Billionz Multi-Asset Weekly Newsletter

Midcaps Outshine in Resilient Earnings; Commodities Stay Supported.

US Developments:

- Longest Government Shutdown: The U.S. government shutdown has now become the longest in history, stretching to 39 days.

- Data Release Impact: The October jobs report was not released due to the shutdown, shifting market focus to private labor indicators.

- Labor Market Weakness: The Challenger report showed a sharp rise in job cuts in October, dampening sentiment and raising December rate cut odds to 66%.

- Consumer Sentiment Drops: The University of Michigan Consumer Sentiment Index fell to 50.3, nearing its record low of 50 (June 2022).

- Trade Policy Developments: The U.S. Supreme Court expressed skepticism over Trump’s reciprocal tariffs, with key justices suggesting they may be legally untenable — a situation that warrants close monitoring.

Global Equities

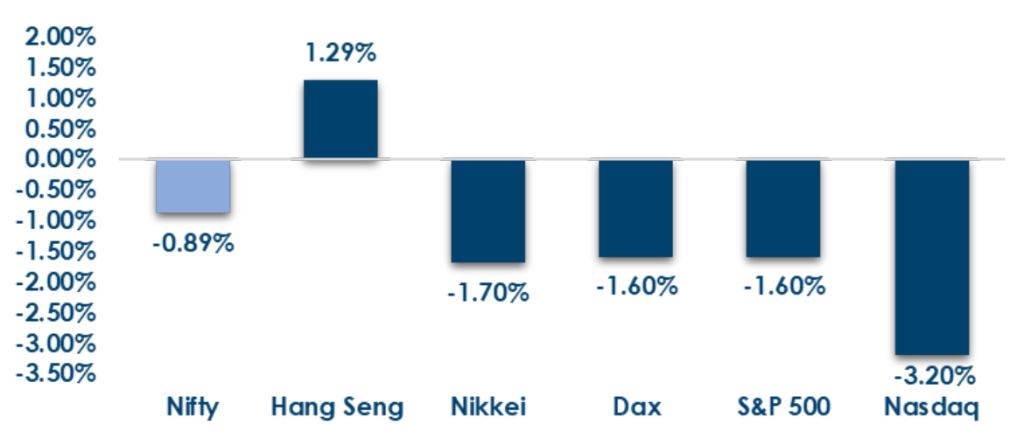

This is how Global Equities performed this week.

Domestic Equities :

- Global equities ended the week mixed, with major Western and Asian indices like the S&P 500, DAX, CAC, and Nikkei losing around 1.5–2% amid risk aversion, while Hang Seng, Jakarta, and Straits Times outperformed, posting gains of 1– 3% on regional resilience and bargain buying.

- Valuations across Indian equities remain elevated, with the Nifty50 trading at 23x trailing and 20.9x forward earnings, while Midcap100 and Smallcap250 indices command richer multiples of 33.1x/30.4x and 29.2x/27.9x, respectively— reflecting sustained optimism in the broader market despite stretched valuations.

- In terms of factors, Growth and Market Cap underperformed, while value did relatively well

- India VIX ended at 12.55 compared to the previous week’s close of 12.15

- FPIs have sold net USD 1.4bn of domestic equities in November so far

- FIIs remained net sellers for the second consecutive week with outflows of ₹1,633 crore, though slightly lower than the previous week’s ₹2,103 crore, while DIIs continued strong buying, pumping in ₹16,678 crore versus ₹18,804 crore a week earlier, providing key domestic support to markets.

- The week saw 3M India (+20.4%), CCL Products (+19.2%), and Hitachi Energy (+17.4%) emerge as top gainers, while Reliance Infrastructure (-18.6%), Reliance Power (-15.6%), and Netweb Technologies (-15%) led the losers’ pack amid sectoral rotation and profit booking.

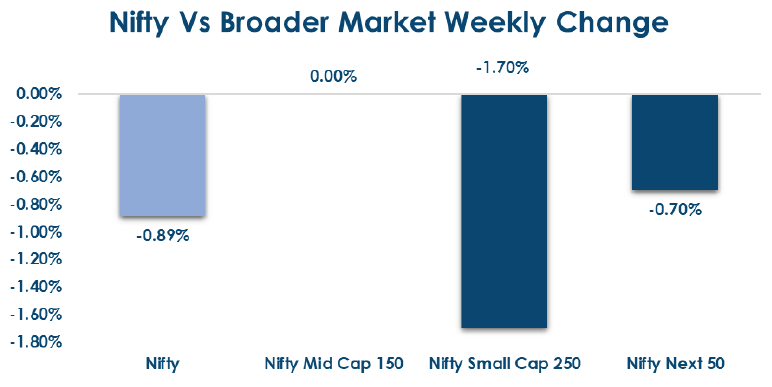

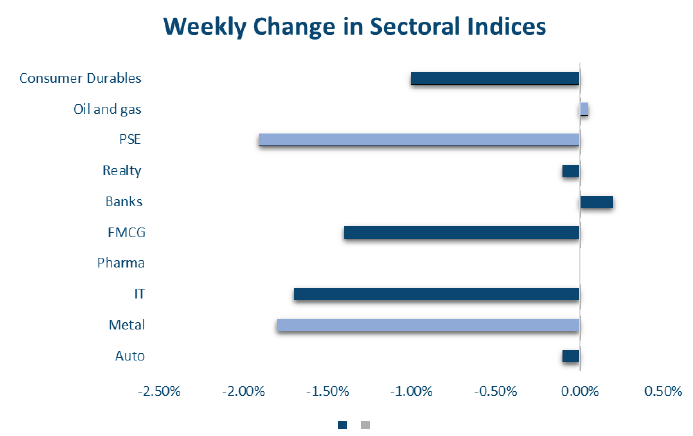

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices performed this week:

Fixed Income:

- Global Rates: Global bond markets were steady, with US 2-year and 10-year yields easing to 3.56% and 4.10%, while UK, Eurozone, Japan, and China yields remained largely unchanged.

- India Rates & Flows: The Indian 10-year yield stayed in a narrow 6.50–6.55% range with the new benchmark at 6.48%. Short-term rates edged higher, but call rates eased as liquidity turned ₹2 lakh crore surplus. 1-year Tbill stood at 5.56%, 1-year CD at 6.45–6.50%, while 10-year AAA PSU/NBFC spreads remained steady at 55bps/73bps. FPIs invested USD 100 million in bonds so far in November, reflecting steady foreign interest.

Real Estate:

- Institutional Capital Shift Needed: India’s real estate sector is calling for a transition from the traditional build-to-sell model to rental and lease-based formats to attract long-term institutional investors. Global players like Brookfield and Blackstone remain concentrated in commercial assets—offices, warehouses, hotels, malls, and data centres—through direct holdings and REITs.

- CapitaLand Expands in India: Temasek-backed CapitaLand plans to diversify its portfolio in the NCR while entering renewable energy, following its 21 MW solar plant in Tamil Nadu. The company is in talks to acquire multiple clean energy projects to build a scalable platform in India.

IPOs:

- India’s primary market remains vibrant, with three mainboard IPOs — PhysicsWallah, Emmvee Photovoltaic Power, and Tenneco Clean Air India — together targeting ₹9,000 crore, alongside two SME issues (Workmates Core2Cloud and Mahamaya Lifesciences), underscoring sustained fundraising momentum.

- The coming week also features high-profile listings like Lenskart, Groww, and Pine Labs, reflecting strong issuer confidence, broad-based investor participation, and robust demand across technology, energy, and manufacturing, supported by improving earnings and policy-driven capital formation.

Private Equity & Venture Capital:

- PE & VC activity slowed during the holiday-shortened week, with deal volume falling to 31 from 39, though investment value rose to $1.85 billion from $1.17 billion, marking the third straight week above $1 billion. The surge was driven by Brookfield India REIT’s $1.5 billion Ecoworld acquisition, which alone accounted for most of the total.

- M&A activity stayed subdued with seven small deals, including Cipla’s $12.5 million buyout of Inpera Healthsciences, Mitsubishi Corp’s minority stake in KIS Group’s Indonesia arm, and Omega Hospitals’ acquisition of Cytecare Hospitals in Bengaluru

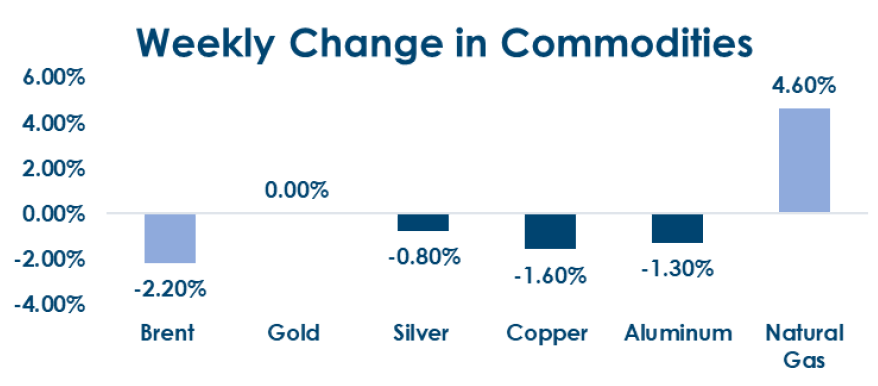

Commodities:

- Commodities traded mixed this week, with energy prices firming on gas gains while metals and crude saw mild declines, and gold stayed flat.

- Copper has retreated after printing highs above USD 11000 last week on Dollar strength post a hawkish Fed

- Dollar strength has weighed on precious metals as well.

What’s New in the World of Wealth Management?

SIFs have emerged as a dynamic addition to India’s wealth management landscape, offering fund managers the flexibility to pursue advanced strategies such as long–short equities, structured credit, and thematic or event-driven opportunities within a regulated framework. With fewer diversification constraints than mutual funds and a minimum investment threshold of ₹10 lakh, SIFs are designed to attract the mass affluent and emerging HNI segment. This structure bridges the gap between mutual funds and PMS offerings, providing investors access to institutional-grade, high-alpha strategies tailored to evolving risk-return preferences.

In parallel, India’s wealth ecosystem is witnessing a broader embrace of alternative investments by wealth managers and

family offices. Private credit, real assets, and startup investments are increasingly forming a key part of diversified portfolios as domestic capital becomes more sophisticated. The combination of regulatory innovation through SIFs and growing participation in alternative assets signals a structural shift toward a more advanced, diversified, and globally integrated wealth management environment.

Our Views: What we Like?

Equities: 25450 on Nifty50 is a crucial level. We had slipped below that, but the weekly close is above that level at 25492. A break above 25700 would be crucial to gain momentum on the upside. We may continue to see sideways price action for some time on the Nifty50. NSE 500 Earnings have been resilient in the Jul-Sep quarter. Midcap Earnings have been much better than large-cap and small-cap. Among sectoral indices, we are overweight on IT and Banks.

Fixed Income: We expect the yield on the 10y benchmark to trade in a 6.45-6.60% range. Any uptick towards 6.60% is a good level to add duration to the portfolio.

Commodities: We expect Gold and Silver to get bought on dips. There is still a lot of FOMO, and many have not participated in the rally and are waiting on the sidelines to enter. Base Metals may continue to remain supported and may inch higher with trade tensions ebbing a bit. Brent is likely to remain range-bound as slowdown concerns and tightening supply offset each other’s impact

FX: We have a slightly dovish bias on the Dollar against majors and are neutral on Dollar against EM currencies