Billionz Multi-Asset Weekly Newsletter

Valuations Moderate, Momentum Strengthens: Is Nifty Ready to Hit Fresh Records?

US Developments:

- Risk sentiment weakened earlier in the week as expectations of a December Fed rate cut faded. Risk sentiment weakened earlier in the week as expectations of a December Fed rate cut faded.

- Market participants trimmed bets following stronger data and cautious Fed communication.

- Sentiment reversed on Friday after Fed member Williams signalled room for a near-term rate cut amid softening labour market conditions.

- OIS-implied probability of a December cut fell to 35% before his remarks.

- Post-commentary, the probability jumped sharply to around 75% by week’s end.

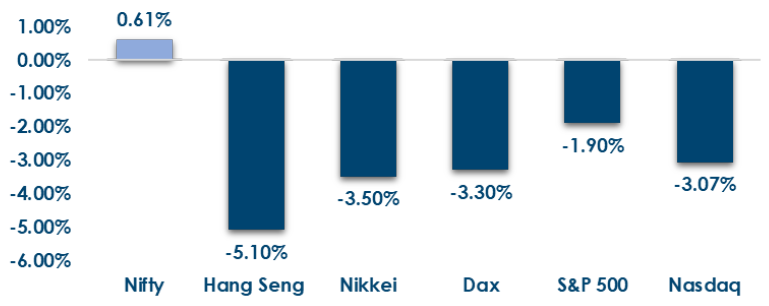

Global Equities:

This is how Global Equities performed this week.

Domestic Equities:

- Global equity markets broadly declined this week, with major Western and Asian indices registering sharp corrections, while only Indonesia managed to buck the trend.

- Benchmark index valuations currently stand at Nifty50: 21.6x TTM and 18.4x forward PE, Midcap100: 34.9x TTM and 24.0x forward PE, and Smallcap250: 31.0x TTM and 21.5x forward PE.

- Broader markets underperformed the Nifty50 significantly, even as the Nifty50 reached within striking distance of all-time highs.

- In terms of factors, low volatility and market cap outperformed this week

- FPIs have sold net USD 400mn of domestic Equities in November so far.

- FIIs saw a marginal outflow of ₹188 crore this week versus ₹12,020 crore last week, indicating stabilisation. DIIs remained strong buyers, pumping in ₹12,969 crore, though lower than the ₹24,674 crore inflow in the previous week.

- Top gainers were Narayana Hrudayalaya (+16.5%), Jaiprakash Power Venture (+12.7%), and Mahindra & Mahindra (+11%). Top losers included HBL Engineering (-13.9%), Gujarat Mineral Development (-13.9%), and Godawari Power Ispat (-12.7%).

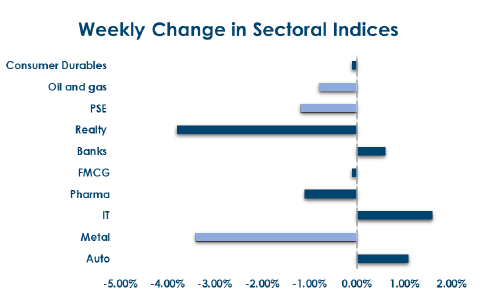

Below are the graphical representations of how key benchmark indices performed this week & how sectoral indices

performed this week:

Fixed Income:

- Global Rates: US 2Y Treasury yield fell 10 bps to 3.51%, while the US 10Y yield dropped 8 bps to 4.06% this week. Eurozone and UK 10Y yields were broadly stable, moving between -1 to +2 bps. Japan’s 10Y JGB yield rose 4 bps to 1.77%, marking its highest level since 2007.

- India Rates & Flows: Domestic 10Y traded in the 6.47– 6.52% range, ending at 6.52% with a 4 bps spike on Friday. 1Y OIS stayed flat at 5.475%, while 5Y OIS rose to 5.77%; overnight MIBOR was 5.43–5.59%. Liquidity remains in ~₹1.75 lakh cr surplus. Credit spreads: 10Y AAA PSU ~43 bps, AAA NBFC ~73 bps. Short-term rates: 1Y T-bill 5.55%, 1Y CD 6.39%. FPIs bought ~USD 600 mn of domestic debt in November so far.

Real Estate:

- SEBI is considering expanding the liquid MF investments allowed for REITs and InvITs and pushing for their inclusion in major indices. It is also coordinating with IRDAI, PFRDA and EPFO to boost institutional participation, building on moves to allow foreign investors and QIBs as strategic investors to strengthen capital flows.

- CapitaLand India Trust’s 4.6-million-sq-ft International Tech Park in Chennai has drawn strong interest as it moves toward divestment, with Embassy REIT and Mindspace REIT evaluating the asset—signalling continued demand for high-quality, income-generating office spaces.

IPOs:

- Next week’s IPO activity is concentrated in the SME segment, with no mainboard launches. Three issues— SSMD Agrotech India, Mother Nutri Foods, and KK Silk Mills—will open for subscription, while Excelsoft Technologies, Sudeep Pharma, and Gallard Steel are set to list, signalling a muted week for large-cap IPOs.

- SSMD Agrotech India (₹114–₹121) will expand food processing and dark store ops; Mother Nutri Foods (₹111– ₹117) is funding a new facility; and KK Silk Mills (₹36– ₹38) plans machinery upgrades and debt reduction. Meanwhile, several retail-heavy IPOs have dropped up to 36% post-listing, highlighting rising risks for momentum-driven investors.

Private Equity & Venture Capital:

- Private equity and venture capital activity slowed to 27 deals from 34, but investments still crossed $1.2B. The week was led by TPG’s $1B commitment to its AI data-centre JV with TCS HyperVault, driving deal value past the $1B mark for the fourth time in five weeks.

- M&A activity remained muted with three deals versus six previously. The biggest was Nuvoco Vistas Corp’s acquisition of Vadraj Energy, a JSW Cement and Alpha Alternatives-owned power generation asset, aimed at boosting captive power capacity for its cement operations

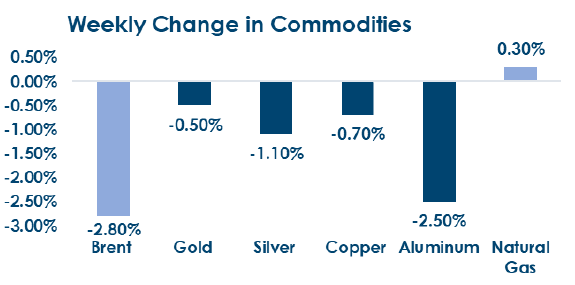

Commodities:

Major commodities posted a broadly softer performance this week, with energy showing mixed moves while base and precious metals largely trended lower, signalling continued caution across global commodity markets.

The US pushing ahead with the Russia-Ukraine peace plan weighed on Brent.

Overall, a stronger Dollar weighed on commodities in general this week.

What’s New in the World of Wealth Management?

The private-wealth advisory landscape is poised for robust expansion, with the global private wealth management services market projected to grow at a 10.6% CAGR between 2025 and 2035. The report highlights how rising HNI/UHNI populations are increasingly turning to structured advisory models that combine digital platforms, cross-border services, and multi-asset portfolio strategies. Wealth managers are stepping up their offerings with enhanced asset-allocation tools, estate and tax planning, and alternative investments to meet the evolving needs of affluent clients.

Domestically, India’s alternative-investment ecosystem is witnessing a significant shift: combined assets under management for PMS and AIFs have crossed ₹23.43 lakh crore, after growing at a staggering 31.24% CAGR over the past decade. This surge reflects a clear move among wealthy investors toward high-conviction, alpha-seeking strategies via PMS and AIFs, signaling the rise of alternatives as a core component in modern wealth-management portfolios.

Our Views: What we Like?

Equities: While benchmark Nifty50 reached within striking distance of all-time highs, Broader markets are underperforming. Breadth indicators are a bit of a concern. Therefore, we prefer sticking to the large-cap universe to express our long view. We believe large Caps are fairly valued, considering 1y forward PE levels. Among sectors, we continue to remain upbeat on banks and IT.

Fixed Income: We expect the yield on the domestic 10y benchmark to trade in a 6.45-6.60% range. Any uptick towards 6.60% is a good opportunity to add duration to the portfolio. We had been highlighting that paying 5y OIS around 5.65% was attractive. It has moved higher to 5.77%. Around 5.85-5.90% would be good levels to exit.

Commodities: We continue to be buyers of precious Metals on dips. We are also upbeat on Base Metals. Brent is likely to continue to remain range-bound in USD 58-70 in our view.

FX: Broad Dollar continues to remain in a range. We are close to the lower end of the range in EUR, GBP, and AUD. However, we expect ranges to hold into year-end. RBI likely gave up the defence of 88.80, considering broad Dollar strength and the fact that it was already short substantially in forwards.