Billionz Multi-Asset Weekly Newsletter

Valuations Ease, Momentum Builds: Nifty Set to Break Records?

US Developments:

- Trump signed the bill this week to end the longest government shutdown in history.

- Due to the unavailability of key economic data, the Fed may consider pausing in December to gain more clarity on labour market conditions and inflation trends.

- The probability of a Fed rate cut has dropped to 43% from 66%, weighing on risk sentiment.

- This shift led to higher US Treasury yields and a pullback in equities.

- The US overnight rate (SOFR) has risen above the upper bound of the Fed Funds rate range.

- This has sparked speculation that the Fed may eventually need to buy US Treasuries to inject reserves into the system

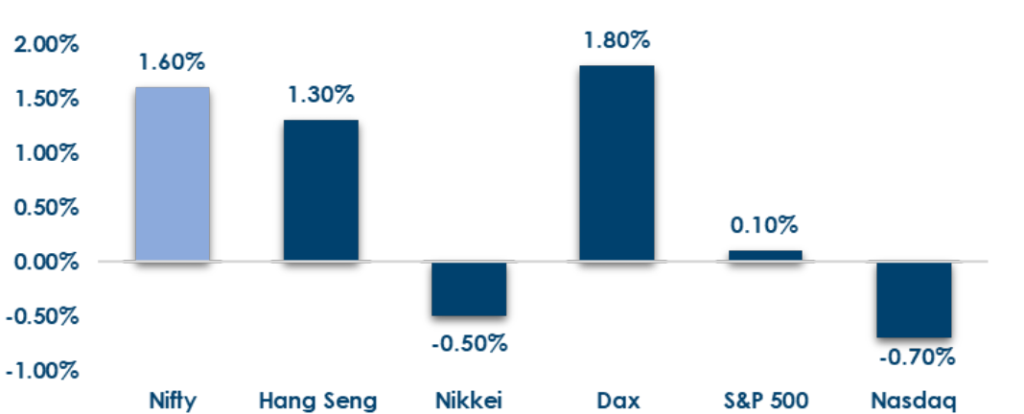

Global Equities

This is how Global Equities performed this week.

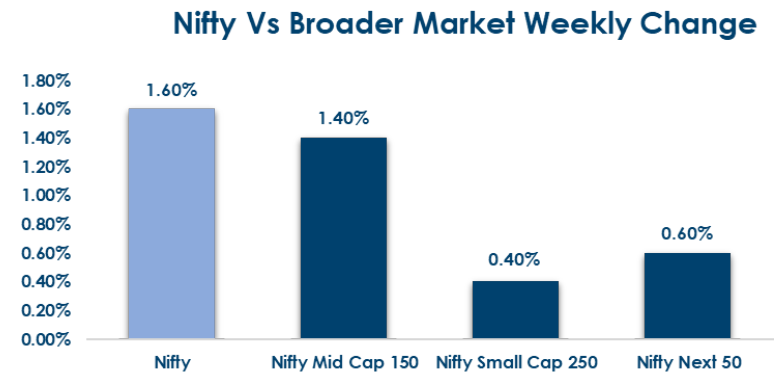

Domestic Equities

- Global equities were mixed this week, with modest gains in the S&P 500, FTSE, DAX, Hang Seng, Kospi, and Straits, a strong rise in France’s CAC, and declines across the Nikkei, Taiwan, and Jakarta indices.

- Equity valuations remain elevated across segments, with Nifty50 trading at 23.3x/21x (trailing/forward PE), Midcap100 at a richer 35.2x/29.2x, and Smallcap250 at 31.5x/26.7x—indicating broader market expensiveness despite expected earnings growth.

- All Nifty50 companies have reported Earnings for Q2FY26. Average Sales surprise has been 7.5% and Earnings surprise has been -3%

- In terms of factors, Earnings revision and liquidity outperformed, while Growth underperformed

- FPIs have sold net USD 700mn of domestic equities in November so far.

- FIIs sharply increased their selling this week (-₹12,020 Cr vs -₹1,633 Cr last week), while DIIs absorbed the pressure with significantly higher inflows (₹24,674 Cr vs ₹16,678 Cr).

- Market action was polarized with Tata Motors (+21.8%), Data Patterns (+18.5%), and Muthoot Finance (+15.3%) leading gains, while Transformers & Rectifiers (-18.8%), Cohance Lifescience (-13%), and Ola Electric (-9.2%) were the biggest drags.

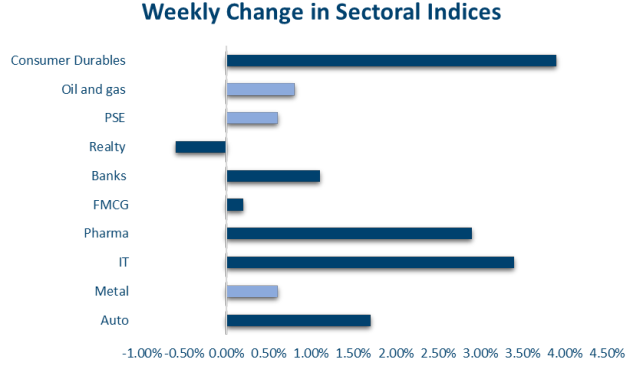

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices

performed this week:

Fixed Income:

- Global Rates: US yields edged up (2Y +2 bps to 3.61%, 10Y +3 bps to 4.15%) as markets grew uncertain about a December Fed rate cut. UK 10Y jumped 11 bps after the government decided against income-tax hikes, while Eurozone 10Y yields rose 2–6 bps.

- India Rates & Flows: The 10Y G-sec stayed in the 6.44– 6.50% range and closed at 6.49%; October CPI fell to 0.25% YoY due to base effects, keeping yield impact muted. OIS was steady (1Y at 5.47%, 5Y +3 bps to 5.74%), call rates hovered near 5.39% amid a ₹2 lakh crore liquidity surplus, and credit spreads were stable (AAA PSU ~48 bps, NBFC ~77 bps). FPIs have bought USD 700 million of bonds so far in November

Real Estate:

- Nexus REIT plans to aggressively expand its shopping centre portfolio, driven by strong mall footfalls and rising branded retail demand in both metros and smaller cities. With limited competition and growing spending power in emerging urban centres, developers see meaningful opportunities for new retail projects.

- India’s real estate sector has strengthened on the back of regulatory reforms, robust commercial real estate, and a revival in housing demand. With five listed REITs, rising warehousing activity, and greater institutional participation, the market is maturing—though structural gaps still remain.

IPOs:

- India’s primary market remains busy, with 74 IPOs raising about USD 10 bn so far this year versus 91 IPOs raising USD 18 bn last year. Despite the strong pipeline, the market isn’t euphoric — listing gains have varied sharply from –40% to +73%, averaging around 9%. Next week alone, large IPOs across ed-tech, clean energy, auto-tech, and pharma aim to raise over ₹10,000 crore.

- High activity and ample liquidity don’t guarantee returns. The wide divergence in listing performance reinforces the need for selective investing — focusing on pricing, fundamentals, and each IPO’s value proposition rather than chasing momentum.

Private Equity & Venture Capital:

- PE & VC activity stayed strong in terms of deal count, recording 34 transactions—the third straight week above 30. However, total deal value slumped to $369 million, an 80% drop from last week’s $1.8 billion peak, with only one large-ticket deal: Waaree Energy’s $113M+ fundraise led by Niveshaay.

- M&A remained muted with seven small transactions and no major value drivers; the largest disclosed deals were Entero Healthcare acquiring 80% of Bioaide Technologies and 51% of Anand Chemieutics, keeping overall transaction value subdued.

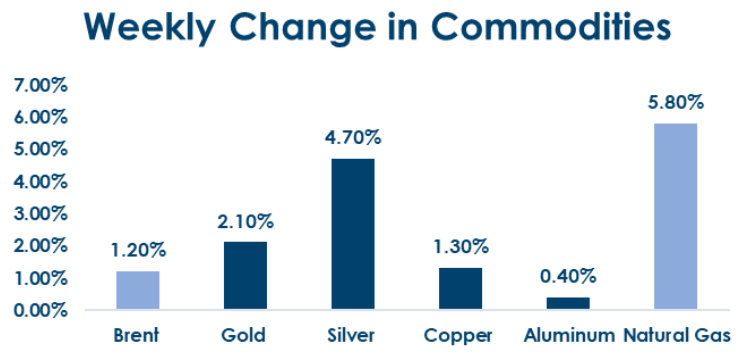

Commodities:

- Brent crude gained 1.2% this week to USD 64.4, US natural gas rose 5.8% to USD 4.6, LME aluminum inched up 0.4% to USD 2858, and LME copper climbed 1.3% to USD 10852.

- Gold ended the week 2.1% higher at USD 4084, after rising to USD 4245 intra-week before giving up gains.

- Silver gained 4.7% to USD 50.6, having briefly touched USD 53.6 but failing to sustain those levels.

- Base metals overall continued to move gradually higher

What’s New in the World of Wealth Management?

Fintech is radically transforming wealth management in India, making it much more accessible to everyday investors. Tools such as robo-advisors, AI-driven financial planning, mobile investing apps, and digital onboarding are no longer niche — they’re going mainstream. This democratization means investors with modest sums can now get sophisticated, goal-based advice that was once the preserve of HNI individuals.

At the same time, AI is increasingly driving core wealth-management functions. According to a market forecast, the global AI-powered wealth management solutions industry is poised for strong growth, with India projected to be one of the fastest-growing regions, experiencing a CAGR of ~15.9% through 2035. These AI tools help with smarter portfolio optimization, real-time risk analysis, and personalized advice — significantly reducing costs and improving operational efficiency.

Looking ahead, the blend of fintech and AI is reshaping how wealth managers operate: routine tasks are being automated, while human advisors are freed up to focus on higher-value strategic planning. As digital adoption deepens and AI models become more sophisticated, wealth-management firms in India will need to balance technology-led scale with personalized, trust-based relationships to stay competitive.

Our Views: What we Like?

Equities: We believe the Nifty50 seems poised to take out all-time highs. 1y forward valuations in Nifty50 and NSE500 look reasonable now. Midcaps are still overvalued in our view. Indian equities have underperformed year to date, and we expect them to play catch-up towards the end of the year. In terms of sectors, we are overweight in banks and IT.

Fixed Income: We believe current levels are attractive to add duration in US Treasuries, especially given the chatter around the inadequacy of Reserves and the need for the Fed to start buying Treasuries again. Domestic 10y yield is expected to trade sideways in the 6.40-6.60% band. Any uptick to 6.60% would be a good level to add duration to the portfolio. We believe there is value in buying SDLs (SGS) given the current spreads over Gsecs. We had recommended paying 5y OIS around 5.65% and that view seems to be coming off.

Commodities: We continue to remain constructive on base Metals and may see sideways price action in Brent for some time. Precious metals, in our view, are a buy on dips.

FX: Vols continue to remain very subdued. Rangish behavior is likely to continue heading into year-end. A bit of risk off could cause carry currencies to remain supported. 88.80 continues to remain the line in the sand as of now