Billionz Multi-Asset Weekly Newsletter

Nifty’s Uptrend Resumes: Time for Quality, Value & Large Caps?

Weekly Developments:

- RBI cut the repo rate by 25 bps to 5.25% (unanimous vote); stance maintained as neutral.

- One MPC member voted to shift stance to accommodative.

- OMO purchase of ₹1 lakh crore announced for December to inject liquidity.

- USD 5 bn Buy-Sell swap (3-year tenor) scheduled for December, adding ₹45,000 crore liquidity.

- Growth remains RBI’s priority amid benign headline and core inflation.

- The buy-sell swap indicates that the RBI is offsetting spot USD sales used earlier to curb rupee depreciation.

- Ample liquidity is expected to aid policy transmission.

- Upcoming focus: US Fed policy; 25 bps rate cut widely expected.

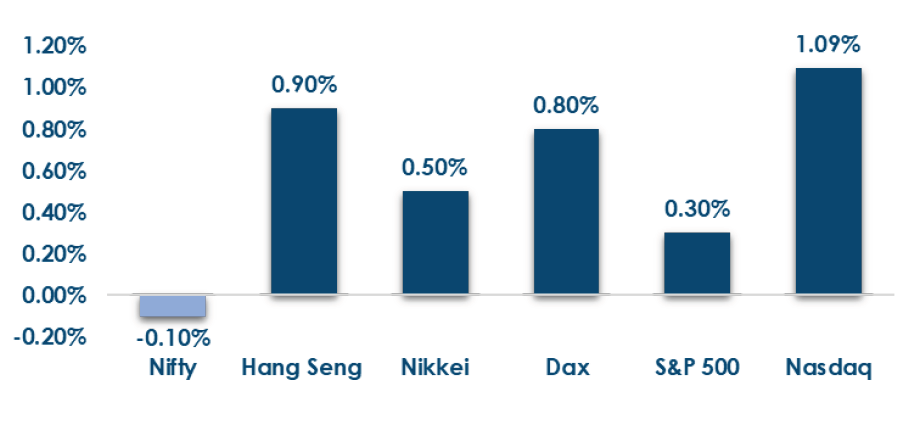

Global Equities:

This is how Global Equities performed this week.

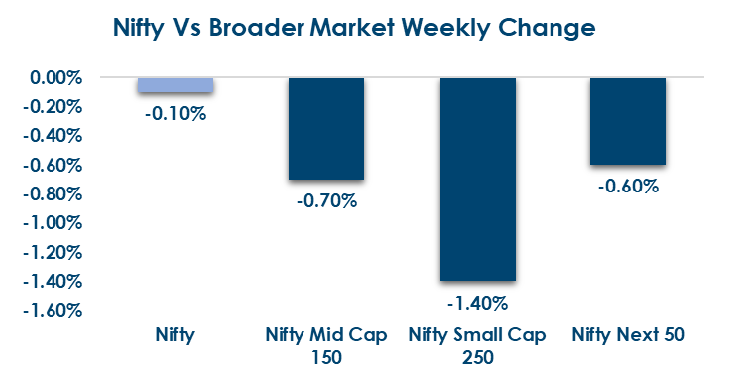

Domestic Equities:

- Global equities saw a mixed week. US and European markets were largely flat to mildly positive, with the S&P 500 up 0.3% and the DAX leading gains at 0.8%, while the FTSE slipped 0.6%.

- In Asia, performance was stronger — the Kospi surged 4.4%, Jakarta gained 1.5%, and Hong Kong’s Hang Seng rose 0.9%, reflecting improved regional sentiment.

- Domestic equity markets cheered the RBI’s pro-growth stance.

- Valuations remain elevated across the board, with the Nifty 50 trading at 21.6x TTM and 21.3x forward earnings, while midcaps are costlier at 35.1x and 29.3x, and smallcaps at 30.7x and 26.2x, showing only modest easing on a forward PE basis.

- In terms of factors, value, growth and momentum underperformed while Quality and high dividend stocks outperformed.

- FIIs saw sharper outflows this week at ₹5,252 crore versus ₹3,659 crore last week, while DIIs continued to support the market with strong inflows of ₹11,394 crore compared to ₹22,763 crore previously.

- Birlasoft (+13.8%), Hindustan Copper (+13.7%), and ZF Commercial Vehicle (+12%) led the week’s gains, while Kaynes Technology (-20.7%), Ola Electric (-13.9%), and Transformers & Rectifiers (-12.6%) were the top laggards

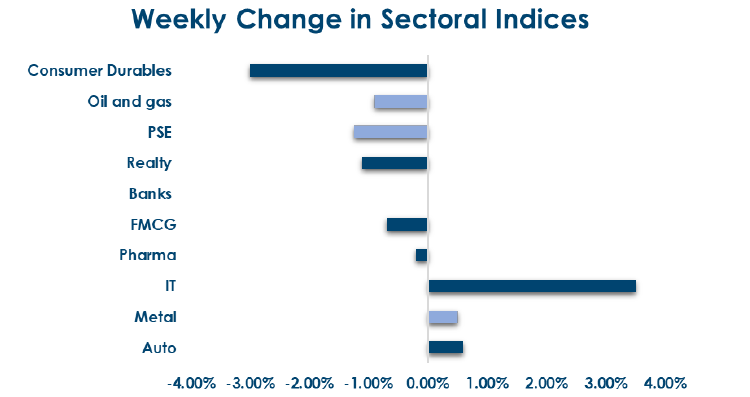

Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices

performed this week:

Fixed Income:

- Global Rates: US 2Y/10Y yields inched up by 3bps and 5bps to 3.56% and 4.13%, Eurozone 10Y yields rose 2–4bps, and Japan’s 10Y JGB climbed 8bps to 1.93%.

- India Rates & Flows: The 10Y G-sec traded within 6.45– 6.54% and closed at 6.50%, with the initial OMO-driven dip quickly reversing; RBI clarified it will exclude SDLs from OMO purchases. OIS saw mixed moves with 1Y down 3bps (5.43%) and 5Y up 3bps (5.79%), liquidity remained in a surplus above ₹2 lakh crore, and credit spreads stood at 50bps for 10Y AAA PSU and 85bps for 10Y NBFC.

Real Estate:

- Alternative Real Estate Funding: Funding momentum is rising in the fractional real estate space, with Micro Mitti now in advanced talks to raise ₹150–200 crore after its earlier ₹90 crore round, as family offices and venture funds show growing appetite for project-level SPV structures.

- REIT Market Evolution: India’s REIT market is maturing but still shallow, with five REITs valued at over $18 billion yet representing just 0.2% of market cap and 330,000 unitholders; improving awareness and liquidity should drive wider participation.

IPOs:

- Primary market activity is strong, with four mainboard IPOs — Nephrocare, Park Medi World, Wakefit Innovations, and Corona Remedies — opening this week to raise about ₹3,735 crore, alongside upcoming listings of Meesho, Aequs, and Vidya Wires and active SME issues.

- Market attention is centred on ICICI Prudential AMC’s upcoming ₹10,700-crore IPO, one of 2025’s largest, reinforcing a record year where mainboard IPOs have crossed 100 issues and total fundraises are set to exceed ₹1.7 trillion, offering investors diverse opportunities across market segments.

Private Equity & Venture Capital:

- PE/VC Activity: Deal volumes softened in early December, but total funding jumped to $589 million across 18 deals—more than double last week’s $255 million—driven primarily by KKR’s $322 million investment in National Highways Infrastructure Trust, which contributed over half the total.

- M&A remained robust with 12 deals, well above typical levels, led by large strategic transactions such as JSW Steel’s $2.72 billion restructuring of Bhushan Power & Steel with JFE Steel and Shriram Pistons & Rings’ acquisition of three Indian units of Grupo Antolin.

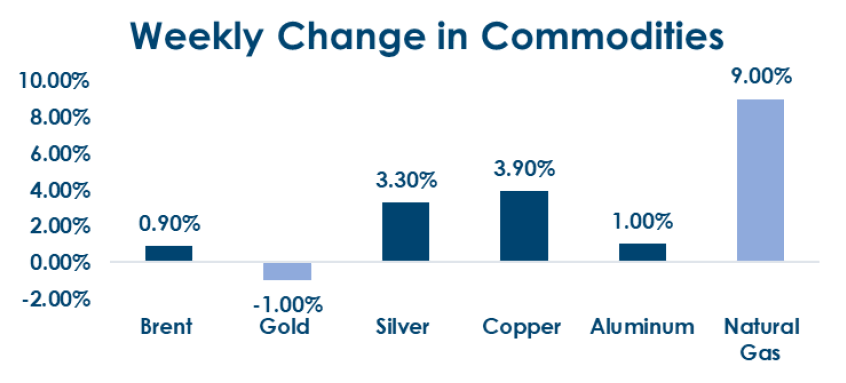

Commodities:

- Major commodities saw mixed movement this week, with Brent (+0.9%), natural gas (+9%), aluminium (+1%), copper (+3.9%), and silver (+3.3%) gaining, while gold dipped (-1%).

- Silver and Copper continue to rally. Weak Dollar and Fed cut expectations are helping the commodity complex.

What’s New in the World of Wealth Management?

The recent cut in the RBI’s repo rate to 5.25% has reignited optimism in rate-sensitive sectors and boosted overall market sentiment. This easing is seen as supportive for credit growth, corporate earnings, and borrowing costs, which could propel demand across equities and fixed income — making it a favourable environment for both debt- and equity-linked investments. At the same time, global uncertainty and shifting macro signals have injected volatility into capital flows, prompting investors to recalibrate exposure and favour value, yield-oriented assets.

Another important shift: global institutions are increasingly eyeing India as a destination for equity investment. For example, Sberbank has launched a new mutual fund — “First-India” — linked to the NIFTY 50, offering Russian retail investors direct access to India’s equity market. Such cross-border engagement, alongside ongoing regulatory efforts to simplify foreign investor access and streamline global capital flows, may mark a turning point — motivating long-term international inflows, enhancing liquidity, and bolstering transparency in India’s capital markets.

Our Views: What we Like?

Equities: Yesterday’s price action is quite encouraging and gives us conviction that the Nifty50 is on course to trend higher. Value and Quality could outperform growth and momentum. We favour adding quality large caps from a long-term horizon perspective. In terms of sectors, we prefer being overweight on IT and Banks, especially large caps.

Fixed Income: Yield on the benchmark 10y is likely to continue trading in the 6.45-6.60% range. 10y SDLs and NBFC papers are offering attractive yield pick up. 5y OIS is likely to trade a 5.65-5.85% range broadly, with moves to either side giving a good trading opportunity.

Commodities: We expect base metals to continue to rally on a weaker Dollar and amid positive risk sentiment. Gold may see some profit-taking, while momentum in Silver will likely push it higher to new all-time highs. Brent is likely to trade sideways in the USD 58.5-65.5 per barrel range.

FX: We believe the Fed policy will be the last major trigger for the year. After that, the liquidity will start thinning out till year end. The dollar is likely to continue trading with a weakening bias against majors.