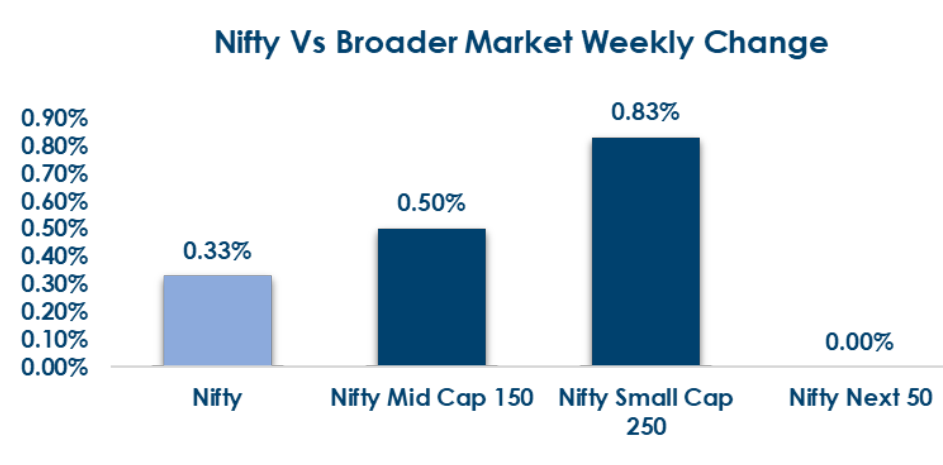

Domestic Equities

- Optimism around the US-India trade deal lifted sentiment. Nifty50 did cross the 26000 mark but ran into profit-taking and was not able to take out the all-time high of last September

- Valuations across key benchmark indices remain elevated, with the Nifty50 trading at a trailing P/E of 22.9x and a forward P/E of 22.1x. The Midcap100 continues to command a premium, trading at 33.0x on a trailing basis and 29.5x forward, while the Smallcap250 stands at 29.3x trailing and 27.9x forward, indicating relatively rich valuations across the broader market.

- In terms of factors, value and market cap outperformed, while Growth and Momentum underperformed this week

- For the 100 NSE500 companies that have reported Jul-Sep Qtr results so far, the average Sales surprise has been -0.9% and the average Earnings surprise has been -2.7%

- FPIs have invested net USD 830mn in domestic equities in October so far.

- Top gainers in the market were Shipping Corporation of India (21.8%), Sammaan Capital Ltd. (12.9%), and Birlasoft Ltd (11.9%).

- Top losers included Tejas Networks Ltd. (-8.7%), Godfrey Philips Ltd. (-8.5%), and Poonawalla Fincorp (-8%).

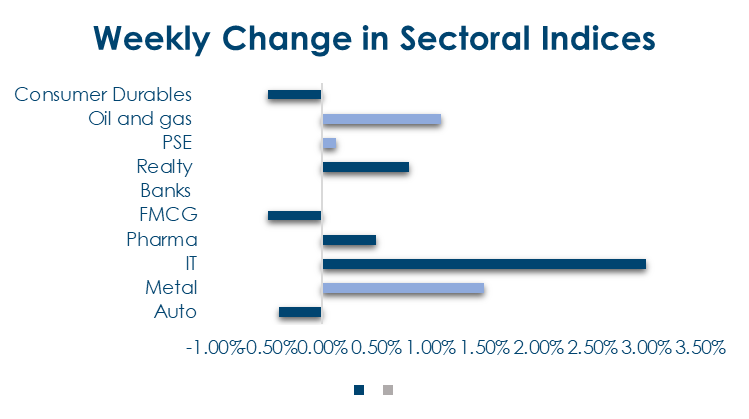

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices performed this week:

Fixed Income:

- US 2y and 10y yields rose 2bps this week to 3.48% and 4%, respectively.

- UK 10y yield fell 7bps on softer inflation, while Eurozone 10y yields rose 5–7bps.

- India’s 10y G-sec traded in a 6.49–6.56% range, ending at 6.53%; 1y and 5y OIS rose to 5.45% and 5.65%.

- Liquidity remains neutral; 10y AAA PSU and NBFC spreads stand at 52bps and 85bps, with FPIs investing USD 1.9bn in bonds this month.

Real Estate:

- India’s real estate sector raised USD 1.15bn in Q2 FY26, more than doubling from the previous quarter, driven by IPOs, QIPs, M&A, and PE activity.

- Retail real estate continues to attract strong investor interest, highlighted by Nexus Select Trust, India’s First listed retail-mall REIT.

- Nexus plans to expand its portfolio to 18–20mn sqft across 30–35 malls by FY30, backed by ₹5,000–6,000 cr of debt and equity funding.

- High occupancy rates and solid rental growth support the REIT’s expansion strategy, reflecting sustained confidence in organised retail.

IPOs:

- The Indian IPO market is picking up, with five companies, including Lenskart and Groww, set to raise nearly ₹35,000 crore, supported by strong retail participation.

- Next week’s IPO calendar is modest, featuring Orkla India (₹1,667 crore offer) and two SME listings, Jayesh Logistics and Game Changers Texfab.

- Orkla’s pricing (₹695–730/share) highlights continued demand for established consumer brands.

- Market outlook is constructive, but investors should remain selective amid high valuations, with SME listings helping broaden participation.

Private Equity & Venture Capital:

- PE and VC deal count fell sharply to 10 in the week ended October 24, down from 34 the previous week, marking one of the weakest weeks this year.

- Despite fewer deals, total deal value surged to $1.15 billion (~₹10,095 crore), up nearly 50% from the prior week, driven by a few large transactions.

- M&A activity remained soft with only three deals, though the Emirates NBD–RBL Bank acquisition and Blackstone’s $716 million investment in Federal Bank stood out.

- Overall, deal volume was muted due to the festive season slowdown, but large-ticket transactions lifted total value.

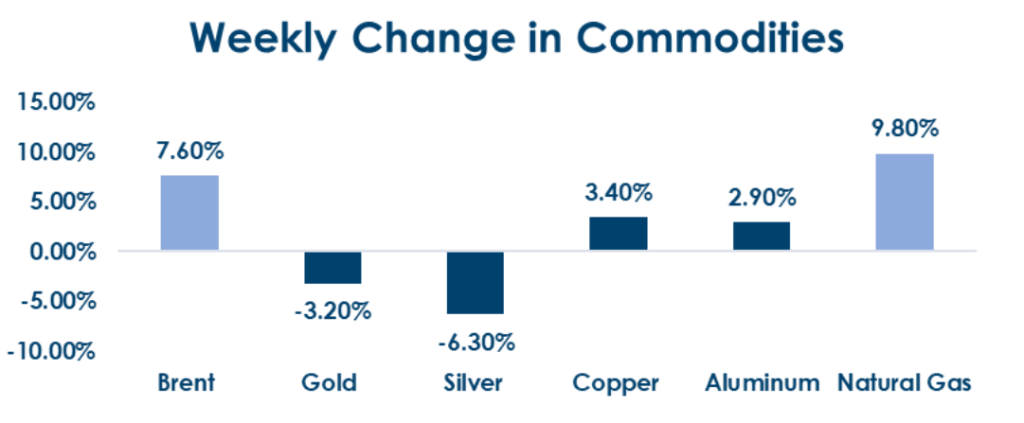

Commodities: Gold and Silver ran into profit-taking this week after printing all-time highs.

Brent spiked as the US imposed sanctions on Rosneft and Lukoil, and on the Trump administration’s claims that India and China will be tapering Russian crude purchases

What’s New in the World of Wealth Management?

The Indian wealth-management sector continues to mature rapidly, driven by digital-first fintech platforms, alternative

asset strategies, and broadening wealth demographics. In a recent earnings release, a leading fintech firm noted that

“India is at the start of a multiyear expansion across investing, wealth management, protection, credit, and fixed income.”, underscoring how digital adoption and an expanding investor base beyond major metros are reshaping the landscape.

With risk sentiment still heightened, wealth-management firms are emphasising diversification, tech-enabled advice, and

deeper client engagement. The filings show that firms are investing in AI-powered tools, a broad range of products

(including commodities and global funds), and developing wealth solutions for both high-net-worth and emerging

affluent segments. The combined effect is an ecosystem transitioning from purely advisory into a full-service wealth stack

— spanning investment, protection, credit, and technology. As volatility persists, the industry’s focus seems to be on

building long-term investor behaviours, expanding penetration into non-metro markets, and layering premium solutions

backed by robust digital infrastructure.

Our Views: What we Like?

Equities: Indian equities have underperformed this year in absolute and Dollar terms. This week, Nifty50 rallied on optimism around the India-US trade deal but ran into profit-taking above the 26000 mark. A vertical move of 5-7% is likely if Nifty50 takes out 26300 convincingly. Until then, we can expect to see range-bound price action in 25300-26300. We have increased our equity allocation, and in terms of sectors, we are overweight on IT and Banks in our model fund. A lot of pessimism is already priced into IT stocks, and banks may do well in a low-interest-rate environment.

Fixed Income: We expect the yield on the benchmark 10y to trade in a 6.45-6.65% range. Any uptick towards 6.65% is a good opportunity to add duration to the portfolio. Current levels on 5y OIS seem attractive to pay to convert floating-rate exposures to fixed.

Commodities: We are bullish on Brent and Copper and neutral on previous Metals now, having captured a large part of this rally.

FX: We continue to believe, despite this week’s Dollar strength, that we are still in a phase of overall Dollar weakness, especially in the case of G10. We expect Dollar weakness to be less pronounced against Emerging market currencies, especially the Rupee