Billionz Multi-Asset Weekly Newsletter

Nifty Holds Ground; Wealth Managers Eye Global Horizons.

US Developments:

- Fed cuts rates by 25 bps, in line with expectations, but highlighted that a December rate cut is not guaranteed. Market probability for another 25 bps cut in December currently stands at ~62%.

- US–China trade tone improved following Trump’s APAC meeting with Xi. China agreed to increase imports of U.S. soybeans and other agricultural goods.

- The U.S. also avoided a disruption in rare earth metal supplies, while the recent 30% tariff on Chinese goods was reduced to 20%, signaling early steps toward de-escalation.

- India–US trade ties have shown positive developments recently, but lack of tangible progress could lead to renewed market uncertainty.

- The U.S. government shutdown has now lasted a month, and as it is on track to become the longest in history, it may soon shift market focus back from trade headlines.

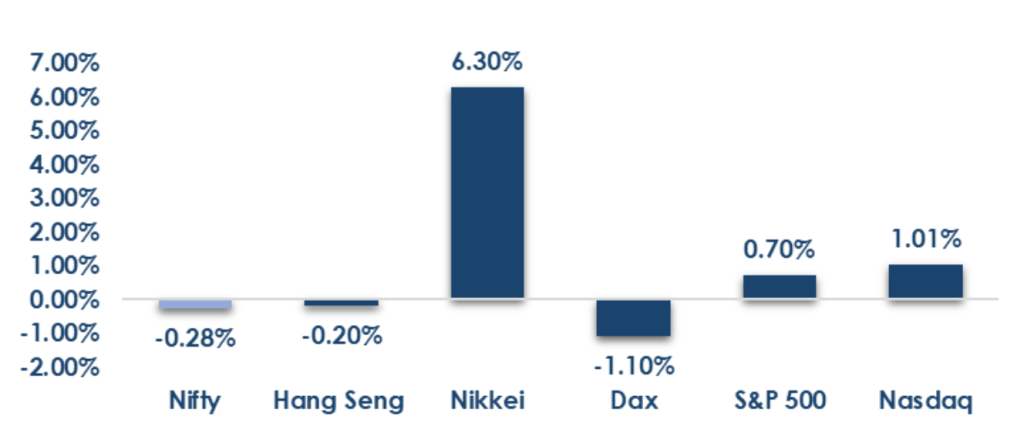

Global Equities

This is how Global Equities performed this week.

Domestic Equities

- Out of the 6 of Magnificent 7 earnings released so far, Meta and Tesla have delivered a negative Earnings surprise.

- Valuations across key benchmark indices remain elevated, with the Nifty50 trading at a trailing P/E of 22.8x and a forward P/E of 22.1x. The Midcap100 continues to command a premium, trading at 33.3x on a trailing basis and 30x forward, while the Smallcap250 stands at 29.6x trailing and 28x forward, indicating relatively rich valuations across the broader market.

- Out of about 200 companies that have published results for Q2FY26, revenue surprise has been -0.9% while Earnings surprise has been +13.8%.

- In terms of factors, value and growth both did well this week while momentum and market cap underperformed

- FPIs invested net USD 1.7bn in domestic equities in October.

- FIIs turned net sellers this week with outflows of ₹2,103 crore, while DIIs provided strong support with ₹18,804 crore in inflows (vs ₹5,945 crore last week).

- Top Gainers: Chennai Petroleum (+26.8%), Five Star Business Finance (+21.6%), Blue Dart Express (+18.1%) | Top Losers: Cohance Lifescience (–14%), Vodafone Idea (–9.3%), 360 One Wam (–8.9%).

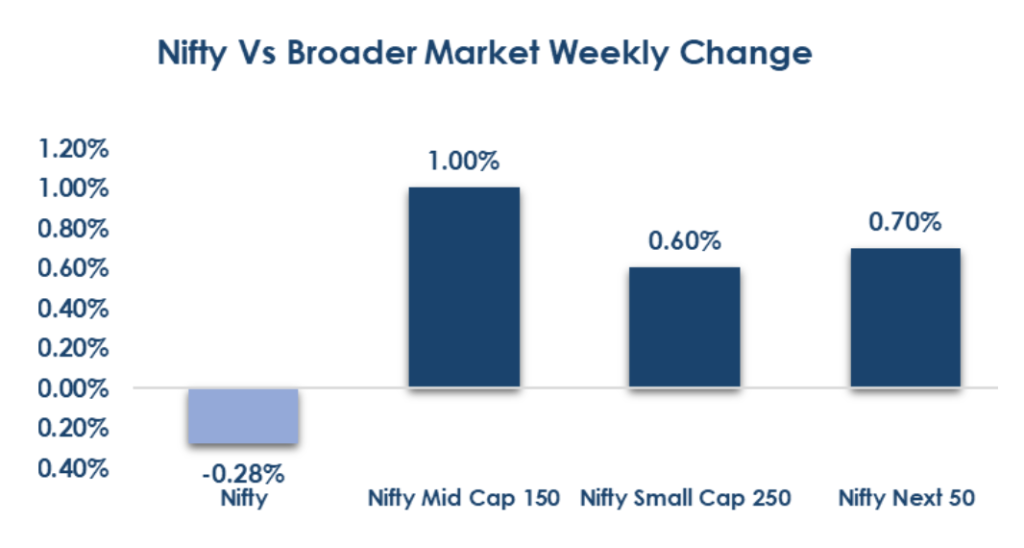

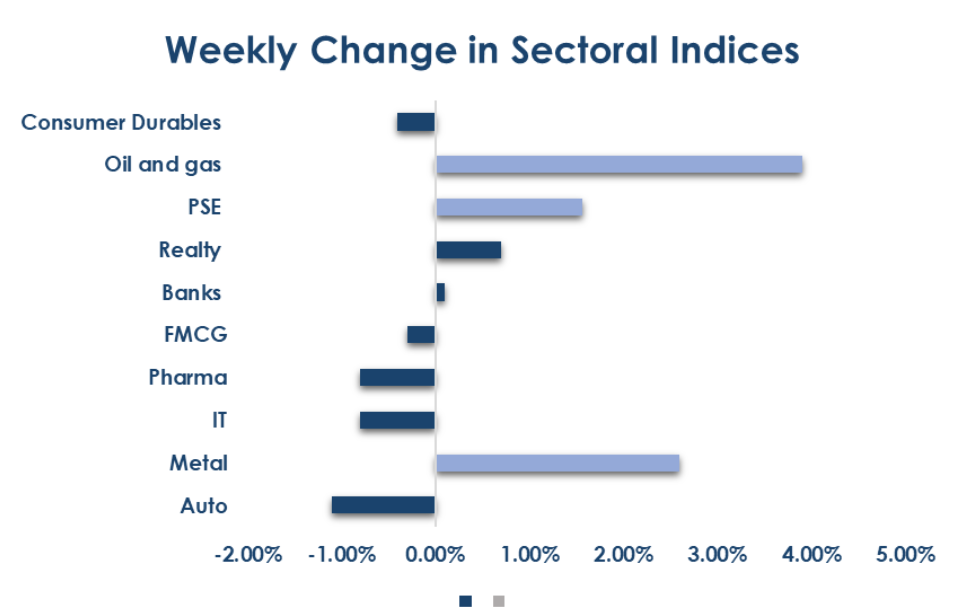

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices performed this week:

Fixed Income:

- Global Rates: The US 10Y rose 10 bps to 4.08% and the 2Y rose 8 bps to 3.57% amid a hawkish Fed, while 10Y yields in the Eurozone, UK and Japan remained largely unchanged.

- India Rates & Flows: The domestic 10Y ended at 6.53% after the RBI rejected all bids in the 2032 auction, leading to a sharp rally. Banking system liquidity is near neutral with overnight MIBOR in the 5.64–5.69% range. 1Y T-bill ~5.58%, 1Y CD ~6.40%, and spreads remain steady (AAA PSU at 44 bps, AAA NBFCs at 82 bps). FPIs were net buyers of USD 2.3 bn in Indian bonds in October.

Real Estate:

- Lighthouse Canton plans to invest $1.5B+ in India over the next few years, with $1B+ in private credit and $500M in real estate.

- A new India-focused private credit fund is expected by early 2026, highlighting rising global interest in India’s alternative investment space.

- Domestic family offices are diversifying real estate exposure—balancing direct property ownership with REITs and InvITs for better liquidity and tax efficiency.

- While REITs/InvITs face limited market depth and price discovery, their growing adoption signals a maturing real estate investment landscape.

IPOs:

- Groww IPO opens Nov 4, aiming to raise ~₹6,632 crore (₹1,060 crore fresh issue + ₹5,572 crore OFS) at a price band of ₹95–100 per share. Three SME IPOs also opening, keeping retail sentiment active.

- Shadowfax has filed for a confidential IPO of ₹2,000–2,500 crore, potentially valuing the logistics startup at ₹5,000–8,000 crore in the unlisted market.

- Valuation concerns resurface amid a busy IPO calendar, with Lenskart reportedly targeting a $6B+ valuation.

- Market takeaway: Strong investor appetite persists, but sustained post-listing performance will hinge on realistic pricing and earnings delivery

Private Equity & Venture Capital:

- Deal momentum rebounded: 39 PE/VC deals this week vs. 10 last week; total value steady at ~$1.17B.

- Top deal: General Atlantic’s $600M investment in PhonePe; other key raises included RMSI ($56M), Snabbit ($30M), and IntrCity ($28M).

- M&A steady: 8 deals led by Narayana Health’s $248M acquisition of Practice Plus Group Hospitals, alongside smaller buys by Godrej, DCM Shriram, Authum, and Dhampur Sugar Mills.

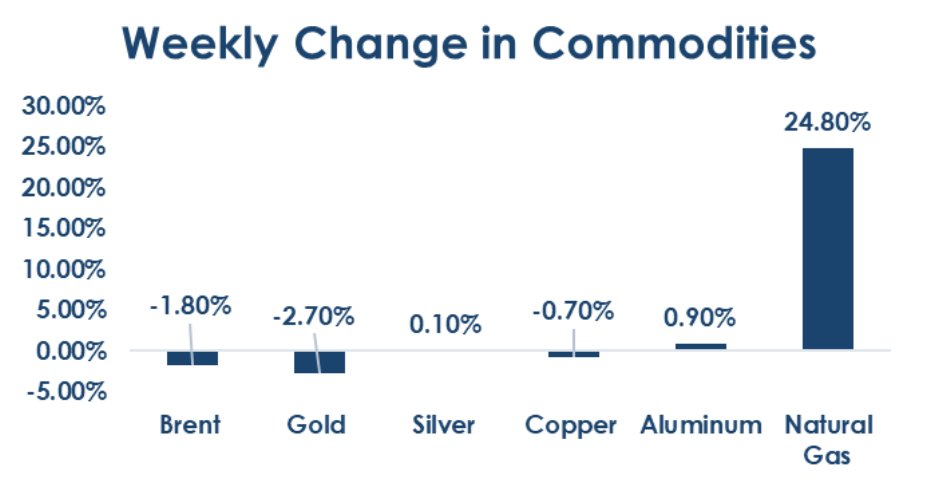

Commodities:

- Energy: Brent crude slipped 1.8% to $64.8, while US Natural Gas surged 24.8% to $4.12, indicating strong heating and power demand.

- Metals: Aluminum edged up 0.9% to $2,884, Copper dipped 0.7% to $10,887, and Gold fell 2.7% to $4,002, while Silver remained flat at $48.7.

- Precious metals sold off but recovered from lows on dips buying.

What’s New in the World of Wealth Management?

India’s wealth management space is witnessing a marked transformation, led by a surge in cross-border investing as affluent investors seek portfolio diversification and access to global growth opportunities. With rising awareness of international markets and greater digital accessibility, more Indians are looking beyond domestic equities to allocate funds into global indices, blue-chip stocks, ETFs, and even offshore private market opportunities. The Reserve Bank’s Liberalised Remittance Scheme (LRS) allows resident individuals to invest up to USD 250,000 annually in overseas assets, enabling them to buy shares directly on foreign exchanges, invest in international mutual funds or feeder funds offered by Indian AMCs, and explore alternative assets such as U.S. real estate or startup funds through global investment platforms. Wealth managers are increasingly facilitating these allocations by partnering with global brokers and fintech platforms that simplify access to international products.

At the same time, SEBI’s recent proposal to rationalize mutual fund fee structures, particularly through lowering the Total Expense Ratio (TER), reflects a broader effort to enhance transparency and cost efficiency across the wealth ecosystem. Lower TERs are expected to improve investor returns while compelling asset managers to prioritize performance, scale, and advisory quality. As a result, the wealth management industry is entering a phase of greater sophistication—marked by global diversification, competitive pricing, and stronger fiduciary standards—setting the stage for more democratized access to both domestic and international investment opportunities.

Our Views: What we Like?

Equities: Nifty50 is struggling to sustain above the 26000 mark. A strong positive trigger will likely be needed for it to surpass previous highs. We believe these are times for active sector allocation and stock selection. We are overweight on IT and Banks in our model portfolio.

Fixed Income: Yet again an uptick to 6.60% on the 10y failed and market quickly rallied. We have been sharing that 6.60% levels on 10y are attravtive to add duration to portfolio. Current 5y OIS are attravtive to pay for those looking to convert floating rate liabilities to fixed.

Commodities: We are bullish on Copper and Brent. US-China trade truce bodes well for commodities overall. We see consolidation in Precious metals but maintain a slightly bullish bias. There are many who have not been able to participate in the rally will be keen to buy on dips.

FX: We believe Dollar is rangebound overall against majors. We don’t see this week’s Dollar strength as a reversal. Market will test RBI’s resolve to defend the Rupee.