Multi-Asset Weekly Newsletter

Global Development

Nifty rises for 3rd straight week, India volatility index drops to an all-time low.

The Fed cut rates along expected lines by 25 basis points and indicated a cut at each of the remaining two Fed meetings for the year. Expectations of Fed cuts are keeping the risk sentiment afloat. US PCE data for August, due on Friday, will be the key data to look forward to next week. BoE and BoJ kept rates unchanged. The Bank of Canada cut rates 25 basis points to shield the economy from the impact of Trump’s trade tariffs. President Trump said that he had a productive phone call with Chinese President Xi. The two are due to meet in November. India-US trade talks are back on track, and the chief economic advisor expressed optimism, saying trade issues could be resolved in 8-10 weeks.

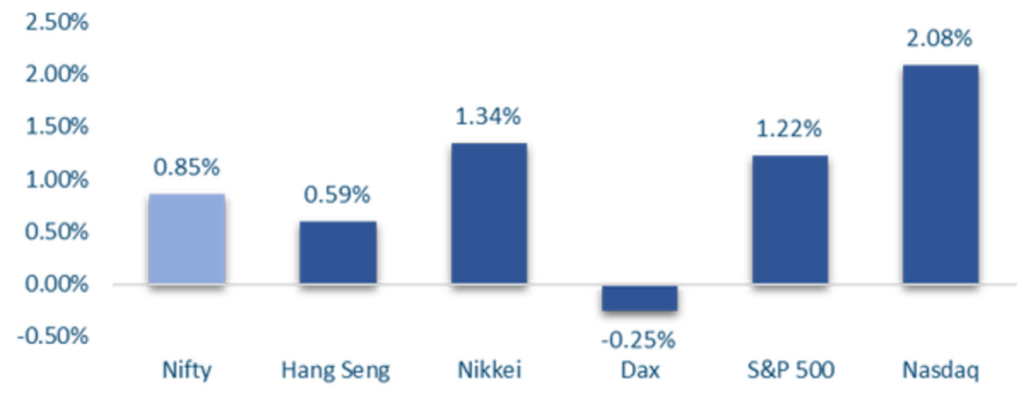

Global Equities

This is how Global Equities performed this week.

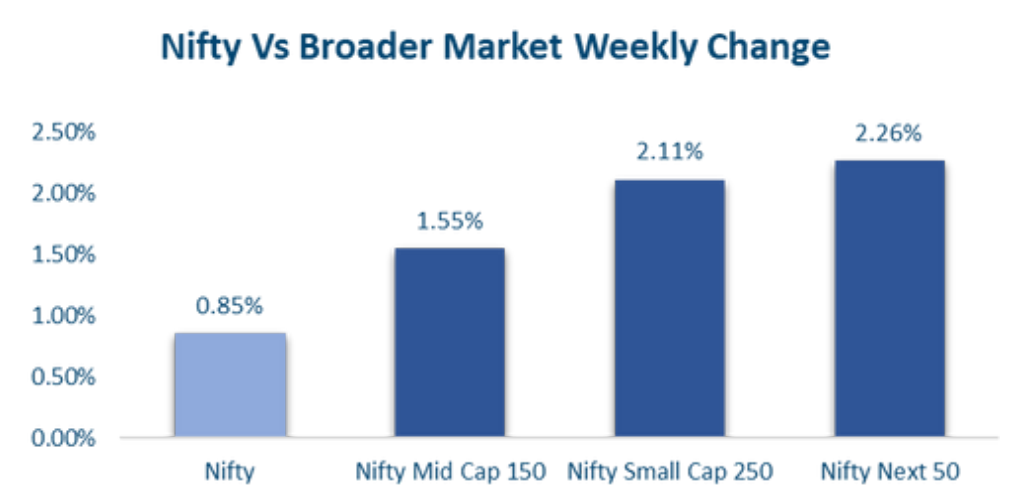

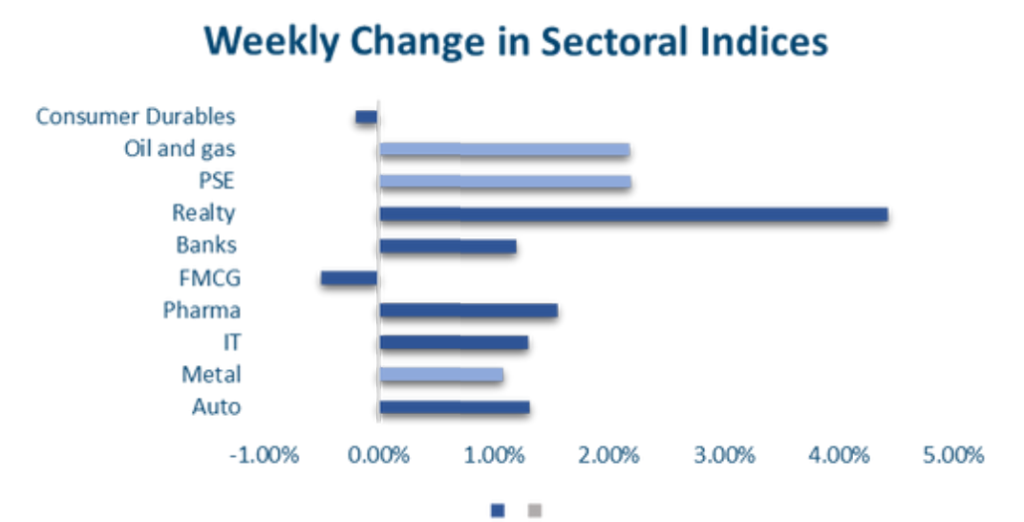

Domestic Equities

Valuations across key indices remain elevated. On a trailing/forward 12m EPS basis, Nifty50 trades at 22.5/21.4, Midcap100 at 32.9/28.2, and Smallcap250 at 29.8/27.6. This highlights richer multiples in mid and small caps versus large caps. In terms of factors, low volatility and quality underperformed growth and momentum, a sign of risk returning to markets. FPIs have pulled out USD 900mn from domestic Equities in September so far. This is the third consecutive month of outflows. India VIX at 9.97 is at an all-time low. The FIIs saw outflows of ₹203 Cr this week vs ₹3,579 Cr last week, while DIIs infused ₹8,884 Cr. Top gainers were Intense Tech (+43.5%), Banco Products (+35.2%), and Redington (+22.9%); losers included Dreamfolk (-14.7%), Balmerlawrie (-11.7%), and KRBL (-11%). Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices performed this week:

Fixed Income

US 2y yield rose 3bps this week to 3.57% while US 10y yield rose 9bps to 4.13% this week.

10y Yields across the UK and the Eurozone were up 5-8bps this week. Japan 10y rose 5bps to 1.63%. Yield on the domestic 10y benchmark traded a 6.47-6.53% range this week and ended at 6.49%, unchanged from last week. 1y OIS ended 2bps lower at 5.45% while 5y OIS ended 2bps higher at 5.71%

Surplus liquidity in the Banking system has come off on advance tax outflows. This pushed overnight call fixings to 5.58-5.60% over the last couple of days. 1y t-bill is around 5.56% and 1y PSU CD is around 6.30%. Spread of 10y AAA PSU and NBFC over Gsec is 56bps and 78bps, respectively. FPIs have invested net USD 1.2bn in domestic debt in September so far.

IPOs

India’s IPO market is getting ready for a surge, with 174 companies reportedly lining up to raise around ₹2.84 trillion. While investor caution remains, the volume of intended IPOs underscores how many firms are looking to tap public markets soon.

In the coming week alone, there are 25 new issues set to open—nine in the mainboard segment targeting roughly ₹5,464 crore, and sixteen SME IPOs making up the rest of a combined ₹6,300-odd crore fundraising. Among the names in the spotlight are Atlanta Electricals, Ganesh Consumer Products, Seshaasai Technologies, Jaro Institute, Solarworld, Anand Rathi, Epack Prefab Technologies, Jain Resource Recycling, and Jinkushal Industries.

This busy pipeline suggests that despite market headwinds, companies are pushing forward with public offerings. For investors, this means both opportunity (diversified sectors, fresh businesses) and increased diligence, especially around valuation, business fundamentals, and subscription interest.

Private Equity & Venture Capital

Private equity and venture capital activity slowed this week, with deal count slipping to 21 from 29 and disclosed value falling nearly a third to $242 million from $363 million. Infra.Market and FinBox together accounted for over half of the week’s total fundraising.

IPO-bound Infra.Market raised a Series G round led by Nikhil Kamath-backed NKSquared, with participation from Accel India, Nexus Venture Partners, Tiger Global, Evolvence India Fund, and its co-founders. The transaction valued the company at $2.8 billion (₹24,600 crore), making it the week’s standout deal.

Mergers and acquisitions remained steady, with 12 transactions recorded, up from nine last week. Key highlights included JSW Neo Energy’s ₹1,728 crore ($196 million) acquisition of Tidong Power, IFC’s ₹1,254 crore ($142 million) exit from Apollo Health, and TCC Concept signing a term sheet to acquire a controlling stake in Pepperfry.

Real Estate

BlackRock has signed a lease for over 400,000 sq. ft. of office space in Bengaluru, one of the city’s largest flexible workspace deals this year. Valued at around ₹350–400 crore over the lease term, it highlights strong demand for premium office assets, with Bengaluru’s Grade-A absorption already crossing 10 million sq. ft. in 2025.

Meanwhile, Brookfield Asset Management has raised its stake in Mumbai’s Nirlon Ltd to nearly 10% after additional purchases of about ₹84–89 crore this year, on top of its earlier ₹400 crore commitment. With over 55 million sq. ft. of assets under management in India, Brookfield’s move underscores continued institutional confidence in the country’s commercial real estate market.

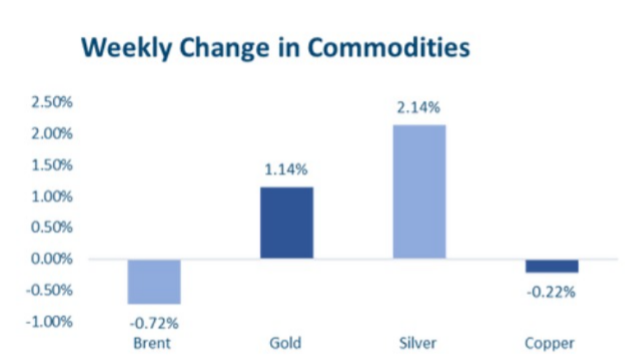

Commodities

Expectations of a supply glut are keeping crude prices under pressure.

Precious metals continue to see positive traction.

Base Metals failed through on last week’s positive

price action.

Adjacent is how major global commodities

moved this week:

What’s New in the World of Wealth Management?

Recent regulatory changes are significantly enhancing the landscape of wealth management in India. SEBI’s relaxation of IPO rules, including greater flexibility in public shareholding timelines and higher anchor investor allocations, combined with eased disclosure requirements for low-risk foreign investors, is broadening access to equity markets. Additionally, the reclassification of REITs as equity for mutual funds and reduced exit loads are improving liquidity and expanding the range of investable instruments for both retail and institutional clients.

These developments present compelling opportunities for portfolio diversification and strategic allocation of domestic capital. That said, rigorous due diligence remains critical. While regulatory easing facilitates broader participation, it also underscores the need to carefully assess investment quality and continuously monitor policy changes to optimise client outcomes in a rapidly evolving market environment.

Our Views: What we Like?

Equities

The weekly price is quite positive, but is close to a near-term resistance of around 25,500. Near-term corrections cannot be ruled out, given the broad sentiments of Indian equities. Therefore, we prefer to invest in large caps and select midcaps where valuations seem reasonable now.

Fixed Income

6.54% on the 10y becomes crucial now. Only a break above that level again could see the 10y yield move to 6.75%. Otherwise, we expect range-bound action between 6.40% and 6.55%. Any dips to 5.65% on 5y OIS are good to pay in our view.

Commodities

We continue to remain upbeat on precious metals. We believe Silver could outperform gold. It did so this week. We did not see a follow-through in base Metals this week after a rally last week. We remain neutral on base Metals and Crude for now.

FX

Dollar index hit the lowest level since Feb’22 but recovered sharply during the week from lows. We have been bearish

on the Dollar for some time now