Billionz Multi-Asset Weekly Newsletter

Record Highs, Selective Bets: Large Caps Lead the Market Narrative

US Developments:

- India’s Q2 GDP surprised on the upside at 8.2% YoY (vs. 7.4% consensus), with GVA at 8.1% YoY and Nominal GDP at 8.7% YoY.

- On the expenditure side, strong private consumption and private capex drove growth, offsetting weaker government spending and the drag from imports.

- Strong private consumption and private capex supported overall growth. This offset weaker government spending and the import drag.

- Robust manufacturing activity and electricity generation lifted Q2 performance.

- Some market participants expect a 25 bps rate cut. Strong GDP data + INR pressure may give the RBI reason to wait and hold. However, with low inflation (below the 2–6% mandate), the RBI may still choose to deliver one last rate cut to support growth.

- India’s exchange rate regime has been reclassified to “crawl-like” from “stabilised” due to higher FX volatility.

Global Equities:

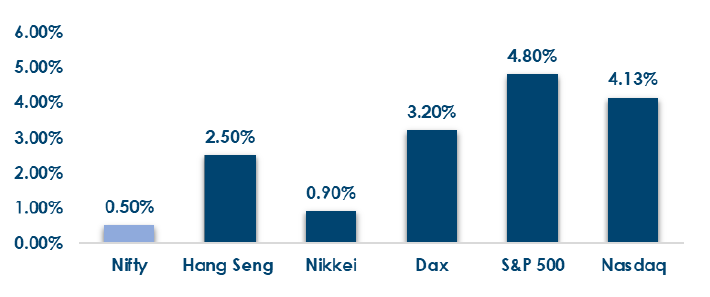

This is how Global Equities performed this week.

Domestic Equities:

- Global equities rallied strongly this week, with major indices across the US, Europe, and Asia posting broad-based gains led by the S&P 500’s standout 4.8% surge.

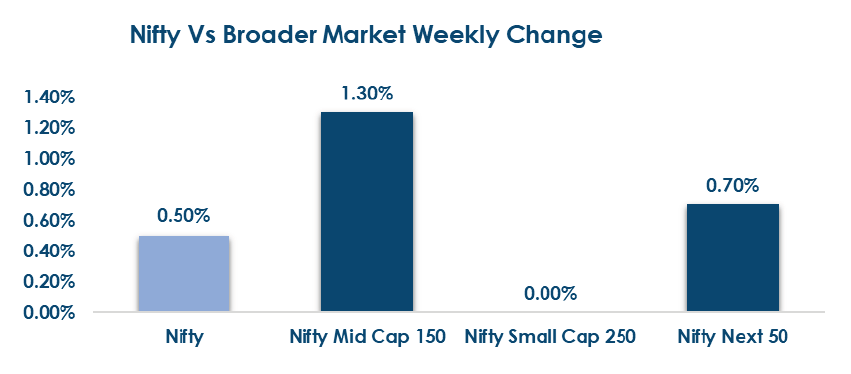

- Nifty50 printed all-time highs on Thursday. However, the volume and breadth indicators are weaker compared to what they were during highs in September ’24.

- Valuations remain elevated down the market-cap curve, with Nifty50 at a reasonable ~21x PE while Midcap100 (~35x → 29x) and Smallcap250 (~31x → 26x) continue to trade at a premium even on a forward basis

- YTD in terms of factors, value and low volatility have outperformed, while growth and momentum have underperformed

- FPIs sold net USD 425mn of domestic Equities in November

- FIIs turned heavy sellers this week with net outflows of ₹3,659 crore, while DIIs strongly supported the market with a robust ₹22,763 crore of inflows—far higher than last week’s ₹12,969 crore.

- Weekly Gainers: Gujarat Mineral Development (+10.3%), Aditya Birla Capital (+10%), and Ashok Leyland (+9.3%) topped the charts, while Weekly Losers: Transformers & Rectifiers (-11.1%), Chennai Petroleum (-10.6%), and Whirlpool of India (-9.2%) lagged

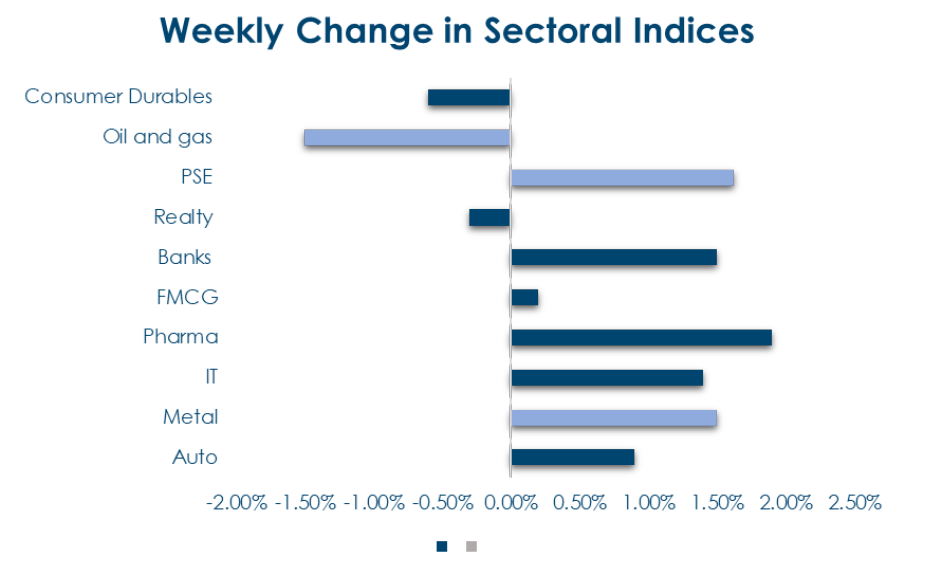

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices

performed this week:

Fixed Income:

- Global Rates: US 10y yield slipped 1bp to 4.01%, while the 2y was steady at 3.49%; UK 10y fell sharply by 10bps on a balanced budget, and France & Italy 10y yields eased ~4bps, whereas Japan’s 10y rose 3bps to 1.80%.

- India Rates & Flows: India’s 10y moved slightly higher to 6.51% post a strong GDP print, with rate-cut hopes fading; 1y and 5y OIS spiked 3bps and 6bps to 5.43% and 5.76%, liquidity remained in ₹1 lakh+ crore surplus, AAA PSU/NBFC spreads held at 55bps/87bps, and FPIs bought USD 700mn in domestic debt for November.

Real Estate:

- Real estate momentum is accelerating with HDFC Capital and Hero Realty launching a ₹1,000 crore platform focused on mid-income housing in Tier 1 & 2 cities, driven by strong demand from better infrastructure, improved affordability, and expanding urban migration

- NovumLake Partners completed the third close of its maiden ₹1,000 crore AIF at ₹414 crore, targeting distressed and value-add commercial assets in Mumbai and Bengaluru through a buy-fix-sell strategy, reflecting rising institutional interest in structured real estate plays.

IPOs:

- The primary market gears up for a heavy week with three IPOs — Meesho, Aequs, and Vidya Wires — set to open between Dec 3–5, collectively aiming to raise ~₹6,900 crore amid strong investor interest and active

- grey-market signals.

- While recent listings have largely delivered gains, the surge in new supply makes selectivity key — with valuations, subscription quality, and underlying business fundamentals likely to drive differentiated performance across these offerings.

Private Equity & Venture Capital:

- Deal momentum was mixed this week—volumes rose from 27 to 32, but funding plunged to $254.6M from $1.2B, with the final figure likely to rise once details of an undisclosed KKR–PSP Investments deal are released. Key transactions included KKR increasing its stake in Lighthouse Learning alongside PSP, plus mid-sized investments in Rippir (SBI), Ace International (FMO), Square Yards (Smile Gate), and Neo Group (Artha Group).

- M&A activity strengthened with five deals, including a major headline transaction where CPPIB and IndoSpace acquired six industrial and logistics parks worth ~$336M through their IndoSpace Core JV.

Commodities:

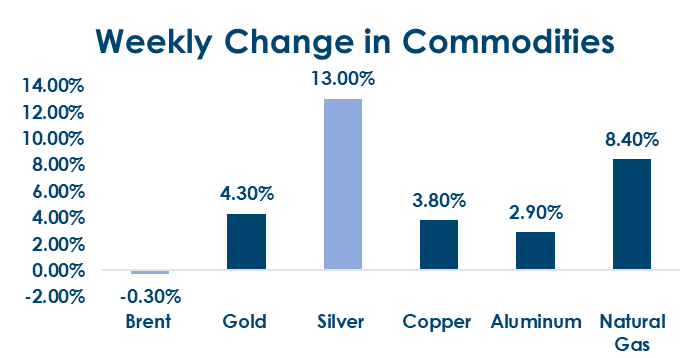

Commodities saw mixed moves, with energy softening and metals surging — Brent dipped 0.3% while US Natural Gas jumped 8.4%, and industrial/precious metals rallied sharply (Aluminium +2.9%, Copper +3.8%, Gold +4.3%, Silver +13%).

Disruptions due to an outage in CME pushed Silver to new highs amid low Black Friday volumes. Silver inventories in China have fallen to the lowest level in 10 years following large shipments to London triggered by a supply squeeze. Copper surge was driven mainly by concerns over supply expressed at a miners, traders, and smelters meet in Shanghai

What’s New in the World of Wealth Management?

India’s wealth-management landscape is undergoing a rapid transformation driven by rising private wealth creation and a growing preference for structured financial planning. One of the most notable shifts is the institutionalisation of family offices, which are now moving beyond informal wealth oversight toward governance-led, professionally managed structures. With increasing intergenerational wealth transfer and greater exposure to global investment frameworks, ultra-high-net-worth families are prioritising formal asset allocation, succession planning, and risk-managed investing rather than ad-hoc or promoter-centric financial decisions.

Alongside this structural evolution, technology continues to reshape the advisory model. Wealth managers are increasingly leveraging AI-driven portfolio analytics, digital reporting frameworks, and hybrid advisory models to enhance personalisation, transparency, and operational efficiency. As the market scales, the focus is shifting from transactional wealth products to holistic financial stewardship — spanning public markets, private equity, alternatives, estate planning, and philanthropy. India remains one of the fastest-growing global wealth hubs, and the coming phase is expected to be defined by advisory depth, digital capability, and the ability to balance human judgment with technology-enabled insights

Our Views: What we Like?

Equities: Nifty50 hit record highs, but broader markets have not participated. The market is therefore cautious and prefers to stick to quality and large Caps. We hold a similar view but have a preference in terms of sectors. Large-cap names in banking and IT are looking attractive from a long-term portfolio construction perspective.

Fixed Income: Ranges continue to hold on 10y benchmark. 6.45-6.60% is what we have been trading in. Any uptick towards 6.60% is a good opportunity to add duration to the portfolio. Paying 5y OIS on dips has worked well. One can look to exit on uptick to 5.85-5.90%

Commodities: We have been bullish on precious metals and continue to remain so. However, we may see short-term corrections given the run-up. Base metals are also likely to trend higher amid a weak Dollar environment gradually.

FX: Ranges continue to hold in EUR, GBP, and AUD and are likely to hold into year-end. Yen continues to remain under pressure. BoJ jawboning may have put a cap around 158 for now. Rupee continues to underperform. The market is clearly wanting to position long USD. RBI’s resolve will be tested